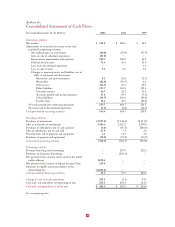

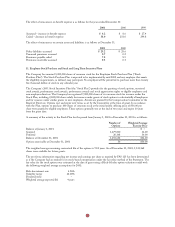

Anthem Blue Cross 2001 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2001 Anthem Blue Cross annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

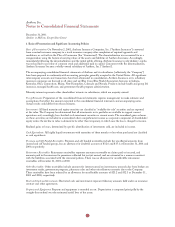

45

Anthem, Inc.

Notes to Consolidated Financial Statements

December 31, 2001

(Dollars in Millions, Except Share Data)

1. Basis of Presentation and Significant Accounting Policies

Basis of Presentation: On November 2, 2001, Anthem Insurance Companies, Inc. (“Anthem Insurance”) converted

from a mutual insurance company to a stock insurance company after completion of required approvals and

conditions, as set forth in the Plan of Conversion (the “Conversion”). The demutualization was accounted for as a

reorganization using the historical carrying values of the assets and liabilities of Anthem Insurance. Accordingly,

immediately following the demutualization and the initial public offering, Anthem Insurance’s policyholders’ surplus

was reclassified to par value of common stock and additional paid in capital. Concurrent with the demutualization,

Anthem Insurance became a wholly-owned subsidiary of Anthem, Inc. (“Anthem”).

The accompanying consolidated financial statements of Anthem and its subsidiaries (collectively, the “Company”)

have been prepared in conformity with accounting principles generally accepted in the United States. All significant

intercompany accounts and transactions have been eliminated in consolidation. Anthem Insurance or its subsidiary

insurance companies are licensed in all states and are Blue Cross Blue Shield Association licensees in Indiana,

Kentucky, Ohio, Connecticut, Maine, New Hampshire, Colorado and Nevada. Products include health and group life

insurance, managed health care, and government health program administration.

Minority interest represents other shareholders’ interests in subsidiaries, which are majority-owned.

Use of Estimates: Preparation of the consolidated financial statements requires management to make estimates and

assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes.

Actual results could differ from those estimates.

Investments: All fixed maturity and equity securities are classified as “available-for-sale” securities and are reported

at fair value. The Company has determined that all investments in its portfolio are available to support current

operations and, accordingly, has classified such investment securities as current assets. The unrealized gains or losses

on these securities are included in accumulated other comprehensive income as a separate component of shareholders’

equity unless the decline in value is deemed to be other than temporary, in which case the loss is charged to income.

Realized gains or losses, determined by specific identification of investments sold, are included in income.

Cash Equivalents: All highly liquid investments with maturities of three months or less when purchased are classified

as cash equivalents.

Premium and Self Funded Receivables: Premium and self funded receivables include the uncollected amounts from

insured and self funded groups, less an allowance for doubtful accounts of $32.6 and $35.1 at December 31, 2001 and

2000, respectively.

Reinsurance Receivables: Reinsurance receivables represent amounts recoverable on claims paid or incurred, and

amounts paid to the reinsurer for premiums collected but not yet earned, and are estimated in a manner consistent

with the liabilities associated with the reinsured policies. There was no allowance for uncollectible reinsurance

receivables at December 31, 2001 or 2000.

Other Receivables: Other receivables include amounts for interest earned on investments, proceeds due from brokers on

investment trades, government programs, pharmacy sales and other miscellaneous amounts due to the Company.

These receivables have been reduced by an allowance for uncollectible amounts of $23.2 and $32.3 at December 31,

2001 and 2000, respectively.

Restricted Cash and Investments: Restricted cash and investments represent fiduciary amounts held under an insurance

contract and other agreements.

Property and Equipment: Property and equipment is recorded at cost. Depreciation is computed principally by the

straight-line method over the estimated useful lives of the assets.