Rosetta Stone 2012 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2012 Rosetta Stone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Table of Contents

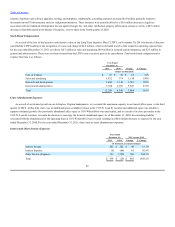

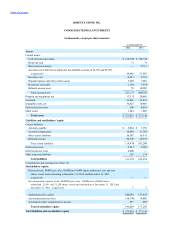

The following table summarizes our contractual obligations at December 31, 2012 and the effect such obligations are expected to have on our

liquidity and cash flow in future periods.

The operating lease obligations reflected in the table above include our corporate office leases and site licenses for our kiosks.

In June 2011, the FASB issued new guidance on comprehensive income presentation (ASU o. 2011-05—.

Under the amendments to Topic 220, an entity has the option to present the total of comprehensive income, the components of net income, and the

components of other comprehensive income either in a single continuous statement of comprehensive income or in two separate but consecutive

statements. In both choices, an entity is required to present each component of net income along with total net income, each component of other

comprehensive income along with a total for other comprehensive income, and a total amount for comprehensive income. This update eliminates the

option to present the components of other comprehensive income as part of the statement of changes in stockholders' equity. The amendments in this

update do not change the items that must be reported in other comprehensive income or when an item of other comprehensive income must be

reclassified to net income, thus the adoption of such standard did not have a material impact on the Company's reported results of operations and

financial position.

In September 2011, the FASB issued new guidance on goodwill impairment testing (ASU 2011-08,

), effective for calendar years beginning after December 15, 2011. Early adoption is permitted. The objective of

this standard is to simplify how an entity tests goodwill for impairment. The amendments in this standard will allow an entity to first assess qualitative

factors to determine whether it is more likely than not that the fair value of a reporting unit is less than its carrying value as a basis for determining

whether it needs to perform the quantitative two-step goodwill impairment test. Only if an entity determines, based on qualitative assessment, that it is

more likely than not that a reporting unit's fair value is less than its carrying value will it be required to calculate the fair value of the reporting unit. The

Company adopted this guidance beginning in fiscal year 2012, and the adoption of such guidance did not have a material impact on the Company's

reported results of operations or financial position.

In July 2012, the FASB issued new guidance on the impairment testing of indefinite-lived intangible assets (ASU 2012-02,

), effective for calendar years beginning after September 15, 2012.

Early adoption is permitted. The objective of this standard is to simplify how an entity tests indefinite-lived intangible assets for impairment. The

amendments in this standard will allow an entity to first assess qualitative factors to determine whether it is more likely than not that an indefinite-lived

intangible asset is impaired as a basis for determining whether it is necessary to perform the quantitative impairment test. Only if an entity determines,

based on qualitative assessment, that it is more likely than not that the indefinite-lived intangible asset is impaired will it be required to determine the fair

value of the indefinite-lived intangible asset and perform the quantitative impairment test. The Company intends to adopt this guidance beginning in

fiscal year 2013, and the adoption of such

65

Kiosk $ 1,977 $ 1,356 $ 480 $ 72 $ 69

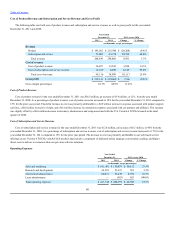

Non-Kiosk $ 15,609 $ 4,085 $ 5,646 $ 4,014 $ 1,864

Total $ 17,586 $ 5,441 $ 6,126 $ 4,086 $ 1,933