Oracle 2012 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2012 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

interest rates affect the interest expense that we recognize in our statements of operations. An interest rate risk

sensitivity analysis is used to measure interest rate risk by computing estimated changes in cash flows as a result

of assumed changes in market interest rates. As of May 31, 2012, if LIBOR-based interest rates increased by 100

basis points, the change would increase our interest expense annually by approximately $15 million as it relates

to our fixed to variable interest rate swap agreements.

Foreign Currency Risk

Foreign Currency Transaction Risk

We transact business in various foreign currencies and have established a program that primarily utilizes foreign

currency forward contracts to offset the risks associated with the effects of certain foreign currency exposures.

Under this program, our strategy is to enter into foreign currency forward contracts so that increases or decreases

in our foreign currency exposures are offset by gains or losses on the foreign currency forward contracts in order

to mitigate the risks and volatility associated with our foreign currency transactions. We may suspend this

program from time to time. Our foreign currency exposures typically arise from intercompany sublicense fees,

intercompany loans and other intercompany transactions that are expected to be cash settled in the near term. Our

foreign currency forward contracts are generally short-term in duration.

We neither use these foreign currency forward contracts for trading purposes nor do we designate these forward

contracts as hedging instruments pursuant to ASC 815. Accordingly, we record the fair values of these contracts as

of the end of our reporting period to our consolidated balance sheet with changes in fair values recorded to our

consolidated statement of operations. The balance sheet classification for the fair values of these forward contracts

is prepaid expenses and other current assets for a net unrealized gain position and other current liabilities for a net

unrealized loss position. The statement of operations classification for changes in fair values of these forward

contracts is non-operating income (expense), net for both realized and unrealized gains and losses.

We expect that we will continue to realize gains or losses with respect to our foreign currency exposures, net of gains

or losses from our foreign currency forward contracts. Our ultimate realized gain or loss with respect to foreign

currency exposures will generally depend on the size and type of cross-currency transactions that we enter into, the

currency exchange rates associated with these exposures and changes in those rates, the net realized gain or loss on

our foreign currency forward contracts and other factors. As of May 31, 2012 and 2011, the notional amounts of the

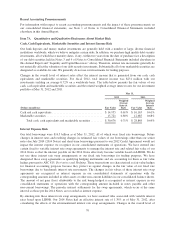

forward contracts we held to purchase U.S. Dollars in exchange for other major international currencies were $3.0

billion and $2.5 billion, respectively, and the notional amounts of forward contracts we held to sell U.S. Dollars in

exchange for other major international currencies were $873 million and $1.6 billion, respectively. The fair values of

our outstanding foreign currency forward contracts were nominal at May 31, 2012 and 2011. Net foreign exchange

transaction gains (losses) included in non-operating income (expense), net in the accompanying consolidated

statements of operations were $(105) million, $11 million and $(149) million in fiscal 2012, 2011 and 2010,

respectively. Included in the net foreign exchange transaction losses for fiscal 2010 were foreign currency losses

relating to our Venezuelan subsidiary’s operations, which are more thoroughly described under “Non-Operating

Income (Expense), net” in Management’s Discussion and Analysis of Financial Condition and Results of Operations

above. As a large portion of our consolidated operations are international, we could experience additional foreign

currency volatility in the future, the amounts and timing of which may vary.

Foreign Currency Translation Risk

Fluctuations in foreign currencies impact the amount of total assets and liabilities that we report for our foreign

subsidiaries upon the translation of these amounts into U.S. Dollars. In particular, the amount of cash, cash

equivalents and marketable securities that we report in U.S. Dollars for a significant portion of the cash held by

these subsidiaries is subject to translation variance caused by changes in foreign currency exchange rates as of

the end of each respective reporting period (the offset to which is recorded to accumulated other comprehensive

income on our consolidated balance sheet). Periodically, we may hedge net assets of certain international

subsidiaries from foreign currency exposure.

As the U.S. Dollar fluctuated against certain international currencies as of the end of fiscal 2012, the amount of

cash, cash equivalents and marketable securities that we reported in U.S. Dollars for these subsidiaries as of

May 31, 2012 decreased relative to what we would have reported using a constant currency rate as of May 31,

2011. As reported in our consolidated statements of cash flows, the estimated effect of exchange rate changes on

77