Western Union 2012 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2012 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

76

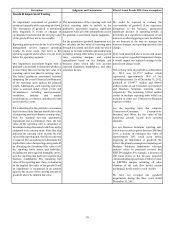

Description Judgments and Uncertainties Effect if Actual Results Differ from Assumptions

Goodwill Impairment Testing

An impairment assessment of goodwill is

conducted annually at the reporting unit level.

This assessment of goodwill is performed

more frequently if events or changes in

circumstances indicate that the carrying value

of the goodwill may not be recoverable.

Reporting units are driven by the level at which

management reviews segment operating

results. In some cases, that level is the

operating segment and in others it is one level

below the operating segment.

Our impairment assessment begins with a

qualitative assessment to determine whether it

is more likely than not that the fair value of a

reporting unit is less than its carrying value.

The initial qualitative assessment includes

comparing the overall financial performance

of the reporting units against the planned

results. Additionally, each reporting unit's fair

value is assessed under certain events and

circumstances, including macroeconomic

conditions, industry and market

considerations, cost factors, and other relevant

entity-specific events.

If it is determined in the qualitative assessment

that it is more likely than not that the fair value

of a reporting unit is less than its carrying value,

then the standard two-step quantitative

impairment test is performed. First, the fair

value of the reporting unit is calculated or

determined using discounted cash flows and is

compared to its carrying value. If the first step

indicates the carrying value exceeds the fair

value of the reporting unit, then the second step

is required. The second step is to determine the

implied fair value of a reporting unit's goodwill

by allocating the determined fair value to all

the reporting unit's assets and liabilities,

including any unrecognized intangible assets,

as if the reporting unit had been acquired in a

business combination. The remaining fair

value of the reporting unit, if any, is deemed to

be the implied fair value of the goodwill and

an impairment is recognized in an amount

equal to the excess of the carrying amount of

goodwill above its implied fair value.

The determination of the reporting units and

which reporting units to include in the

qualitative assessment requires significant

judgment. Also, all of the assumptions used in

the qualitative assessment require judgment.

For the quantitative goodwill impairment test,

we calculate the fair value of reporting units

through discounted cash flow analyses which

require us to make estimates and assumptions

including, among other items, revenue growth

rates, operating margins, and capital

expenditures based on our budgets and

business plans which take into account

expected regulatory, marketplace, and other

economic factors.

We could be required to evaluate the

recoverability of goodwill if we experience

disruptions to the business, unexpected

significant declines in operating results, a

divestiture of a significant component of our

business, or other triggering events. In addition,

as our business or the way we manage our

business changes, our reporting units may also

change.

If an event described above occurs and causes

us to recognize a goodwill impairment charge,

it would impact our reported earnings in the

period such charge occurs.

The carrying value of goodwill as of December

31, 2012 was $3,179.7 million which

represented approximately 34% of our

consolidated assets. As of December 31, 2012,

goodwill of $1,947.7 million and $996.0

million resides in our Consumer-to-Consumer

and Business Solutions reporting units,

respectively. The remaining $236.0 million

resides in multiple reporting units which are

included in either our Consumer-to-Business

segment or Other.

For the reporting units that comprise

Consumer-to-Consumer, Consumer-to-

Business, and Other, the fair value of the

businesses greatly exceed their carrying

amounts.

For our Business Solutions reporting unit,

which was recently acquired between 2009 and

2011, a decline in estimated fair value of

approximately 10% could occur before

triggering an impairment of goodwill. We

believe the primary assumptions impacting our

Business Solutions impairment valuation

analysis relate to projected revenue and

EBITDA margins. For example, a decrease of

200 basis points in the ten-year projected

compound annual growth rate of either revenue

or EBITDA margin, assuming all other

elements of the cash flow model remain

unchanged, would result in such decline.

We have not recorded any goodwill

impairments during the three years ended

December 31, 2012.