Chevron 2007 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2007 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

31

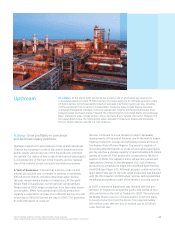

Upstream Earnings for the upstream segment are closely

aligned with industry price levels for crude oil and natural

gas. Crude oil and natural gas prices are subject to external

factors over which the company has no control, including

product demand connected with global economic conditions,

industry inventory levels, production quotas imposed by the

Organization of Petroleum Exporting Countries (OPEC),

weather-related damage and disruptions, competing fuel

prices, and regional supply interruptions or fears thereof that

may be caused by military conflicts, civil unrest or political

uncertainty. Moreover, any of these factors could also inhibit

the company’s production capacity in an affected region.

The company monitors developments closely in the countries

in which it operates and holds investments, and attempts to

manage risks in operating its facilities and business.

Price levels for capital and exploratory costs and operat-

ing expenses associated with the efficient production of crude

oil and natural gas can also be subject to external factors

beyond the company’s control. External factors include not

only the general level of inflation but also prices charged by

the industry’s material and service providers, which can be

affected by the volatility of the industry’s own supply and

demand conditions for such materials and services. The

oil and gas industry worldwide has experienced significant

price increases for these items since 2005, and future price

increases may continue to exceed the general level of infla-

tion. Capital and exploratory expenditures and operating

expenses also can be affected by damages to production

facilities caused by severe weather or civil unrest.

Industry price levels for crude oil increased during

2007. The spot price for West Texas Intermediate (WTI)

crude oil, a benchmark crude oil, averaged $72 per barrel in

2007, up approximately $6 per barrel from the 2006 average

price. The rise in crude oil prices was attributed primarily

to increasing demand in growing economies, the heightened

level of geopolitical uncertainty in some areas of the world

and supply concerns in other key producing regions. As of

mid-February 2008, the WTI price was about $93 per barrel.

As in 2006, a wide differential in prices existed in 2007

between high-quality (i.e., high-gravity, low-sulfur) crude oils

and those of lower quality (i.e., low-gravity, heavier types of

crude). The price for the heavier crudes has been dampened

because of ample supply and lower relative demand due to

the limited number of refineries that are able to process this

lower-quality feedstock into light products (i.e., motor gaso-

line, jet fuel, aviation gasoline and diesel fuel). The price for

higher-quality crude oil has remained high, as the demand

for light products, which can be more easily manufactured by

refineries from high-quality crude oil, has been strong world-

wide. Chevron produces or shares in the production of heavy

crude oil in California, Chad, Indonesia, the Partitioned

Neutral Zone between Saudi Arabia and Kuwait, Venezuela

and certain fields in Angola, China and the United Kingdom

North Sea. (Refer to page 38 for the company’s average U.S.

and international crude oil prices.)

In contrast to price movements in the global market

for crude oil, price changes for natural gas in many regional

markets are more closely aligned with supply and demand

conditions in those markets. In the United States during

2007, benchmark prices at Henry Hub averaged about $7 per

thousand cubic feet (MCF), compared with about $6.50 in

2006. As of mid-February 2008, the Henry Hub price was

about $8 per MCF. Fluctuations in the price for natural gas

in the United States are closely associated with the volumes

produced in North America and the inventory in under-

ground storage relative to customer demand. U.S. natural gas

prices are also typically higher during the winter period when

demand for heating is greatest.

Certain other regions of the world in which the com-

pany operates have different supply, demand and regulatory

circumstances, typically resulting in significantly lower

average sales prices for the company’s production of natural

gas. (Refer to page 38 for the company’s average natural gas

prices for the U.S. and international regions.) Additionally,

excess-supply conditions that exist in certain parts of the

world cannot easily serve to mitigate the relatively high-price

Crude Oil Prices 1987 Through 2007

/. // /0 0' 0( 0) 0* 0+ 0, 0- 0. 0/ 00 '' '( '+') '* ', '- '.

0'%,/

('

.'

-'

,'

(''

0'

/'

+'

*'

)'

009 – Crude Oil Prices 1986 through 2006 – v3

011 – U.S. Natural Gas Prices – v3

'

*'''

)+''

-''

()''

(/''

'%''

/%''

-%''

+%''

)%''

U.S. Natural Gas Realizations

Net Production

'+'* ', '- '.

-%()

(#-00

'

),''

)'''

(,''

('''

,''

10B – Net Crude Oil Nat Gas

Liquids Production back – v3

Net Crude Oil Natural Gas

Liquids Production

'+'* ', '- '.

(#.,-