Lexmark 2008 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2008 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Consolidated Statements of Financial Position, with changes in its fair value recognized in current period

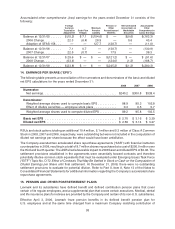

earnings. An immaterial portion of the Company’s cash flow hedges was determined to be ineffective, and

recognized in current period earnings during 2007 and 2006.

Lexmark recorded $18.5 million, $8.2 million and $4.6 million of aggregate net foreign currency transaction

losses in 2008, 2007 and 2006, respectively. The aggregate foreign currency transaction net loss amounts

include the gains/losses on the Company’s foreign currency fair value hedges for all periods presented.

Financial Instruments

In May 2008, the Company repaid its $150.0 million principal amount of 6.75% senior notes that were due

on May 15, 2008. Additionally, in May 2008, the Company completed a public debt offering of

$650.0 million aggregate principal amount of fixed rate senior unsecured notes. As of December 31,

2008, the carrying value of Lexmark’s $650.0 million of senior note debt was $648.7 million and the fair

value was $505.0 million. The fair value of the debt was estimated based on current rates available to the

Company for debt with similar characteristics. As of December 31, 2007, the carrying value of Lexmark’s

$150.0 million of senior note debt was $149.9 million and the fair value was $150.3 million. The fair value of

the debt was estimated based on current rates available to the Company for debt with similar

characteristics. As the notes matured in May 2008, the senior notes were reclassified from Long-term

debt to Current portion of long-term debt during 2007. As of December 31, 2008, the carrying value of the

company’s short-term debt was $5.5 million, which approximated its fair value. As of December 31, 2007,

the Company had no short-term debt outstanding.

During October 2003, Lexmark entered into interest rate swap contracts to convert its $150.0 million

principal amount of 6.75% senior notes from a fixed interest rate to a variable interest rate. The interest rate

swaps were designated as a fair value hedge of the Company’s $150.0 million long-term debt. The interest

rate swaps were recorded at their fair value and the Company’s long-term debt was adjusted by the same

corresponding value in accordance with the short-cut method of SFAS 133. The fair value of the interest

rate swaps was combined with the fair value adjustment of the Company’s senior note debt due to

immateriality and was presented in Current portion of long-term debt at December 31, 2007 on the

Consolidated Statements of Financial Position. In May 2008, the interest rate swap contracts expired

concurrently with the repayment of the $150.0 million debt. As of December 31, 2007, the fair value of the

interest rate swap contracts was an asset of $0.1 million.

Concentrations of Risk

Lexmark’s main concentrations of credit risk consist primarily of short-term cash investments, marketable

securities and trade receivables. Short-term cash and marketable securities investments are made in a

variety of high quality securities with prudent diversification requirements. The Company seeks

diversification among its cash investments by limiting the amount of cash investments that can be

made with any one obligor. Credit risk related to trade receivables is dispersed across a large number

of customers located in various geographic areas. Collateral such as letters of credit and bank guarantees

is required in certain circumstances. Lexmark sells a large portion of its products through third-party

distributors and resellers and original equipment manufacturer (“OEM”) customers. If the financial

condition or operations of these distributors, resellers and OEM customers were to deteriorate

substantially, the Company’s operating results could be adversely affected. The three largest

distributor, reseller and OEM customer trade receivable balances collectively represented $188 million

or approximately 30% of total trade receivables at December 31, 2008, and $281 million or approximately

46% of total trade receivables at December 31, 2007, of which Dell receivables were $125 million or

approximately 20% of total trade receivables at December 31, 2008, and $207 million or approximately

34% of total trade receivables at December 31, 2007. However, Lexmark performs ongoing credit

evaluations of the financial position of its third-party distributors, resellers and other customers to

determine appropriate credit limits.

100