Xcel Energy 2007 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2007 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

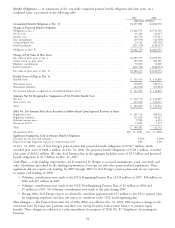

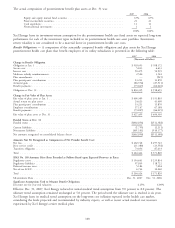

Benefit Obligations — A comparison of the actuarially computed pension-benefit obligation and plan assets, on a

combined basis, is presented in the following table:

2007 2006

(Thousands of Dollars)

Accumulated Benefit Obligation at Dec. 31 ..................................... $2,497,898 $2,486,370

Change in Projected Benefit Obligation

Obligation at Jan. 1 .................................................... $2,666,555 $2,796,780

Service cost ......................................................... 61,392 61,627

Interest cost ......................................................... 162,774 155,413

Plan amendments ...................................................... (19,955) (16,569)

Actuarial (gain) loss .................................................... 23,325 (82,339)

Benefit payments ...................................................... (231,332) (248,357)

Obligation at Dec. 31 ................................................... $2,662,759 $2,666,555

Change in Fair Value of Plan Assets

Fair value of plan assets at Jan. 1 ............................................ $3,183,375 $3,093,536

Actual return on plan assets ............................................... 199,230 306,196

Employer contributions .................................................. 35,000 32,000

Benefit payments ...................................................... (231,332) (248,357)

Fair value of plan assets at Dec. 31 ........................................... $3,186,273 $3,183,375

Funded Status of Plans at Dec. 31

Funded status ........................................................ $ 523,514 $ 516,820

Noncurrent assets ...................................................... 568,055 586,712

Noncurrent liabilities ................................................... (44,541) (69,892)

Net pension amounts recognized on consolidated balance sheets ......................... $ 523,514 $ 516,820

Amounts Not Yet Recognized as Components of Net Periodic Benefit Cost:

Net loss ............................................................ $ 216,776 $ 143,695

Prior service cost ...................................................... 123,426 168,437

Total ............................................................. $ 340,202 $ 312,132

SFAS No. 158 Amounts Have Been Recorded as Follows Based Upon Expected Recovery in Rates:

Regulatory assets ...................................................... $ 205,720 208,216

Regulatory liabilities .................................................... 111,650 89,627

Deferred income taxes ................................................... 9,780 6,312

Net-of-tax AOCI ...................................................... 13,052 7,977

Total ............................................................. $ 340,202 312,132

Measurement Date ..................................................... Dec. 31, 2007 Dec. 31, 2006

Significant Assumptions Used to Measure Benefit Obligations

Discount rate for year-end valuation .......................................... 6.25% 6.00%

Expected average long-term increase in compensation level ............................ 4.00 4.00

At Dec. 31, 2007, one of Xcel Energy’s pension plans had projected benefit obligations of $732.7 million, which

exceeded plan assets of $688.1 million. At Dec. 31, 2006, the projected benefit obligations of $728.1 million, exceeded

plan assets of $658.2 million. All other Xcel Energy plans in the aggregate had plan assets of $2.5 billion and projected

benefit obligations of $1.9 billion on Dec. 31, 2007.

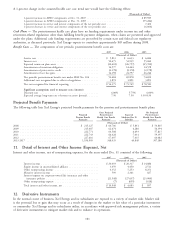

Cash Flows — Cash funding requirements can be impacted by changes to actuarial assumptions, actual asset levels and

other calculations prescribed by the funding requirements of income tax and other pension-related regulations. These

regulations did not require cash funding for 2005 through 2007 for Xcel Energy’s pension plans and are not expected

to require cash funding in 2008.

• Voluntary contributions were made to the PSCo Bargaining Pension Plan of $35 million in 2007, $30 million in

2006 and $15 million in 2005.

• Voluntary contributions were made to the NCE Non-Bargaining Pension Plan of $2 million in 2006 and

$5 million in 2005. No voluntary contributions were made to the plan during 2007.

• During 2008, Xcel Energy expects to voluntarily contribute approximately $35 million to the PSCo pension plan

for bargaining employees and does not expect to contribute to the NCE non-bargaining plan.

Plan Changes — The Pension Protection Act of 2006 (PPA) was effective Dec. 31, 2006. PPA requires a change in the

conversion basis for lump-sum payments and three-year vesting for plans with account balance or pension equity

benefits. These changes are reflected as a plan amendment for purposes of SFAS No. 87-’’Employers’ Accounting for

Pensions’’.

98