Anthem Blue Cross 2001 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2001 Anthem Blue Cross annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

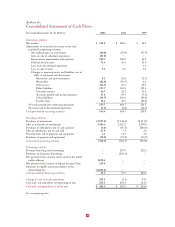

In connection with our acquisitions of BCBS-ME and BCBS-NH, further limitations were imposed on

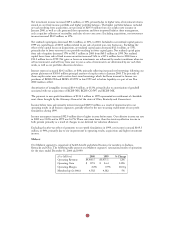

their ability to pay dividends. Until June 2005, BCBS-ME may not declare any dividend without the prior

approval of the Department of Insurance of Maine. BCBS-NH could not pay any dividends for as long as it

continued to use certain favorable statutory accounting practices permitted by the New Hampshire

Department of Insurance before our acquisition. Such practices permitted by the New Hampshire

Department of Insurance had no effect on our consolidated financial statements. The application of these

permitted statutory accounting practices have been discontinued subsequent to December 31, 2001. The

maximum dividend payable to Anthem Insurance from its licensed insurance company subsidiaries without

prior approval in 2001 was approximately $163.0 million. The dividends paid by such regulated subsidiaries

in 2001 to Anthem Insurance were $368.1 million, which includes some extraordinary dividends. The

amount of dividends planned to be paid by Anthem Insurance to Anthem in 2002 is $400.0 million.

Pending approval of the Indiana Department of Insurance, this 2002 dividend is expected to be paid by the

end of the first quarter of 2002, and will be classified as an ordinary dividend.

Credit Facilities and Commercial Paper

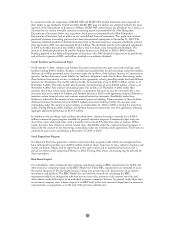

On November 5, 2001, Anthem and Anthem Insurance entered into two new unsecured revolving credit

facilities totaling $800.0 million. Anthem is jointly and severally liable for all borrowings under the facilities.

Anthem also will be permitted to be a borrower under the facilities, if the Indiana Insurance Commissioner

approves Anthem Insurance’s joint liability for Anthem’s obligations under the facilities. Borrowings under

these facilities bear interest at rates, as defined in the agreements, which generally provide for three different

interest rate alternatives. One facility, which provides for borrowings of up to $400.0 million, expires as of

November 5, 2006. The other facility, which provides for borrowings of up to $400.0 million, expires as of

November 4, 2002. Any amount outstanding under this facility as of November 4, 2002 (other than

amounts which bear interest rates determined by a competitive bid process) may be converted into a one-

year term loan at the option of Anthem and Anthem Insurance. Each credit agreement requires Anthem to

maintain certain financial ratios and contains minimal restrictive covenants. Availability under these

facilities is reduced by the amount of any commercial paper outstanding. Upon execution of these facilities,

Anthem Insurance terminated its prior $300.0 million unsecured revolving facility. No amounts were

outstanding under the current or prior facilities as of December 31, 2001 or 2000 or during the years then

ended. During February, 2002, Anthem and Anthem Insurance entered into two new agreements allowing

aggregate additional borrowings of $135.0 million.

In addition to the revolving credit facilities described above, Anthem Insurance currently has a $300.0

million commercial paper program available for general corporate purposes. Commercial paper notes are

short term senior unsecured notes, with a maturity not to exceed 270 days from date of issuance. When

issued, the notes bear interest at current market rates. Availability under the commercial paper program is

reduced by the amount of any borrowings outstanding under our revolving credit agreements. There were no

commercial paper notes outstanding at December 31, 2001 or 2000.

Stock Repurchase Program

Our Board of Directors approved a common stock repurchase program under which our management has

been authorized to purchase up to $400.0 million worth of shares from time to time, subject to business and

market conditions. Shares may be repurchased in the open market and in negotiated transactions for a

period of twelve months beginning February 6, 2002. During 2002, shares outstanding may be affected by

share repurchases.

Risk-Based Capital

Our subsidiaries’ states of domicile have statutory risk-based capital, or RBC, requirements for health and

other insurance companies based on the RBC Model Act. These RBC requirements are intended to assess

the capital adequacy of life and health insurers, taking into account the risk characteristics of an insurer’s

investments and products. The RBC Model Act sets forth the formula for calculating the RBC

requirements which are designed to take into account asset risks, insurance risks, interest rate risks and

other relevant risks with respect to an individual insurance company’s business. In general, under these laws,

an insurance company must submit a report of its RBC level to the state insurance department or insurance

commissioner, as appropriate, as of the end of the previous calendar year.

38