Motorola 2007 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2007 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

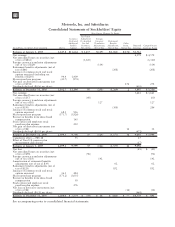

shares outstanding during the period to arrive at the basic earnings per share. Diluted earnings per share is

calculated by dividing net earnings by the sum of the weighted average number of common shares used in the basic

earnings per share calculation and the weighted average number of common shares that would be issued assuming

exercise or conversion of all potentially dilutive securities, excluding those securities that would be anti-dilutive to

the earnings (loss) per share calculation. Both basic and diluted earnings (loss) per share amounts are calculated for

earnings (loss) from continuing operations and net earnings (loss) for all periods presented.

Share-Based Compensation Costs: The Company has incentive plans that reward employees with stock

options and restricted stock, as well as an employee stock purchase plan. Prior to January 1, 2006, the Company

applied the intrinsic value method of accounting for share-based compensation. On January 1, 2006, the Company

adopted SFAS No. 123R, “Share-Based Payment” (“SFAS 123R”) using the modified prospective transition

method. The Company had previously disclosed the fair value of its stock options in its footnotes. The Company’s

consolidated financial statements for the fiscal year ending December 31, 2005 have not been restated to reflect,

and do not include, the impact of SFAS 123R. The amount of compensation cost for share-based awards is

measured based on the fair value of the awards, as determined by the Black-Scholes option pricing model, as of the

date that the share-based awards are issued and adjusted for the estimated number of awards that are expected to

vest. Compensation cost for share-based awards is recognized on a straight-line basis over the vesting period.

Retirement Benefits: The Company records annual expenses relating to its pension benefit and

postretirement plans based on calculations which include various actuarial assumptions, including discount rates,

assumed asset rates of return, compensation increases, turnover rates and health care cost trend rates. The

Company reviews its actuarial assumptions on an annual basis and makes modifications to the assumptions based

on current rates and trends. The effects of the gains, losses, and prior service costs and credits are amortized over

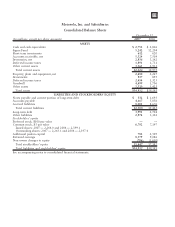

future service periods. The funding status, or projected benefit obligation less plan assets, for each plan, is reflected

in the Company’s consolidated balance sheets using a December 31 measurement date.

Advertising Expense: Advertising expenses, which are the external costs of marketing the Company’s

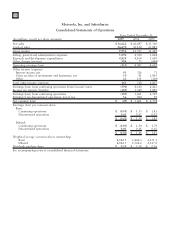

products, are expensed as incurred. Advertising expenses were $1.1 billion, $1.2 billion and $972 million for the

years ended December 31, 2007, 2006, and 2005, respectively.

Use of Estimates: The preparation of financial statements in conformity with U.S. generally accepted

accounting principles requires management to make certain estimates and assumptions that affect the reported

amounts of assets, liabilities, revenues and expenses and the disclosure of contingent assets and liabilities in the

financial statements. Actual results may differ from those estimates.

Reclassifications: Certain amounts in prior years’ financial statements and related notes have been

reclassified to conform to the 2007 presentation.

Recent Accounting Pronouncements: The Company adopted Financial Accounting Standards Board

(“FASB”) Interpretation No. 48, “Accounting for Uncertainty in Income Taxes” (“FIN 48”) effective January 1,

2007. Among other things FIN 48 prescribes a “more-likely-than-not” threshold to the recognition and de-

recognition of tax positions, provides guidance on the accounting for interest and penalties relating to tax positions

and requires that the cumulative effect of applying the provisions of FIN 48 shall be reported as an adjustment to

the opening balance of retained earnings or other appropriate components of equity or net assets in the statement

of financial position. The adoption of FIN 48 resulted in a $120 million reduction of the Company’s unrecognized

tax benefits and related interest accrual and has been reflected as an increase in the opening balance of Retained

earnings of $27 million and Additional paid-in capital of $93 million as of January 1, 2007. Upon adoption of

FIN 48, the Company also reclassified unrecognized tax benefits of $877 million from Deferred income taxes to

Other liabilities in the Company’s consolidated balance sheets.

In September 2006, the FASB issued Statement of Financial Accounting Standards (“SFAS”) No. 158,

“Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans” (“SFAS 158”). SFAS 158 has

certain recognition and disclosure requirements which the Company adopted as of December 31, 2006.

Additionally, SFAS 158 requires employers to measure defined benefit plan assets and obligations as of the date of

the statement of financial position. The measurement date provision of SFAS 158 only affects the Company’s

non-U.S. pension plans. The Company adopted the measurement date provisions for its Non-U.S. pension plans as

of December 31, 2007. Upon adoption of the measurement provisions, the Company recorded $17 million, net of

$2 million of taxes, as a decrease in the opening balance of Retained earnings at January 1, 2007 in the

consolidated statements of stockholders’ equity.

83