Rosetta Stone 2012 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2012 Rosetta Stone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

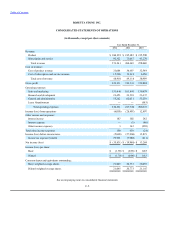

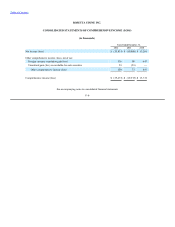

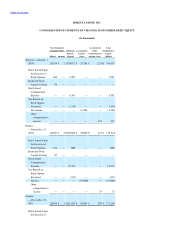

Table of Contents

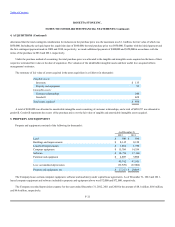

The carrying amounts reported in the consolidated balance sheets for cash and cash equivalents, restricted cash, accounts receivable, accounts

payable and other accrued expenses approximate fair value due to relatively short periods to maturity.

On November 1, 2009, the Company acquired certain assets from SGLC International Co. Ltd. ("SGLC"), a software reseller headquartered in

Seoul, South Korea. As the assets acquired constituted a business, this transaction was accounted for under ASC topic 805,

("ASC 805"). The purchase price consisted of an initial cash payment of $100,000, followed by three annual cash installment payments if the acquired

company's revenues exceed certain targeted levels each of these years. The amount was calculated as the lesser of a percentage of the revenue generated

or a fixed amount for each year, based on the terms of the agreement.

Based on these terms, the minimum additional cash payment would have been zero if none of the minimum revenue targets were met, and the

maximum additional payment was $1.1 million, which amount was recorded as contingent consideration at its fair value of $850,000, resulting in a total

purchase price of $950,000 including the initial cash payment of $100,000 above. Together with the initial cash payment and the first contingent

payment made, we made additional payments of $300,000 and $350,000 in accordance with the terms of the purchase in 2012 and 2011, respectively.

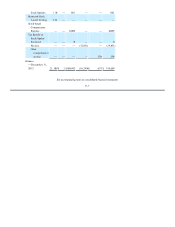

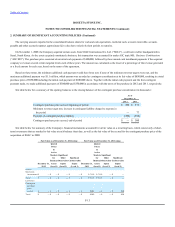

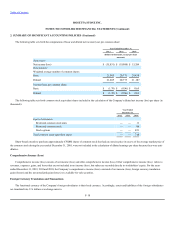

See table below for a summary of the opening balances to the closing balances of the contingent purchase consideration (in thousands):

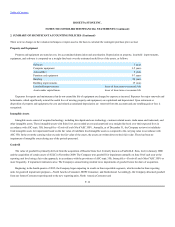

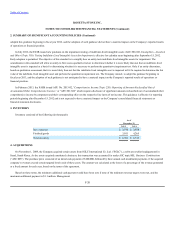

See table below for summary of the Company's financial instruments accounted for at fair value on a recurring basis, which consist only of short-

term investments that are marked to fair value at each balance sheet date, as well as the fair value of the accrual for the contingent purchase price of the

acquisition of SGLC in 2009:

F-13

Contingent purchase price accrual, beginning of period $ 300 $ 573

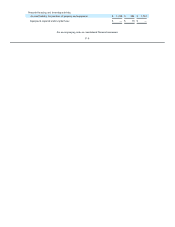

Minimum revenue target met, increase in contingent liability charged to expense in

the period — 77

Payment of contingent purchase liability (300) (350)

Contingent purchase price accrual, end of period $ — $ 300

Short-term

investments $ — $ — $ — $ — $9,711 $9,711 $ — $ —

Total $ — $ — $ — $ — $9,711 $9,711 $ — $ —

Contingent

purchase

price

accrual $ — $ — $ — $ — $300 $ — $ — $300

Total $ — $ — $ — $ — $300 $ — $ — $300