The Hartford 2010 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2010 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

62

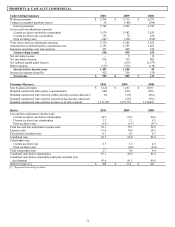

Definitions of Non-GAAP and other measures and ratios

Account Value

Account value includes policyholders’ balances for investment contracts and reserves for future policy benefits for insurance contracts.

Account value is a measure used by the Company because a significant portion of the Company’ s fee income is based upon the level of

account value. These revenues increase or decrease with a rise or fall in the amount of account value whether caused by changes in the

market or through net flows.

After-tax Margin

After-tax margin, excluding realized gains (losses) and DAC Unlock, is a non-GAAP financial measure that the Company uses to

evaluate, and believes is an important measure of, certain of the segment’ s operating performance. After-tax margin is the most directly

comparable U.S. GAAP measure. The Hartford believes that the measure after-tax margin, excluding realized gains (losses) and DAC

Unlock, provides investors with a valuable measure of the performance of certain of the Company’ s on-going businesses because it

reveals trends in those businesses that may be obscured by the effect of realized gains (losses) or quarterly DAC Unlocks. Some

realized capital gains and losses are primarily driven by investment decisions and external economic developments, the nature and

timing of which are unrelated to insurance aspects of our businesses. Accordingly, these non-GAAP measures exclude the effect of all

realized gains and losses that tend to be highly variable from period to period based on capital market conditions. The Hartford

believes, however, that some realized capital gains and losses are integrally related to our insurance operations, so after-tax margin,

excluding realized gains (losses) and DAC Unlock, should include net realized gains and losses on net periodic settlements on credit

derivatives. These net realized gains and losses are directly related to an offsetting item included in the statement of operations such as

net investment income. DAC Unlocks occur when the Company determines based on actual experience or other evidence, that estimates

of future gross profits should be revised. As the DAC Unlock is a reflection of the Company’ s new best estimates of future gross

profits, the result and its impact on the DAC amortization ratio is meaningful; however, it does distort the trend of after-tax margin.

After-tax margin, excluding realized gains (losses) and DAC Unlock, should not be considered as a substitute for after-tax margin and

does not reflect the overall profitability of our businesses. Therefore, the Company believes it is important for investors to evaluate both

after-tax margin, excluding realized gains (losses) and DAC Unlock, and after-tax margin when reviewing the Company’ s performance.

After Tax Margin is calculated by dividing the earnings measures described above by Total Revenues adjusted for the measures

described above. For additional information regarding the DAC Unlock, see Critical Accounting Estimates within the MD&A.

Assets Under Administration

Assets under administration (“AUA”) represents the client asset base of the Company’ s recordkeeping business for which revenues are

predominately based on the number of plan participants. Unlike assets under management, increases or decreases in AUA do not have a

direct corresponding increase or decrease to the Company’ s revenues, and therefore are not included in assets under management.

Assets Under Management

Assets under management (“AUM”) include account values and mutual fund assets. AUM is a measure used by the Company because a

significant portion of the Company’ s revenues are based upon asset values. These revenues increase or decrease with a rise or fall in the

amount of account value whether caused by changes in the market or through net flows.

Catastrophe ratio

The catastrophe ratio (a component of the loss and loss adjustment expense ratio) represents the ratio of catastrophe losses incurred in

the current calendar year (net of reinsurance) to earned premiums and includes catastrophe losses incurred for both the current and prior

accident years. A catastrophe is an event that causes $25 or more in industry insured property losses and affects a significant number of

property and casualty policyholders and insurers. The catastrophe ratio includes the effect of catastrophe losses, but does not include the

effect of reinstatement premiums.

Combined ratio

The combined ratio is the sum of the loss and loss adjustment expense ratio, the expense ratio and the policyholder dividend ratio. This

ratio is a relative measurement that describes the related cost of losses and expenses for every $100 of earned premiums. A combined

ratio below 100.0 demonstrates underwriting profit; a combined ratio above 100.0 demonstrates underwriting losses.

Combined ratio before catastrophes and prior accident year development

The combined ratio before catastrophes and prior accident year development represents the combined ratio for the current accident year,

excluding the impact of catastrophes. The Company believes this ratio is an important measure of the trend in profitability since it

removes the impact of volatile and unpredictable catastrophe losses and prior accident year reserve development.

Current accident year loss and loss adjustment expense ratio before catastrophes

The current accident year loss and loss adjustment expense ratio before catastrophes is a measure of the cost of non-catastrophe claims

incurred in the current accident year divided by earned premiums. Management believes that the current accident year loss and loss

adjustment expense ratio before catastrophes is a performance measure that is useful to investors as it removes the impact of volatile and

unpredictable catastrophe losses and prior accident year reserve development.