Motorola 2005 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2005 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

|

|

119

The Company recorded approximately $93 million in goodwill, none of which was deductible for tax

purposes, a $32 million charge for acquired in-process research and development, and $54 million in other

intangibles. The acquired in-process research and development will have no alternative future uses if the products

are not feasible. At the date of the acquisition, a total of eight projects were in process. The average risk adjusted

rate used to value these projects ranged from 25% to 28%. The allocation of value to in-process research and

development was determined using expected future cash flows discounted at average risk adjusted rates reflecting

both technological and market risk as well as the time value of money. These research and development costs were

written off at the date of acquisition and have been included in Other Charges in the Company's consolidated

statements of operations. Goodwill and intangible assets are included in Other Assets in the Company's

consolidated balance sheets. The intangible assets will be amortized over periods ranging from 3 to 5 years on a

straight-line basis.

The results of operations of Winphoria have been included in the Networks segment in the Company's

consolidated financial statements subsequent to the date of acquisition. The pro forma effects of this acquisition on

the Company's consolidated financial statements were not significant.

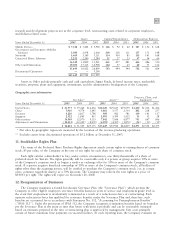

Intangible Assets

Amortized intangible assets, excluding goodwill were comprised of the following:

2005

2004

Gross

Gross

Carrying Accumulated

Carrying Accumulated

December 31

Amount Amortization

Amount Amortization

Intangible assets:

Licensed technology $113 $105 $113 $103

Completed technology 412 288 419 246

Other intangibles 152 51 76 26

$677 $444 $608 $375

Amortization expense on intangible assets was $69 million, $53 million and $101 million for the years ended

December 31, 2005, 2004 and 2003, respectively. Future amortization expense is estimated to be as follows: 2006Ì

$75 million; 2007Ì$61 million; 2008Ì$42 million; 2009Ì$30 million and 2010Ì$14 million.

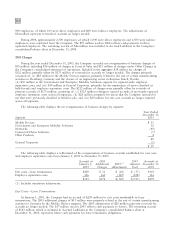

The following tables display a rollforward of the carrying amount of goodwill from January 1, 2004 to

December 31, 2005, by business segment:

January 1, December 31,

Segment 2005 Acquired Adjustments 2005

Mobile Devices $ 17 $Ì $ Ì $ 17

Government and Enterprise Mobility Solutions 257 73 (7) 323

Networks 251 Ì (18) 233

Connected Home Solutions 758 16 2 776

$1,283 $89 $(23) $1,349

January 1, December 31,

Segment 2004 Acquired Adjustments 2004

Mobile Devices $ 17 $ Ì $ Ì $ 17

Government and Enterprise Mobility Solutions 123 134 Ì 257

Networks 192 59 Ì 251

Connected Home Solutions 758 Ì Ì 758

Other 125 Ì (125) Ì

$1,215 $193 $(125) $1,283

The goodwill impairment test is performed at the reporting unit level and is a two-step analysis. First, the fair

value (FV) of each reporting unit is compared to its book value. If the FV of the reporting unit is less than its

book value, the Company performs a hypothetical purchase price allocation based on the reporting unit's fair value