Lexmark 2008 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2008 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

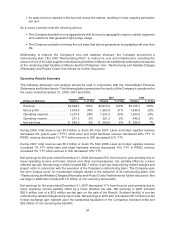

experiencing in its OEM business. The Company continues to invest in its core print technologies and

product development that is expected to drive a strong pipeline of future Lexmark products.

2007

Beginning in the second quarter of 2007, ISD experienced on-going declines in inkjet supplies and OEM

unit sales, lower average unit revenues (“AURs”) and additional costs in its new products. As the Company

analyzed the situation, it saw that some of its unit sales were not generating adequate lifetime profitability,

some markets and channels were on the low-end of the supplies generation distribution curve and its sales

were too skewed to the low-end versus the market.

As a result, the Company decided to more aggressively shift the Company’s focus to geographic regions,

market segments, and customers that generate higher page usage and minimize the unit sales that do not

generate an acceptable profit over their life.

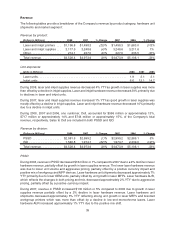

Refer to the section entitled “RESULTS OF OPERATIONS” that follows for a further discussion of the

Company’s results of operations.

Trends and Opportunities

Lexmark management believes that the total distributed output opportunity was between $90 and

$100 billion in 2008, including hardware, supplies and related software and services. This opportunity

includes printers and multifunction devices as well as a declining base of copiers and fax machines that are

increasingly being integrated into multifunction devices. Based on industry information, Lexmark

management estimates that the market may have declined slightly in 2008 and may decline again in

2009 due to the severe global economic slowdown. When global economic growth resumes, perhaps in

2010, the industry could again experience low to mid-single digit annual revenue growth rates with highest

growth likely to be in MFPs and related software solutions and services and emerging economies.

Market trends driving long-term growth include:

• Continuing improvement in price/performance points;

• Increased adoption of color and graphics output in business;

• Advancements in electronic movement of information, driving more pages to be printed by end

users when and where it is convenient to do so;

• Continued convergence in technology between printers, scanners, copiers and fax machines into

single, integrated AIO devices; and

• Advancements in digital photography driving the opportunity to print digital images on distributed

output devices.

As a result of these market trends, Lexmark has growth opportunities in monochrome laser printers, color

lasers, laser MFPs and inkjet AIOs.

Industry laser printer unit growth in recent years has generally exceeded the growth rate of laser printer

revenue due to unit growth in lower-priced desktop color and monochrome laser printers and unit price

reductions. Additionally, color and multifunction laser printer units represent a more significant component

of laser unit growth. Management believes these trends will continue. Product pricing pressure is partially

offset by the tendency of customers in the shared workgroup laser market to add higher profit margin

optional features.

In the inkjet product market, advances in inkjet technology have resulted in products with higher resolution

and improved performance while increased competition has led to lower prices. Also, there is an increasing

trend in inkjet products being designed for SOHO and small business. Additionally, over the past couple of

years, the number of customers seeking productivity-related features has driven significant growth in AIO

products. Key factors promoting this trend are greater affordability of AIOs containing productivity features.

25