Xcel Energy 2007 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2007 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

(including both depreciation expense less returns from the investments fund) and amounts recorded under SFAS

No. 143 are deferred as a regulatory asset.

Income Tax Accruals

Judgment, uncertainty, and estimates are a significant aspect of the income tax accrual process that accounts for the

effects of current and deferred income taxes. Uncertainty associated with the application of tax statutes and regulations

and the outcomes of tax audits and appeals require that judgment and estimates be made in the accrual process and in

the calculation of effective tax rates.

Effective tax rates (ETR) are also highly impacted by assumptions. ETR calculations are revised every quarter based on

best available year-end tax assumptions (income levels, deductions, credits, etc.) by legal entity; adjusted in the following

year after returns are filed, with the tax accrual estimates being trued-up to the actual amounts claimed on the tax

returns; and further adjusted after examinations by taxing authorities have been completed.

In accordance with the interim reporting rules under APB 28, a tax expense or benefit is recorded every quarter to

eliminate the difference in continuing operations tax expense computed based on the actual year-to-date ETR and the

forecasted annual ETR.

Accounting for Uncertainty in Income Taxes — an interpretation of FASB Statement No. 109 (FIN 48), has impacted

the income tax accrual process in that the new accounting rule requires that only tax benefits that meet the ‘‘more

likely than not’’ recognition threshold can be recognized or continue to be recognized. The change in the unrecognized

tax benefits need to be reasonably estimated based on evaluation of the nature of uncertainty, the nature of event that

could cause the change and an estimate of range of reasonably possible changes. At any period end, and as new

developments occur, management will use prudent business judgment to unrecognize appropriate amounts of tax

benefits. Unrecognized tax benefits can be recognized as issues are favorably resolved and loss exposures decline. As

required, Xcel Energy adopted FIN 48 as of Jan. 1, 2007 and the initial derecognition amounts were reported as a

cumulative effect of a change in accounting principle. The cumulative effect of the change, which was reported as an

adjustment to the beginning balance of retained earnings, was not material.

As disputes with the IRS and state tax authorities are resolved over time, we may need to adjust our unrecognized tax

benefits and interest accruals to the updated estimates needed to satisfy tax and interest obligations for the related

issues. These adjustments may be favorable or unfavorable, increasing or decreasing earnings.

See Note 7 for further details regarding income taxes.

Employee Benefits

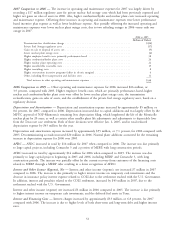

Xcel Energy’s pension costs are based on an actuarial calculation that includes a number of key assumptions, most

notably the annual return level that pension investment assets will earn in the future and the interest rate used to

discount future pension benefit payments to a present value obligation for financial reporting. In addition, the actuarial

calculation uses an asset-smoothing methodology to reduce the volatility of varying investment performance over time.

Note 10 to the consolidated financial statements discusses the rate of return and discount rate used in the calculation of

pension costs and obligations in the accompanying financial statements.

Pension costs have been increasing in recent years, but are expected to decrease over the next several years, due to

higher-than-expected investment returns experienced in recent years, as well as voluntary company contributions. While

investment returns exceeded the assumed level of 8.75 percent in 2006 and 2005 and 9.0 percent in 2004, investment

returns in 2007, 2003 and 2002 were below the assumed level of 8.75, 9.25 and 9.5 percent respectively, and discount

rates have increased to 6.00 percent used in 2007. Xcel Energy continually reviews its pension assumptions and, in

2008, expects to maintain the investment return assumption at 8.75 percent and to increase the discount rate

assumption to 6.25 percent.

The investment gains or losses resulting from the difference between the expected pension returns assumed on asset

levels and actual returns earned are deferred in the year the difference arises and recognized over the subsequent

five-year period. This gain or loss recognition occurs by using a five-year, moving-average value of pension assets to

measure expected asset returns in the cost-determination process, and by amortizing deferred investment gains or losses

over the subsequent five-year period. Based on current assumptions and the recognition of past investment gains and

losses over the next five years, Xcel Energy currently projects that the pension costs recognized for financial reporting

purposes in continuing operations will decrease from an expense, of $11.4 million in 2007 to income of $6.0 million

in 2008 and income of $8.4 million in 2009.

59