Lexmark 2008 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2008 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

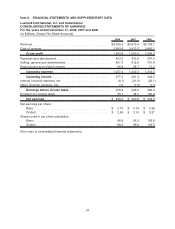

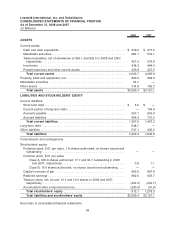

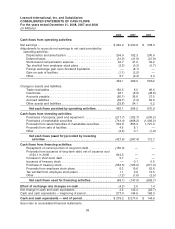

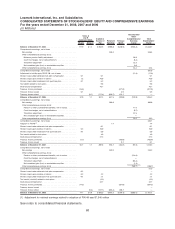

Senior Notes — Long-term Debt and Current Portion of Long-term Debt

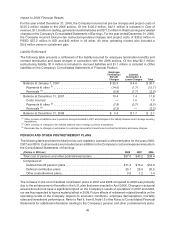

In May 2008, the Company repaid its $150 million principal amount of 6.75% senior notes that were due on

May 15, 2008. Additionally, in May 2008, the Company completed a public debt offering of $650 million

aggregate principal amount of fixed rate senior unsecured notes. The notes are split into two tranches of

five- and ten-year notes respectively. The five-year notes with an aggregate principal amount of $350 million

and 5.9% coupon were priced at 99.83% to have an effective yield to maturity of 5.939% and will mature

June 1, 2013 (referred to as the “2013 senior notes”). The ten-year notes with an aggregate principal amount

of $300 million and 6.65% coupon were priced at 99.73% to have an effective yield to maturity of 6.687% and

will mature June 1, 2018 (referred to as the “2018 senior notes”). At December 31, 2008, the outstanding

balance was $648.7 million (net of unamortized discount of $1.3 million).

The 2013 and 2018 senior notes (collectively referred to as the “senior notes”) pay interest on June 1 and

December 1 of each year, beginning December 1, 2008. The interest rate payable on the notes of each

series will be subject to adjustments from time to time if either Moody’s Investors Service, Inc. or Standard

and Poor’s Ratings Services downgrades the debt rating assigned to the notes to a level below investment

grade, or subsequently upgrades the ratings.

The senior notes contain typical restrictions on liens, sale leaseback transactions, mergers and sales of

assets. There are no sinking fund requirements on the senior notes and they may be redeemed at any time

at the option of the Company, at a redemption price as described in the related indenture agreement, as

supplemented and amended, in whole or in part. If a “change of control triggering event” as defined below

occurs, the Company will be required to make an offer to repurchase the notes in cash from the holders at a

price equal to 101% of their aggregate principal amount plus accrued and unpaid interest to, but not

including, the date of repurchase. A “change of control triggering event” is defined as the occurrence of

both a change of control and a downgrade in the debt rating assigned to the notes to a level below

investment grade.

The Company intends to use the net proceeds from the offering for general corporate purposes, including

to fund share repurchases, repay debt, finance acquisitions, finance capital expenditures and operating

expenses and invest in any subsidiaries.

Additional Sources of Liquidity

Credit Facility

Effective January 20, 2005, Lexmark entered into a $300 million 5-year senior, unsecured, multi-currency

revolving credit facility with a group of banks. Under the credit facility, the Company may borrow in

U.S. dollars, euros, British pounds sterling and Japanese yen. As of December 31, 2008 and 2007, there

were no amounts outstanding under the credit facility.

Lexmark’s credit agreement contains usual and customary default provisions, leverage and interest

coverage restrictions and certain restrictions on secured and subsidiary debt, disposition of assets, liens

and mergers and acquisitions. The $300 million credit facility has a maturity date of January 20, 2010.

Interest on all borrowings under the facility depends upon the type of loan, namely alternative base rate

loans, swingline loans or eurocurrency loans. Alternative base rate loans bear interest at the greater of the

prime rate or the federal funds rate plus one-half of one percent. Swingline loans (limited to $50 million)

bear interest at an agreed upon rate at the time of the borrowing. Eurocurrency loans bear interest at the

sum of (i) a LIBOR for the applicable currency and interest period and (ii) an interest rate spread based

upon the Company’s debt ratings ranging from 0.18% to 0.80%. In addition, Lexmark is required to pay a

facility fee on the $300 million line of credit of 0.07% to 0.20% based upon the Company’s debt ratings. The

interest and facility fees are payable at least quarterly.

52