LensCrafters 2007 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2007 LensCrafters annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

NOTES TO CONSOLIDATED

FINANCIAL STATEMENTS | 143 <

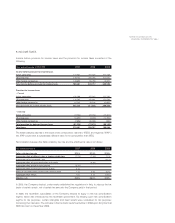

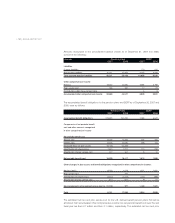

8. INCOME TAXES

Income before provision for income taxes and the provision for income taxes consisted of the

following:

The Italian statutory tax rate is the result of two components: national (“IRES”) and regional (“IRAP”)

tax. IRAP could have a substantially different base for its computation than IRES.

Reconciliation between the Italian statutory tax rate and the effective tax rate is as follows:

In 2005, the Company elected, under newly established tax regulations in Italy, to step-up the tax

basis of certain assets, net of certain tax amounts the Company paid in that period.

In 2006, the Australian subsidiaries of the Company elected to apply a new tax consolidation

regime, which was introduced by the Australian government. By electing such new consolidation

regime for tax purposes, certain intangible and fixed assets were revaluated for tax purposes

increasing their tax basis. The increase in the tax basis became effective in 2006 upon filing the final

2005 tax return in December 2006.

Years ending December 31 (Euro/000) 2007 2006 2005

Income before provision for income taxes

Italian companies 317,637 251,343 216,438

US companies 319,154 331,035 244,050

Other foreign companies 143,890 95,799 78,821

Total income before provision for income taxes 780,681 678,177 539,309

Provision for income taxes

• Current

Italian companies 156,198 157,342 127,730

US companies 116,785 120,681 120,784

Other foreign companies 61,742 33,206 40,855

Total provision for current income taxes 334,725 311,229 289,369

• Deferred

Italian companies (47,736) (23,016) (74,874)

US companies (10,592) (3,392) (14,295)

Other foreign companies (2,896) (46,065) (934)

Total provision for deferred income taxes (61,224) (72,473) (90,103)

Total taxes 273,501 238,757 199,266

Year ended December 31 2007 2006 2005

Italian statutory tax rate 37.3% 37.3% 37.3%

Aggregate effect of different rates in foreign jurisdictions (1.7%) (1.5%) 1.7%

Aggregate Italian tax benefit - net (4.1%)

Aggregate effect of asset revaluation in Australia (6.8%)

Aggregate effect of Italian restructuring (5.3%)

Aggregate effect of change in tax law in Italy 2.1%

Effect of non-deductible stock-based compensation 1.1% 5.5% 3.0%

Aggregate other effects 1.5% 0.7% (0.9%)

Effective rate 35.0% 35.2% 37.0%