Redbox 2010 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2010 Redbox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

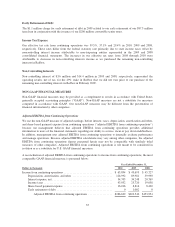

Goodwill Impairment

Goodwill represents the excess purchase price of an acquired enterprise or assets over the estimated fair value of

identifiable net assets acquired. We test goodwill for impairment at the reporting unit level on an annual basis as

of November 30 or whenever an event occurs or circumstances change that would more likely than not reduce

the fair value of a reporting unit below its carrying amount. We perform a goodwill impairment test, whereby the

first step, used to identify potential impairment, compares the fair value of a reporting unit with its carrying

amount including goodwill. If the fair value of a reporting unit exceeds its carrying amount, goodwill of the

reporting unit is considered not impaired and the second step of the test is not performed. The second step of the

impairment test is performed when the carrying amount of the reporting unit exceeds the fair value, then the

implied fair value of the reporting unit goodwill is compared with the carrying amount of that goodwill. If the

carrying amount of the reporting unit goodwill exceeds the implied fair value of that goodwill, an impairment

loss shall be recognized in an amount equal to that excess.

We estimate the fair value of our reporting units, DVD Services and Coin Services, using both the income and

market approaches. Our estimates of fair value can change significantly based on such factors as revenue growth

rates, profit margins, discount rates, market conditions, market prices, and changes in business strategies. As the

estimated fair value of each reporting unit substantially exceeded its carrying value, there was no need to perform

step two of the goodwill impairment test.

Revenue from our DVD Services segment in the fourth quarter of 2010 was lower than we initially anticipated.

As a result, on January 13, 2011, we announced certain preliminary fourth quarter results and our stock price

decreased substantially. This caused us to reevaluate the fair value of the DVD Services reporting unit. In doing

so, we considered the price of our stock after the announcement as well as our new expectations for the reporting

unit. The results of this analysis confirmed that the fair value of our DVD Services reporting unit was

substantially in excess of its carrying value. Also, the events in the fourth quarter of 2010 were not considered to

represent a triggering event that should cause us to reevaluate our Coin Services reporting unit because that

reporting unit continued to perform as expected during the quarter.

During the second quarter of 2010, our Money Transfer Business asset group met the requirements of assets held

for sale and a discontinued operation. The business assets and liabilities held for sale were reported based on the

estimated fair value less cost to sell. We used the market approach to estimate the fair value of the Money

Transfer Business. The carrying value exceeded the estimated fair value less cost to sell, accordingly, the step

one test failed. Upon conducting step two of the impairment test, the implied goodwill of our Money Transfer

Business exceeded the carrying value of its goodwill, and, accordingly, there was no goodwill impairment. We

have assessed the fair value less cost to sell and performed the goodwill impairment test each quarter thereafter

for our Money Transfer Business. During 2010, there was no goodwill impairment. In 2009, our Money Transfer

Business failed the goodwill impairment test resulting in a charge of $7.4 million in the fourth quarter of 2009,

which is included as a component of income (loss) from discontinued operations, net of tax on our Consolidated

Statements of Net Income for 2009.

DVD Library

Our DVD library consists of movie DVDs for rent or sale. We obtain our DVD library through revenue sharing

agreements, and license agreements with studios, as well as through distributors and other suppliers. The DVD

library is capitalized and amortized to its estimated salvage value as a component of direct operating expense

over the usage period of the DVDs. The cost of the DVD library mainly includes the cost of DVDs, labor,

overhead, freight, and studio revenue sharing expense. Estimated salvage value is based on the amounts that we

have historically recovered on disposal of the DVDs. For those purchased DVDs that we expect to be sold at the

end of their useful lives, an estimated salvage value is provided. For those licensed DVDs that we do not expect

to sell, no salvage value is provided. The useful lives and salvage value of our DVD library is periodically

reviewed and evaluated. The amortization charges are recorded on an accelerated basis, reflecting higher rentals

39