Redbox 2010 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2010 Redbox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

Internal-Use Software

We capitalize costs incurred to develop internal-use software during the application development stage.

Capitalization of software development costs occurs after the preliminary project stage is complete, management

authorizes the project, and it is probable that the project will be completed and the software will be used for the

function intended. We expense costs incurred in the post-implementation stage for training and maintenance. A

subsequent addition, modification or upgrade to internal-use software is capitalized only to the extent that it

enables the software to perform a task it previously could not perform. The internal-use software is included in

computers and software under property and equipment. We amortize the internal-use software based on the

estimated useful life, approximately three years, on a straight-line basis.

Intangible Assets Subject to Amortization

Our intangible assets are comprised primarily of retailer relationships acquired in connection with our

acquisitions. We used expectations of future cash flows to estimate the fair value of the acquired retailer

relationships. We amortize our intangible assets on a straight-line basis over their expected useful lives, which

range from 5 to 40 years. We had no impairment to our intangible assets in 2010, 2009 or 2008.

Goodwill

Goodwill represents the excess purchase price of an acquired enterprise or assets over the estimated fair value of

identifiable net assets acquired. We test goodwill for impairment at the reporting unit level on an annual basis as

of November 30 or whenever an event occurs or circumstances change that would more likely than not reduce

the fair value of a reporting unit below its carrying amount. We perform goodwill impairment test, whereby the

first step, used to identify potential impairment, compares the fair value of a reporting unit with its carrying

amount including goodwill. If the fair value of a reporting unit exceeds its carrying amount, goodwill of the

reporting unit is considered not impaired and the second step test is not performed. The second step of the

impairment test is performed when the carrying amount of the reporting unit exceeds the fair value, then the

implied fair value of the reporting unit goodwill is compared with the carrying amount of that goodwill. If the

carrying amount of the reporting unit goodwill exceeds the implied fair value of that goodwill, an impairment

loss shall be recognized in an amount equal to that excess.

We estimate the fair value of our reporting units, DVD Services and Coin Services, using both the income and

market approaches. Our estimates of fair value can change significantly based on such factors as revenue growth

rates, profit margins, discount rates, market conditions, market prices, and changes in business strategies. As the

estimated fair value of each reporting unit exceeded its carrying value, there was no need to perform step two of

the goodwill impairment test.

Revenue from our DVD Services segment was lower in the fourth quarter of 2010 than we initially anticipated.

As a result, on January 13, 2011 we announced certain preliminary fourth quarter results and our stock price

decreased substantially. This caused us to reevaluate the fair value of the DVD Services reporting unit. In doing

so, we considered the price of our stock after the preannouncement as well as our new expectations for the

reporting unit. The results of this analysis confirmed that the fair value of our DVD Services reporting unit was

in excess of its carrying value. Also, the events in the fourth quarter of 2010 were not considered to represent a

triggering event that should cause us to reevaluate our Coin Services reporting unit because that reporting unit

continued to perform as expected during the quarter.

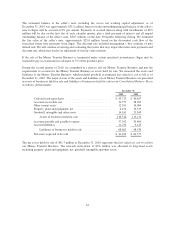

During the second quarter of 2010, our Money Transfer Business asset group met the requirements of assets held

for sale and a discontinued operation. The business assets and liabilities held for sale were reported based on the

estimated fair value less cost to sell. We used the market approach to estimate the fair value of the Money

Transfer Business. The carrying value exceeded the estimated fair value less cost to sell, accordingly, the step

one test failed. Upon conducting step two of the impairment test, the implied goodwill of the Money Transfer

55