Rosetta Stone 2012 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2012 Rosetta Stone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Table of Contents

statutory carryforward periods, our experience with operating loss and tax credit carryforwards not expiring unused, and tax planning alternatives.

Significant judgment is required to determine whether a valuation allowance is necessary and the amount of such valuation allowance, if appropriate.

The valuation allowance is reviewed quarterly and is maintained until sufficient positive evidence exists to support a reversal.

When assessing the realization of our deferred tax assets, we consider all available evidence, including:

•the nature, frequency, and severity of cumulative financial reporting losses in recent years;

•the carryforward periods for the net operating loss, capital loss, and foreign tax credit carryforwards;

•predictability of future operating profitability of the character necessary to realize the asset;

•prudent and feasible tax planning strategies that would be implemented, if necessary, to protect against the loss of the deferred tax assets;

and

•the effect of reversing taxable temporary differences.

The evaluation of the recoverability of the deferred tax assets requires that we weigh all positive and negative evidence to reach a conclusion that it

is more likely than not that all or some portion of the deferred tax assets will not be realized. The weight given to the evidence is commensurate with the

extent to which it can be objectively verified. The more negative evidence that exists, the more positive evidence is necessary and the more difficult it is

to support a conclusion that a valuation allowance is not needed.

The establishment of a valuation allowance has no effect on the ability to use the deferred tax assets in the future to reduce cash tax payments. We

will continue to assess the likelihood that the deferred tax assets will be realizable at each reporting period and the valuation allowance will be adjusted

accordingly, which could materially affect our financial position and results of operations.

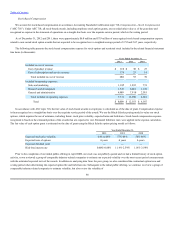

As of December 31, 2012, our net deferred tax liability was $8.1 million compared to a net deferred tax assets of $19.0 million as of December 31,

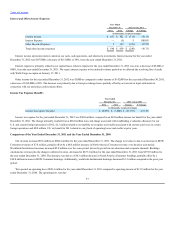

2011. During the second and third quarters of 2012, we established a valuation allowance offsetting certain deferred tax assets which resulted in a non-

cash charge in those periods of $26.0 million. Because evidence such as the Company's operating results during the most recent three-year period is

afforded more weight than forecasted results for future periods, the Company's cumulative loss in the U.S. and certain foreign jurisdictions represents

significant negative evidence in the determination of whether deferred tax assets are more likely than not to be utilized in certain jurisdictions. This

determination resulted in the need for a valuation allowance on the deferred tax assets of certain jurisdictions. We will release this valuation allowance if

and when it is determined that it is more likely than not that our deferred tax assets will be realized. Any future release of valuation allowance may be

recorded as a tax benefit increasing net income in the period of release. See additional discussion by jurisdiction below.

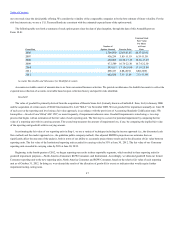

The analysis of the need for a valuation allowance on U.S. deferred tax assets as of December 31, 2012 considers our cumulative loss over our

three-year evaluation period. Consideration has also been given to the steps taken by new leadership to enhance profitability by cutting costs, the fact

that through December 31, 2012 we were ahead of forecast at the beginning of the year, the lengthy period over which these net deferred assets can be

realized, and our history of not having tax loss carryforwards in any jurisdiction expire unused. Because historical cumulative losses carry significantly

more weight than other evidence when evaluating a deferred tax assets and because the significant losses incurred, primarily in 2011 will continue to be

included in the cumulative analysis for the next several quarters, we have concluded the cumulative losses outweigh the positive evidence. As a result

49