Microsoft 2015 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2015 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

|

|

35

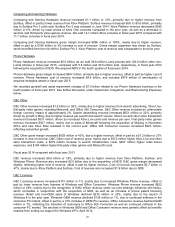

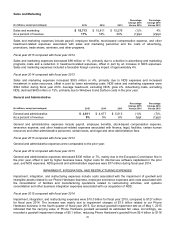

Liquidity

We earn a significant amount of our operating income outside the U.S., which is deemed to be permanently

reinvested in foreign jurisdictions. As a result, as discussed above under Cash, Cash Equivalents, and Investments,

the majority of our cash, cash equivalents, and short-term investments are held by foreign subsidiaries. We currently

do not intend nor foresee a need to repatriate these funds. We expect existing domestic cash, cash equivalents,

short-term investments, cash flows from operations, and access to capital markets to continue to be sufficient to fund

our domestic operating activities and cash commitments for investing and financing activities, such as regular

quarterly dividends, debt maturities, and material capital expenditures, for at least the next 12 months and thereafter

for the foreseeable future. In addition, we expect existing foreign cash, cash equivalents, short-term investments, and

cash flows from operations to continue to be sufficient to fund our foreign operating activities and cash commitments

for investing activities, such as material capital expenditures, for at least the next 12 months and thereafter for the

foreseeable future.

Should we require more capital in the U.S. than is generated by our operations domestically, for example to fund

significant discretionary activities, such as business acquisitions and share repurchases, we could elect to repatriate

future earnings from foreign jurisdictions or raise capital in the U.S. through debt or equity issuances. These

alternatives could result in higher effective tax rates, increased interest expense, or dilution of our earnings. We have

borrowed funds domestically and continue to believe we have the ability to do so at reasonable interest rates.

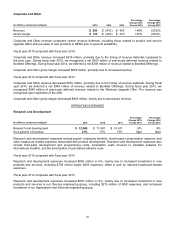

RECENT ACCOUNTING GUIDANCE

See Note 1 – Accounting Policies of the Notes to Financial Statements for further discussion.

APPLICATION OF CRITICAL ACCOUNTING POLICIES

Our consolidated financial statements and accompanying notes are prepared in accordance with U.S. GAAP.

Preparing consolidated financial statements requires management to make estimates and assumptions that affect

the reported amounts of assets, liabilities, revenue, and expenses. These estimates and assumptions are affected by

management’s application of accounting policies. Critical accounting policies for us include revenue recognition,

impairment of investment securities, goodwill, research and development costs, contingencies, income taxes, and

inventories.

Revenue Recognition

Revenue recognition for multiple-element arrangements requires judgment to determine if multiple elements exist,

whether elements can be accounted for as separate units of accounting, and if so, the fair value for each of the

elements.

Judgment is also required to assess whether future releases of certain software represent new products or upgrades

and enhancements to existing products. Certain volume licensing arrangements include a perpetual license for

current products combined with rights to receive unspecified future versions of software products and are accounted

for as subscriptions, with billings recorded as unearned revenue and recognized as revenue ratably over the

coverage period.

Software updates are evaluated on a case-by-case basis to determine whether they meet the definition of an

upgrade, which may require revenue to be deferred and recognized when the upgrade is delivered. If it is determined

that implied post-contract customer support (“PCS”) is being provided, revenue from the arrangement is deferred and

recognized over the implied PCS term. If updates are determined to not meet the definition of an upgrade, revenue is

generally recognized as products are shipped or made available.

Microsoft enters into arrangements that can include various combinations of software, services, and hardware.

Where elements are delivered over different periods of time, and when allowed under U.S. GAAP, revenue is

allocated to the respective elements based on their relative selling prices at the inception of the arrangement, and

revenue is recognized as each element is delivered. We use a hierarchy to determine the fair value to be used for

allocating revenue to elements: (i) vendor-specific objective evidence of fair value (“VSOE”), (ii) third-party evidence,

and (iii) best estimate of selling price (“ESP”). For software elements, we follow the industry specific software

guidance which only allows for the use of VSOE in establishing fair value. Generally, VSOE is the price charged

when the deliverable is sold separately or the price established by management for a product that is not yet sold if it

is probable that the price will not change before introduction into the marketplace. ESPs are established as best

estimates of what the selling prices would be if the deliverables were sold regularly on a stand-alone basis. Our