Oracle 2012 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2012 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

ORACLE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

May 31, 2012

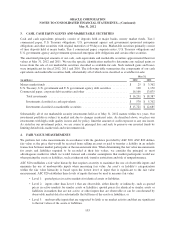

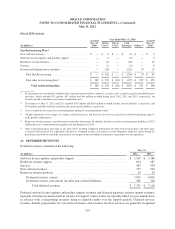

3. CASH, CASH EQUIVALENTS AND MARKETABLE SECURITIES

Cash and cash equivalents primarily consist of deposits held at major banks, money market funds, Tier-1

commercial paper, U.S. Treasury obligations, U.S. government agency and government sponsored enterprise

obligations and other securities with original maturities of 90 days or less. Marketable securities primarily consist

of time deposits held at major banks, Tier-1 commercial paper, corporate notes, U.S. Treasury obligations and

U.S. government agency and government sponsored enterprise debt obligations and certain other securities.

The amortized principal amounts of our cash, cash equivalents and marketable securities approximated their fair

values at May 31, 2012 and 2011. We use the specific identification method to determine any realized gains or

losses from the sale of our marketable securities classified as available-for-sale. Such realized gains and losses

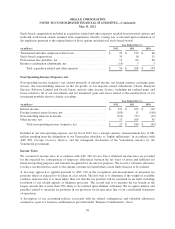

were insignificant for fiscal 2012, 2011 and 2010. The following table summarizes the components of our cash

equivalents and marketable securities held, substantially all of which were classified as available-for-sale:

May 31,

(in millions) 2012 2011

Money market funds ....................................................... $ 25 $ 3,362

U.S. Treasury, U.S. government and U.S. government agency debt securities .......... 100 1,150

Commercial paper, corporate debt securities and other ............................ 16,166 13,875

Total investments ..................................................... $ 16,291 $ 18,387

Investments classified as cash equivalents .................................. $ 570 $ 5,702

Investments classified as marketable securities .............................. $ 15,721 $ 12,685

Substantially all of our marketable security investments held as of May 31, 2012 mature within two years. Our

investment portfolio is subject to market risk due to changes in interest rates. As described above, we place our

investments with high credit quality issuers and, by policy, limit the amount of credit exposure to any one issuer.

As stated in our investment policy, we are averse to principal loss and seek to preserve our invested funds by

limiting default risk, market risk and reinvestment risk.

4. FAIR VALUE MEASUREMENTS

We perform fair value measurements in accordance with the guidance provided by ASC 820. ASC 820 defines

fair value as the price that would be received from selling an asset or paid to transfer a liability in an orderly

transaction between market participants at the measurement date. When determining the fair value measurements

for assets and liabilities required to be recorded at their fair values, we consider the principal or most

advantageous market in which we would transact and consider assumptions that market participants would use

when pricing the assets or liabilities, such as inherent risk, transfer restrictions and risk of nonperformance.

ASC 820 establishes a fair value hierarchy that requires an entity to maximize the use of observable inputs and

minimize the use of unobservable inputs when measuring fair value. An asset’s or liability’s categorization

within the fair value hierarchy is based upon the lowest level of input that is significant to the fair value

measurement. ASC 820 establishes three levels of inputs that may be used to measure fair value:

• Level 1: quoted prices in active markets for identical assets or liabilities;

• Level 2: inputs other than Level 1 that are observable, either directly or indirectly, such as quoted

prices in active markets for similar assets or liabilities, quoted prices for identical or similar assets or

liabilities in markets that are not active, or other inputs that are observable or can be corroborated by

observable market data for substantially the full term of the assets or liabilities; or

• Level 3: unobservable inputs that are supported by little or no market activity and that are significant

to the fair values of the assets or liabilities.

103