MasterCard 2013 Annual Report Download - page 22

Download and view the complete annual report

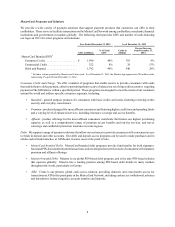

Please find page 22 of the 2013 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

18

resources to the defense of interchange fees in regulatory proceedings, litigation and legislative activity. The potential

outcome of any legislative, regulatory or litigation action could have a more positive or negative impact on MasterCard

relative to its competitors. If we are ultimately unsuccessful in our defense of interchange fees, any such legislation,

regulation and/or litigation may have a material adverse impact on our overall business and results of operations. In

addition, regulatory proceedings and litigation could result in MasterCard being fined and/or having to pay civil damages.

The Dodd-Frank Act may have a material adverse impact on our overall business and results of operations.

The Dodd-Frank Act enacted in the United States includes provisions that provide for the regulation by the Federal

Reserve of debit and prepaid interchange fees and certain other network industry practices. Among other things, it

requires debit and prepaid “interchange transaction fees” (referred to in the Dodd-Frank Act as fees established, charged

or received by a payment card network for the purpose of compensating an issuer for its involvement in an electronic

debit transaction) to be “reasonable and proportional to the cost incurred by the issuer with respect to the transaction.”

Additionally, it provides that neither an issuer nor a payment card network may establish exclusive network arrangements

for debit or prepaid cards or inhibit the ability of a merchant to choose among different networks for routing debit or

prepaid transactions.

The Federal Reserve regulations implementing these provisions limit per-transaction U.S. debit and prepaid interchange

fees to 21 cents plus five basis points. The issuer may receive a fraud prevention adjustment of an additional one cent

if it meets certain requirements. The regulations contain exemptions from the interchange limitations for issuers that,

together with their affiliates, have less than $10 billion in assets, as well as for debit cards issued pursuant to a government-

administered payment program and certain reloadable prepaid cards. Also, while the regulations do not directly regulate

network fees, they make clear that network fees cannot be used to circumvent the interchange fee restrictions. See our

risk factor in “Risk Factors - Legal and Regulatory Risks” in this Part I, Item 1A with respect to interchange fees and

related practices receiving significant and increasingly intense legal, regulatory and legislative scrutiny worldwide.

Issuers and networks are required to file various types of information regarding debit and prepaid transactions with the

Federal Reserve periodically, and such information could be used by the Federal Reserve to reexamine and potentially

re-set the interchange cap. With respect to network arrangements and transaction routing, the regulations require debit

and prepaid cards to be enabled with two unaffiliated payments networks. The regulations also provide that an issuer

or payments network may not inhibit the ability of any person that accepts or honors a debit or prepaid card to direct

the routing of the card transaction for processing over any network enabled on the card.

In July 2013, the U.S. District Court for the District of Columbia (the “District Court”) granted summary judgment in

favor of a group of retailers and retailer trade associations, overturning these Federal Reserve regulations with regard

to interchange fees and network non-exclusivity. The District Court’s decision requires the Federal Reserve to revise

its regulations to consider only incremental authorization, clearing and settlement costs in determining the level of

interchange fees, as well as require two unaffiliated networks for routing transactions for each authentication method

(PIN and signature). The Federal Reserve has appealed the decision to the U.S. Court of Appeals for the District of

Columbia Circuit (the “Appellate Court”) and the District Court has issued an order staying its decision pending this

appeal. As a result, the Federal Reserve’s debit interchange regulations remain in effect until the appellate process is

completed. The Appellate Court has granted a motion to expedite the Federal Reserve’s appeal and a decision is expected

in 2014. If the District Court’s ruling is upheld, the Federal Reserve would be required to revise its regulations in

accordance with the ruling. It is not clear at what level the Federal Reserve would set the interchange fees, although,

based on the decision, the level of interchange fees likely would be significantly reduced.

The CFPB and FSOC were both created under the Dodd-Frank Act. The CFPB has significant authority to regulate

consumer financial products, although it is not clear whether and/or to what extent it will regulate broader aspects of

payment card networks. The FSOC is tasked with identifying payment, clearing and settlement systems that are

“systemically important”. If MasterCard were designated “systemically important”, it would be subject to new risk

management regulations relating to its payment, clearing and settlement activities. New regulations could address

areas such as risk management policies and procedures; collateral requirements; participant default policies and

procedures; the ability to complete timely clearing and settlement of financial transactions; and capital and financial

resource requirements. Also, a “systemically important” payments system could be required to obtain prior approval

from the Federal Reserve or another federal agency for changes to its system rules, procedures or operations that could

materially affect the level of risk presented by that payments system. These developments or actions could increase