Advance Auto Parts 2006 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2006 Advance Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

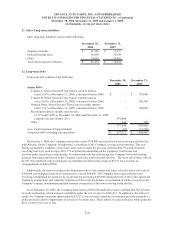

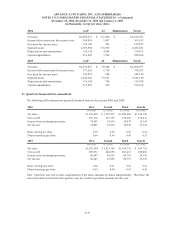

ADVANCE AUTO PARTS, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

December 30, 2006, December 31, 2005 and January 1, 2005

(in thousands, except per share data)

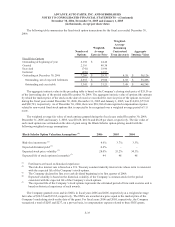

2006 2005

Change in benefit obligation:

Benefit obligation at beginning of the year 13,711$ 14,625$

Interest cost 726 802

Benefits paid (794) (1,513)

Actuarial gain (3,126) (203)

Benefit obligation at end of the year 10,517 13,711

Change in plan assets:

Fair value of plan assets at beginning of the year - -

Employer contributions 794 1,513

Participant contributions 1,088 2,336

Benefits paid (1,882) (3,849)

Fair value of plan assets at end of year - -

Funded Status 10,517 13,711

Reconciliation of funded status:

Funded status (10,517) (13,711)

Unrecognized prior service cost - (6,531)

Unrecognized actuarial loss - 3,929

Accrued postretirement benefit cost (10,517)$ (16,313)$

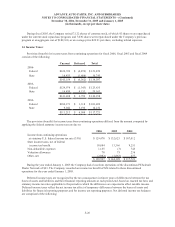

Net periodic postretirement benefit cost is as follows:

2006 2005 2004

Service cos

t

-$-$ 2$

Interest cos

t

726 802 1,004

A

mort

i

zat

i

on o

f

t

h

e pr

i

or serv

i

ce cos

t

(

5

81)

(

5

81)

(436)

Amortization of recognized net losses 210 239 250

355$ 460$ 820$

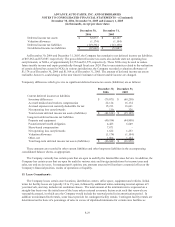

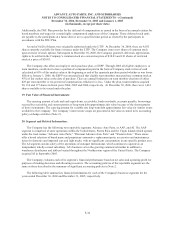

The health care cost trend rate was assumed to be 11.5% for 2007, 10.0% for 2008, 9.5% for 2009, 8.5% for

2010, 8.0% for 2011, 7.0% for 2012 and 5.0% to 6.0% for 2013 and thereafter. If the health care cost were increased

1% for all future years the accumulated postretirement benefit obligation would have increased by $285 as of

December 30, 2006. The effect of this change on the combined service and interest cost would have been an increase

of $26 for 2006. If the health care cost were decreased 1% for all future years the accumulated postretirement

benefit obligation would have decreased by $258 as of December 30, 2006. The effect of this change on the

combined service and interest cost would have been a decrease of $25 for 2006.

The postretirement benefit obligation and net periodic postretirement benefit cost was computed using the

following weighted average discount rates as determined by the Company’s actuaries for each applicable year:

2006 2005

Postretirement benefit obligation 5.50% 5.50%

Net periodic postretirement benefit cost 5.50% 5.75%

F-31