Qantas 2014 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2014 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

|

|

115

QANTAS ANNUAL REPORT 2014

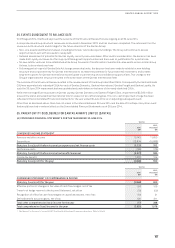

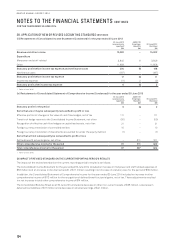

The cost of acquired assets includes the initial estimate at the time of installation and during the period of use, when relevant, the

costs of dismantling and removing the items and restoring the site on which they are located, and changes in the measurement

of existing liabilities recognised for these costs resulting from changes in the timing or outflow of resources required to settle the

obligation or from changes in the discount rate. Subsequent expenditure is capitalised when it is probable that future economic

benefits associated with the expenditure will flow to the Group.

The unwinding of the discount is treated as a finance charge. The cost also may include transfers from hedge reserve of any gain or

loss on qualifying cash flow hedges of foreign currency purchases of property, plant and equipment in accordance with Note 36(C).

Borrowing costs associated with the acquisition of qualifying assets, such as aircraft and the acquisition, construction or production

of significant items of other property, plant and equipment, are recognised as part of the cost of the asset to which they relate.

Depreciation

Depreciation is provided on a straight-line basis on all items of property, plant and equipment except for freehold land, which is

not depreciated. The depreciation rates of owned assets are calculated so as to allocate the cost or valuation of an asset, less

any estimated residual value, over the asset’s estimated useful life to the Qantas Group. Assets are depreciated from the date of

acquisition or, with respect to internally constructed assets, from the time an asset is completed and available for use. The costs of

improvements to assets are depreciated over the remaining useful life of the asset or the estimated useful life of the improvement,

whichever is the shorter. Assets under finance lease are depreciated over the term of the relevant lease or, where it is likely the

Qantas Group will obtain ownership of the asset, the life of the asset.

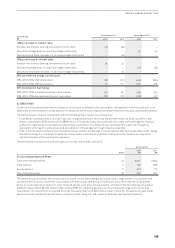

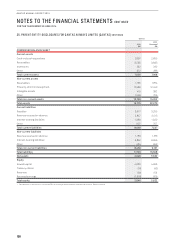

The principal asset depreciation periods and estimated residual value percentages are:

Years

Residual

Value (%)

Buildings and leasehold improvements 10 – 40 01

Plant and equipment 3 – 20 0

Passenger aircraft and engines 2.5 – 20 0 – 10

Freighter aircraft and engines 2.5 – 20 0 – 20

Aircraft spare parts 15 – 20 0 – 20

1 Certain leases allow for the sale of leasehold improvements for fair value. In these instances, the expected fair value is used as the estimated residual value.

Useful lives and residual values are reviewed annually and reassessed having regard to commercial and technological developments,

the estimated useful life of assets to the Qantas Group and the long-term fleet plan.

Finance Leased and Hire Purchase Assets

Leased assets under which the Qantas Group assumes substantially all the risks and benefits of ownership are classified as finance

leases. Other leases are classified as operating leases.

Linked transactions involving the legal form of a lease are accounted for as one transaction when a series of transactions are

negotiated as one or take place concurrently or in sequence and cannot be understood economically alone.

Finance leases are capitalised. A lease asset and a lease liability equal to the present value of the minimum lease payments

and guaranteed residual value are recorded at the inception of the lease. Any gains and losses arising under sale and leaseback

arrangements are deferred and depreciated over the lease term. Capitalised leased assets are depreciated on a straight-line basis

over the period in which benefits are expected to arise from the use of those assets. Lease payments are allocated between the

reduction in the principal component of the lease liability and the interest element.

The interest element is charged to the Consolidated Income Statement over the lease term so as to produce a constant periodic rate

of interest on the remaining balance of the lease liability.

Fully prepaid leases are classified in the Consolidated Balance Sheet as hire purchase assets to recognise that the financing

structures impose certain obligations, commitments and/or restrictions on the Qantas Group, which differentiate these aircraft from

owned assets.

Leases are deemed to be non-cancellable if significant financial penalties associated with termination are anticipated.