Kia 2015 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2015 Kia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

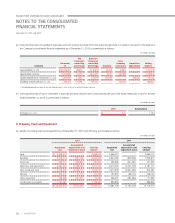

(y) Income taxes

Income tax expense comprises current and deferred tax. Current tax and deferred tax are recognized in profit or loss except to the extent that it

relates to a business combination, or items recognized directly in equity or in other comprehensive income.

Current tax

Current tax is the expected tax payable or receivable on the taxable profit or loss for the year, using tax rates enacted or substantively enacted at the

end of the reporting period and any adjustment to tax payable in respect of previous years. The taxable profit is different from the accounting profit

for the period since the taxable profit is calculated excluding the temporary differences, which will be taxable or deductible in determining taxable

profit (tax loss) of future periods, and non-taxable or non-deductible items from the accounting profit.

Deferred tax

Deferred tax is recognized, using the asset-liability method, in respect of temporary differences between the carrying amounts of assets and liabilities

for financial reporting purposes and the amounts used for taxation purposes. A deferred tax liability is recognized for all taxable temporary differences.

A deferred tax asset is recognized for all deductible temporary differences to the extent that it is probable that taxable profit will be available against

which they can be utilized. However, deferred tax is not recognized for the following temporary differences: taxable temporary differences arising on

the initial recognition of goodwill, or the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects

neither accounting profit or loss nor taxable income.

The Company recognizes a deferred tax liability for all taxable temporary differences associated with investments in subsidiaries, associates and

interests in joint ventures, except to the extent that the Company is able to control the timing of the reversal of the temporary difference and it is

probable that the temporary difference will not reverse in the foreseeable future. The Company recognizes a deferred tax asset for all deductible

temporary differences arising from investments in subsidiaries and associates, to the extent that it is probable that the temporary difference will reverse

in the foreseeable future and taxable profit will be available against which the temporary difference can be utilized.

The carrying amount of a deferred tax asset is reviewed at the end of each reporting period and reduces the carrying amount to the extent that it is no

longer probable that sufficient taxable profit will be available to allow the benefit of part or all of that deferred tax asset to be utilized.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset is realized or the liability is

settled, based on tax laws that have been enacted or substantively enacted by the end of the reporting period. The measurement of deferred tax

liabilities and deferred tax assets reflects the tax consequences that would follow from the manner in which the Company expects, at the end of the

reporting period to recover or settle the carrying amount of its assets and liabilities.

Deferred tax assets and liabilities are offset only if there is a legally enforceable right to offset the related current tax liabilities and assets, and they

relate to income taxes levied by the same tax authority and they intend to settle current tax liabilities and assets on a net basis.

(z) Earnings per share

The Company presents basic and diluted earnings per share (EPS) data for its ordinary shares. Basic EPS is calculated by dividing the profit or loss

attributable to ordinary shareholders of the Parent Company by the weighted average number of ordinary shares outstanding during the period,

adjusted for own shares held. Diluted EPS is determined by adjusting the profit or loss attributable to ordinary shareholders and the weighted average

number of ordinary shares outstanding, adjusted for own shares held, for the effects of all potential dilutive ordinary shares.

(

aa

) Operating segments

An operating segment is a component of the Company that: 1) engages in business activities from which it may earn revenues and incur expenses,

including revenues and expenses that relate to transactions with other components of the Company, 2) whose operating results are reviewed regularly

by the Company’s chief operating decision maker (‘CODM’) in order to allocate resources and assess its performance, and 3) for which discrete

financial information is available.

75

ANNUAL REPORT 2015 |