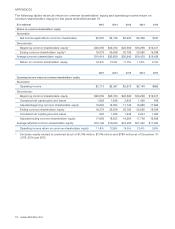

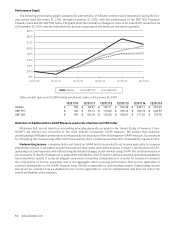

Allstate 2015 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2015 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

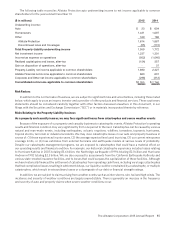

The Allstate Corporation 2015 Annual Report 87

insurance in the state, except pursuant to a plan that is approved by the state insurance department. Additionally, certain

states require insurers to participate in guaranty funds for impaired or insolvent insurance companies. These funds

periodically assess losses against all insurance companies doing business in the state. Our operating results and financial

condition could be adversely affected by any of these factors.

The potential benefits of our sophisticated risk segmentation process may not be fully realized

We believe that our sophisticated pricing and underwriting methods has allowed us to offer competitive pricing and

operate profitably. However, because many of our competitors seek to adopt underwriting criteria and sophisticated

pricing models similar to those we use, our competitive advantage could decline or be lost. Further, the use of increasingly

sophisticated pricing models is being reviewed by regulators and special interest groups. Competitive pressures could

also force us to modify our sophisticated pricing models. Furthermore, we cannot be assured that these sophisticated

pricing models will accurately reflect the level of losses that we will ultimately incur.

Changes in the level of price competition and the use of underwriting standards in the property and casualty

business may adversely affect our operating results and financial condition

The property and casualty market has experienced periods characterized by relatively high levels of price competition,

less restrictive underwriting standards and relatively low premium rates, followed by periods of relatively lower levels of

competition, more selective underwriting standards and relatively high premium rates. A downturn in the profitability of

the property and casualty business could have a material effect on our operating results and financial condition.

Actual claims incurred may exceed current reserves established for claims and may adversely affect our operating

results and financial condition

Recorded claim reserves in the Property-Liability business are based on our best estimates of losses, both reported and

incurred but not reported claims reserves (“IBNR”), after considering known facts and interpretations of circumstances.

Internal factors are considered including our experience with similar cases, actual claims paid, historical trends involving

claim payment patterns, pending levels of unpaid claims, loss management programs, product mix and contractual

terms. External factors are also considered, such as court decisions; changes in law; litigation imposing unintended

coverage and benefits such as disallowing the use of benefit payment schedules, requiring coverage designed to cover

losses that occur in a single policy period to losses that develop continuously over multiple policy periods or requiring

the availability of multiple limits; regulatory requirements and economic conditions. Because reserves are estimates

of the unpaid portion of losses that have occurred, including IBNR losses, the establishment of appropriate reserves,

including reserves for catastrophes, is an inherently uncertain and complex process. The ultimate cost of losses may vary

materially from recorded reserves and such variance may adversely affect our operating results and financial condition

as the reserves are reestimated.

Predicting claim costs relating to asbestos, environmental and other discontinued lines is inherently uncertain and

may have a material effect on our operating results and financial condition

The process of estimating asbestos, environmental and other discontinued lines liabilities is complicated by complex

legal issues concerning, among other things, the interpretation of various insurance policy provisions and whether losses

are covered, or were ever intended to be covered, and whether losses could be recoverable through retrospectively

determined premium, reinsurance or other contractual agreements. Asbestos-related bankruptcies and other asbestos

litigation are complex, lengthy proceedings that involve substantial uncertainty for insurers. Actuarial techniques and

databases used in estimating asbestos, environmental and other discontinued lines net loss reserves may prove to be

inadequate indicators of the extent of probable loss. Ultimate net losses from these discontinued lines could materially

exceed established loss reserves and expected recoveries and have a material effect on our operating results and financial

condition as the reserves are reestimated.

Risks Relating to the Allstate Financial Segment

Changes in underwriting and actual experience could materially affect profitability and financial condition

Our product pricing includes long-term assumptions regarding investment returns, mortality, morbidity, persistency

and operating costs and expenses of the business. We establish target returns for each product based upon these factors

and the average amount of capital that we must hold to support in-force contracts taking into account rating agencies and

regulatory requirements. We monitor and manage our pricing and overall sales mix to achieve target new business returns

on a portfolio basis, which could result in the discontinuation or de-emphasis of products and a decline in sales. Profitability

from new business emerges over a period of years depending on the nature and life of the product and is subject to variability

as actual results may differ from pricing assumptions. Additionally, many of our products have fixed or guaranteed terms

that limit our ability to increase revenues or reduce benefits, including credited interest, once the product has been issued.