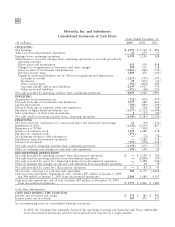

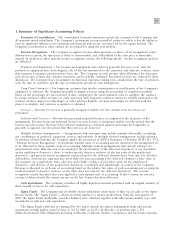

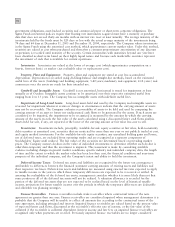

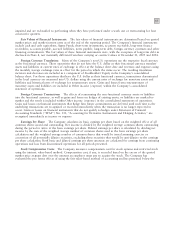

Motorola 2005 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2005 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

76

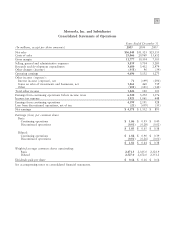

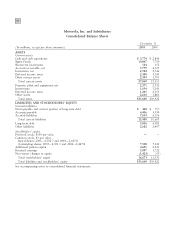

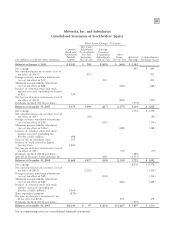

During the fourth quarter of 2005, the Company elected to settle the Variable Forwards by delivering

30.3 million shares of Sprint Nextel common stock, with a value of $725 million, to the counterparties and selling

the remaining 1.4 million Sprint Nextel common shares in the open market. The Company received aggregate cash

proceeds of $391 million and realized a loss of $70 million in connection with the settlement and sale.

Fair Value of Financial Instruments

The Company's financial instruments include cash equivalents, Sigma Funds, short-term investments, accounts

receivable, long-term finance receivables, accounts payable, accrued liabilities, notes payable, long-term debt, foreign

currency contracts and other financing commitments.

Using available market information, the Company determined that the fair value of long-term debt at

December 31, 2005 was $4.3 billion, compared to a carrying value of $4.0 billion. Since considerable judgment is

required in interpreting market information, the fair value of the long-term debt is not necessarily indicative of the

amount which could be realized in a current market exchange.

The fair values of the other financial instruments were not materially different from their carrying or contract

values at December 31, 2005.

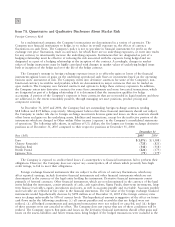

Equity Price Market Risk

At December 31, 2005, the Company's available-for-sale securities portfolio had an approximate fair market

value of $1.2 billion which represented a cost basis of $1.1 billion and a net unrealized gain of $157 million. The

value of the available-for-sale securities would change by $122 million as of year-end 2005 if the price of the stock

in each of the publicly-traded companies were to change by 10%. These equity securities are held for purposes

other than trading.

Interest Rate Risk

At December 31, 2005, the Company's short-term debt consisted primarily of $300 million of commercial

paper, priced at short-term interest rates. The Company has $4.0 billion of long-term debt, including current

maturities, which is primarily priced at long-term, fixed interest rates.

In order to manage the mix of fixed and floating rates in its debt portfolio, the Company has entered into

interest rate swaps to change the characteristics of interest rate payments from fixed-rate payments to short-term

LIBOR-based variable rate payments. During the year ended December 31, 2005, in conjunction with the repurchase

of an aggregate principal amount of $1.0 billion of long-term debt, the Company terminated a notional amount of

$1.0 billion of these swaps that were associated with the repurchased debt, resulting in expense of approximately

$22 million, which is included in debt retirement costs within Other income (expense) in the Company's

consolidated statement of operations. The following table displays the interest rate swaps that were outstanding at

December 31, 2005:

Notional Amount

Hedged Underlying Debt

Date Executed (in millions) Instrument

August 2004 $1,200 4.608% notes due 2007

September 2003 457 7.625% debentures due 2010

September 2003 600 8.0% notes due 2011

May 2003 114 6.5% notes due 2008

May 2003 84 5.8% debentures due 2008

May 2003 69 7.625% debentures due 2010

March 2002 118 7.6% notes due 2007

$2,642

The short-term LIBOR-based variable rate payments on the above interest rate swaps was 6.9% for the three

months ended December 31, 2005. The fair value of the interest rate swaps at December 31, 2005 and 2004, was

approximately $(50) million and $3 million, respectively. The fair value of the interest rate swaps would

hypothetically decrease by $35 million (i.e., would decrease from $(50) million to $(85) million) if LIBOR rates