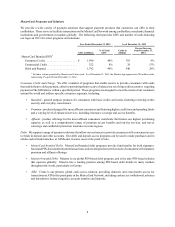

MasterCard 2013 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2013 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

13

and Bankserv in South Africa. In addition, in many countries outside of the United States, local debit brands

serve as the main brands while our brands are used mostly to enable cross-border transactions, which typically

represent a small portion of overall transaction volume.

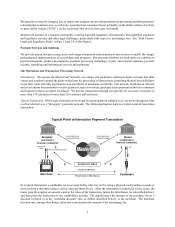

• End-to-End Payments Networks. Our competitors include operators of proprietary end-to-end payments

networks, such as American Express and Discover, that have direct acquiring relationships with merchants

and direct issuing relationships with account holders. These competitors have certain competitive advantages

over four-party payments systems such as ours. Among other things, these networks do not require formal

interchange fees to balance payment system costs between the issuing and acquiring sides of their business,

even though they have the ability to internally transfer costs in a manner similar to interchange fees. As a

result, to date, operators of end-to-end payments networks have generally avoided the same regulatory and

legislative scrutiny and litigation challenges we face.

• Competition for Customer Business. We compete intensely with other payments networks for customer

business. Globally, financial institutions typically issue both MasterCard and Visa-branded payment products,

and we compete with Visa for business on the basis of individual portfolios or programs. In addition, a number

of our customers issue American Express and/or Discover-branded payment cards in a manner consistent

with a four-party system. We continue to face intense competitive pressure on the prices we charge our issuers

and acquirers, and we seek to enter into business agreements with them through which we offer incentives

and other support to issue and promote our payment products. We also compete for non-financial institution

partners, such as merchants, governments and telecommunication companies.

• Third-Party Processors. We face competition, and potential displacement, from transaction processors

throughout the world, such as First Data Corporation and Total System Services, Inc., which are seeking to

enhance their networks that link issuers directly with point-of-sale devices for payment transaction

authorization and processing services.

• Alternative Payments Systems and New Entrants. As the global payments industry becomes more complex,

we may face increasing competition from emerging payment providers, including networks and others that

have developed less traditional payment models. Many of these networks have developed payments systems

focused on online activity in e-commerce and mobile channels, however they either have or may expand to

other channels. These competitors include digital wallet providers such as PayPal®, Google and Amazon,

mobile operators such as Isis, handset manufacturers, and social networks such as Facebook®. We compete

with these providers in some circumstances, but in some cases they may also be our customers or partner

with us.

We compete successfully as a technology-driven company that operates a global payments network within the four-

party model, providing a critical link between consumers, financial institutions, businesses and merchants worldwide.

We offer secure, unsurpassed acceptance via a highly-adaptable network that is the world's fastest. We maintain and

grow our leadership position in payments with the adoption of innovative products and platforms like MasterPass and

MasterCard inControl® (our platform featuring an array of advanced authorization, transaction routing and alert

controls). We are at the forefront of the effort to reduce the incidence of fraud in global payments, leading industry

efforts such as EMV migration and tokenization. Our MasterCard Advisors group is a professional services organization

dedicated solely to the payments industry. Our expanded on-soil presence in individual markets and a heightened focus

on working with governments has improved our ability to serve a broad array of participants in global payments.

Government Regulation

General. Government regulation impacts key aspects of our business. We are subject to regulations that affect the

payments industry in the many countries in which our cards and payment devices are used. See “Risk Factors-Legal

and Regulatory Risks” in Part I, Item 1A of this Report.