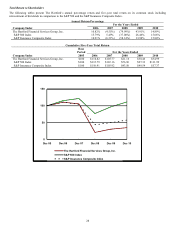

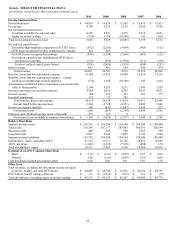

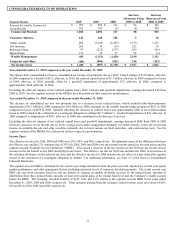

The Hartford 2010 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2010 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

33

OUTLOOKS

The Hartford provides projections and other forward-looking information in the following discussions, which contain many forward-

looking statements, particularly relating to the Company’ s future financial performance. These forward-looking statements are

estimates based on information currently available to the Company, are made pursuant to the safe harbor provisions of the Private

Securities Litigation Reform Act of 1995 and are subject to the precautionary statements set forth on page 3 of this Form 10-K. Actual

results are likely to differ, and in the past have differed, materially from those forecast by the Company, depending on the outcome of

various factors, including, but not limited to, those set forth in each discussion below and in Item 1A, Risk Factors.

In 2011, The Hartford will continue to focus on growing its three customer-oriented divisions, Commercial Markets, Consumer

Markets, and Wealth Management, through enhanced product development, leveraging synergies of the divisions’ product offerings to

meet customer needs, and increased efficiencies throughout the organization. The speed and extent of economic and employment

expansion may impact the asset protection businesses where insureds may change their level of insurance, and asset accumulation

businesses may see customers changing their level of savings based on anticipated economic conditions. The performance of The

Hartford’ s divisions is subject to uncertainty due to market conditions, which impact the earnings of its asset management businesses

and the valuation and earnings on its investment portfolio.

Commercial Markets

Commercial Markets will continue to focus on growth through market-differentiated products and services while maintaining a

disciplined underwriting approach. In the Property & Casualty Commercial insurance marketplace, improving market conditions are

expected to allow for moderate price increases, while a slowly-recovering economy will result in an increase in insurance exposures.

Within Property & Casualty Commercial, the Company expects low to mid single-digit written premium growth in 2011, due to an

increase in pricing, higher new business premium and an increase in premium retention. Additionally, Property & Casualty Commercial

is expected to continue to grow policy counts, particularly for our small commercial business, led by an increase in workers’

compensation in force. This growth potential reflects the combination of our current market position, a broadening of underwriting

expertise focused on selected industries, a leveraging of the payroll model, and numerous initiatives launched in the past several years.

Initiatives include programs aimed at improving policy count retention, the rollout of new product offerings and the introduction of ease

of doing business technology for our small commercial business. The Property & Casualty Commercial combined ratio before

catastrophes and prior accident year development is expected to be slightly higher in 2011 than the 93.4 achieved in 2010 as pricing

increases are expected to largely offset loss cost changes. In the Group Benefits, the economic downturn, combined with the potential

for employees to lessen spending on the Company’ s products and the overall competitive environment, reduced premium levels in 2010.

Premium levels are expected to remain relatively flat in 2011, or until there is economic expansion with lower unemployment rates

compared to 2010 levels. Over time, as employers design benefit strategies to attract and retain employees, while attempting to control

their benefit costs, management believes that the need for the Company’ s products will continue to expand. This combined with the

significant number of employees who currently do not have coverage or adequate levels of coverage, creates continued opportunities for

our products and services. The Company experienced higher disability loss ratios in 2010. The Company anticipates loss ratios to

remain essentially flat in 2011.

Consumer Markets

In 2011, Consumer Markets expects to increase its business written with AARP members and enter into new affinity relationships.

Management expects new business will primarily be generated from continued direct marketing to AARP members, marketing to

households associated with other affinity groups, expanding the sale of the Open Road Advantage auto product through independent

agents and introducing an enhanced homeowners product called Hartford Home Advantage. The Company distributes its discounted

AARP Open Road Advantage auto product through those independent agents who are authorized to offer the AARP product and,

beginning in 2011, will distribute its Hartford Home Advantage product on a discounted basis through those same authorized agents.

The Company expects non-AARP member Agency earned premium to decline in 2011 as the result of continued pricing and

underwriting actions to improve profitability, including efforts to reposition the book into more business for insureds aged 40+. As of

December 31, 2010, the Open Road Advantage auto product was available in 33 states and the Company expects the product to be

available to authorized agents in 42 states by the end of the second quarter of 2011. The Company began rolling out its Hartford Home

Advantage product during the first quarter of 2011 and expects the product to be available in 39 states by the end of 2011. Management

expects that the combined ratio before catastrophes and prior accident year development will improve in 2011, driven by earned pricing

increases, slightly improving claim frequency and modest claim severity in both auto and home as the Company expects to benefit from

a continued shift to a more preferred mix of business.