Allstate 2015 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2015 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

The Allstate Corporation 2015 Annual Report 97

Management’s Discussion and Analysis of Financial Condition and Results of Operations

OVERVIEW

The following discussion highlights significant factors influencing the consolidated financial position and results of

operations of The Allstate Corporation (referred to in this document as “we,” “our,” “us,” the “Company” or “Allstate”).

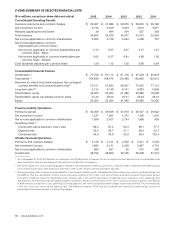

It should be read in conjunction with the 5-year summary of selected financial data, consolidated financial statements

and related notes found under Part II. Item 6. and Item 8. contained herein. Further analysis of our insurance segments

is provided in the Property-Liability Operations (which includes the Allstate Protection and the Discontinued Lines

and Coverages segments) and in the Allstate Financial Segment sections of Management’s Discussion and Analysis

(“MD&A”). The segments are consistent with the way in which we use financial information to evaluate business

performance and to determine the allocation of resources. Resources are allocated by the chief operating decision

maker and performance is assessed for Allstate Protection, Discontinued Lines and Coverages and Allstate Financial.

Allstate Protection and Allstate Financial performance and resources are managed by committees of senior officers of

the respective segments.

Allstate is focused on the following priorities in 2016:

• better serve our customers through innovation, effectiveness and efficiency;

• achieve target economic returns on capital;

• grow insurance policies in force;

• proactively manage investments; and

• build and acquire long-term growth platforms.

The most important factors we monitor to evaluate the financial condition and performance of our company include:

• For Allstate Protection: premium, the number of policies in force (“PIF”), new business sales, policy retention,

price changes, claim frequency and severity, catastrophes, loss ratio, expenses, underwriting results, and relative

competitive position.

• For Allstate Financial: benefit and investment spread, asset-liability matching, amortization of deferred policy

acquisition costs (“DAC”), expenses, operating income, net income, new business sales, invested assets, and

premiums and contract charges.

• For Investments: exposure to market risk, asset allocation, credit quality/experience, total return, net investment

income, cash flows, realized capital gains and losses, unrealized capital gains and losses, stability of long-term

returns, and asset and liability duration.

• For financial condition: liquidity, parent holding company level of deployable assets, financial strength ratings,

operating leverage, debt levels, book value per share, and return on equity.

Summary of Results:

• Consolidated net income applicable to common shareholders was $2.06 billion in 2015 compared to $2.75 billion

in 2014 and $2.26 billion in 2013. The decrease in 2015 compared to 2014 was primarily due to higher Property-

Liability insurance claims and claims expense and lower realized net capital gains and net investment income,

partially offset by higher Property-Liability insurance premiums and decreased catastrophe losses and operating

costs and expenses. The increase in 2014 compared to 2013 was primarily due to lower loss on disposition

related to the Lincoln Benefit Life Company (“LBL”) sale recorded in Allstate Financial and loss on extinguishment

of debt charges reported in Corporate and Other, partially offset by lower net income applicable to common

shareholders from Property-Liability. Net income applicable to common shareholders per diluted common share

was $5.05, $6.27 and $4.81 in 2015, 2014 and 2013, respectively.

• Allstate Protection had underwriting income of $1.61 billion in 2015 compared to $1.89 billion in 2014 and $2.36

billion in 2013. The decrease in 2015 compared to 2014 was primarily due to decreases in underwriting income in

auto and commercial lines, partially offset by increases in underwriting income in homeowners and other personal

lines and lower catastrophe losses. The decrease in 2014 compared to 2013 was primarily due to decreases in

underwriting income in homeowners, auto and other personal lines resulting from increased catastrophe losses.

For a discussion on the components of the increase (decrease) in underwriting income, see the Allstate Protection

segment section of the MD&A. The Allstate Protection combined ratio was 94.7, 93.5 and 91.5 in 2015, 2014 and

2013, respectively. Underwriting income, a measure not based on accounting principles generally accepted in the

United States of America (“GAAP”), is defined in the Property-Liability Operations section of the MD&A.

• Allstate Financial net income applicable to common shareholders was $663 million in 2015 compared to $631

million in 2014 and $95 million in 2013. The increase in 2015 primarily relates to higher net realized capital gains

and lower loss on disposition related to the LBL sale, partially offset by lower net investment income and the

reduction in business due to the sale of LBL. The increase in 2014 primarily relates to lower loss on disposition

related to the LBL sale, partially offset by the associated reduction in business.