MasterCard 2013 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2013 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

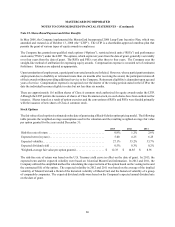

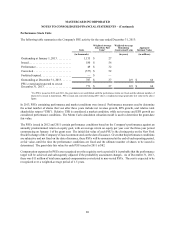

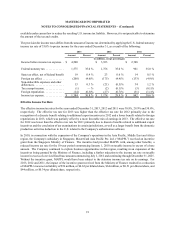

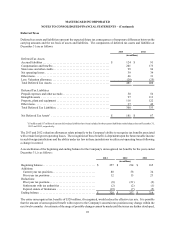

MASTERCARD INCORPORATED

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (Continued)

96

In October 2012, the parties entered into a definitive settlement agreement with respect to the merchant class litigation

and the defendants separately entered into a settlement agreement with the individual merchant plaintiffs (the terms of

which were consistent with a memorandum of understanding that was executed by the parties in July 2012). The

settlements included cash payments that were apportioned among the defendants pursuant to the omnibus judgment

sharing and settlement sharing agreement described above. MasterCard also agreed to provide class members with a

short-term reduction in default credit interchange rates and to modify certain of its business practices, including its No

Surcharge Rule. The court granted final approval of the settlement in December 2013, which has been appealed by

objectors to the settlement.

Merchants representing slightly more than 25% of the MasterCard and Visa purchase volume over the relevant period

chose to opt out of the class settlement. MasterCard anticipates that most of the larger merchants who opted out of the

settlement will initiate separate actions seeking to recover damages, and over 25 opt-out complaints have been filed

on behalf of numerous merchants in various jurisdictions. Those cases are in the early stages and the defendants have

consolidated all of these matters (except for one state court action) in front of the same court that is overseeing the

approval of the settlement. In addition, certain competitors have raised objections to the settlement, including Discover.

Discover’s objections include a challenge to the settlement on the grounds that certain of the rule changes agreed to in

the settlement constitute a restraint of trade in violation of Section 1 of the Sherman Act.

MasterCard recorded a pre-tax charge of $770 million in the fourth quarter of 2011 and an additional $20 million pre-

tax charge in the second quarter of 2012 relating to the settlement agreements described above. In 2012, MasterCard

paid $790 million with respect to the settlements, of which $726 million was paid into a qualified cash settlement fund

related to the merchant class litigation. At December 31, 2013, MasterCard had $723 million in the qualified cash

settlement fund classified as restricted cash on its balance sheet. The class settlement agreement provided for a return

to the defendants of a portion of the class cash settlement fund based upon the percentage of purchase volume represented

by the opt out merchants. This resulted in $164 million from the cash settlement fund being returned to MasterCard

in January 2014 and reclassified at that time from restricted cash to cash and cash equivalents. In the fourth quarter of

2013, MasterCard recorded an incremental net pre-tax charge of $95 million related to these opt out merchants,

representing a change in its estimate of possible losses relating to these matters. Accordingly, as of December 31, 2013,

MasterCard had accrued a liability of $818 million as a reserve for both the merchant class litigation and the filed and

anticipated opt out merchant cases.

The portion of the accrued liability relating to the opt out merchants does not represent an estimate of a loss, if any, if

the opt out merchant matters were litigated to a final outcome, in which case MasterCard cannot estimate the potential

liability. MasterCard’s estimate involves significant judgment and may change depending on progress in settlement

negotiations or depending upon decisions in any opt out merchant cases. In addition, in the event that the merchant

class litigation settlement approval is overturned on appeal, a negative outcome in the litigation could have a material

adverse effect on MasterCard’s results of operations, financial position and cash flows.

Canada. In December 2010, the Canadian Competition Bureau (the “CCB”) filed an application with the Canadian

Competition Tribunal to strike down certain MasterCard rules related to point-of-sale acceptance, including the “honor

all cards” and “no surcharge” rules. In July 2013, the Competition Tribunal issued a decision in MasterCard’s favor

and dismissed the CCB’s application, which was not appealed. In December 2010, a complaint styled as a class action

lawsuit was commenced against MasterCard in Quebec on behalf of Canadian merchants. That suit essentially repeated

the allegations and arguments of the CCB application to the Canadian Competition Tribunal and sought compensatory

and punitive damages in unspecified amounts, as well as injunctive relief. In March 2011, a second purported class

action lawsuit was commenced in British Columbia against MasterCard, Visa and a number of large Canadian financial

institutions, and in May 2011 a third purported class action lawsuit was commenced in Ontario against the same

defendants. These suits allege that MasterCard, Visa and the financial institutions have engaged in a conspiracy to

increase or maintain the fees paid by merchants on credit card transactions and establish rules which force merchants

to accept all MasterCard and Visa credit cards and prevent merchants from charging more for payments with MasterCard

and Visa premium cards. The British Columbia suit seeks compensatory damages in unspecified amounts, and the

Ontario suit seeks compensatory damages of $5 billion. The British Columbia and Ontario suits also seek punitive