Kia 2015 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2015 Kia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

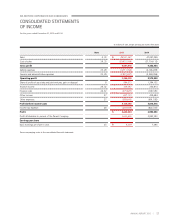

|

|

Non-controlling interests

Non-controlling interests in a subsidiary are accounted for separately from the Company’s ownership interests in a subsidiary. Each component of

net profit or loss and other comprehensive income is attributed to the owners of the Company and non-controlling interest holders, even when

the allocation reduces the non-controlling interest balance below zero.

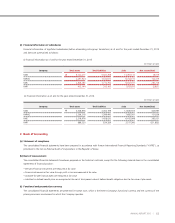

Changes in the Company’s ownership interest in a subsidiary

Changes in the Company’s ownership interest in a subsidiary that do not result in a loss of control are accounted for as equity transactions

with owners in their capacity as owners. Adjustments to non-controlling interests are based on a proportionate amount of the net assets of

the subsidiary. The difference between the consideration and the adjustments made to non-controlling interest is recognized directly in equity

attributable to the owners of the Company.

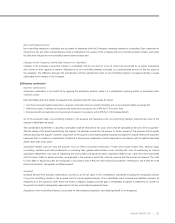

(b) Business combination

Business combination

A business combination is accounted for by applying the acquisition method, unless it is a combination involving entities or businesses under

common control.

Each identifiable asset and liability is measured at its acquisition-date fair value except for below:

• Onlythosecontingentliabilitiesassumedinabusinesscombinationthatareapresentobligationandcanbemeasuredreliablyarerecognized

• DeferredtaxassetsorliabilitiesarerecognizedandmeasuredinaccordancewithK-IFRSNo.1012Income Taxes

• EmployeebenetarrangementsarerecognizedandmeasuredinaccordancewithK-IFRSNo.1019Employee Benefits

As of the acquisition date, non-controlling interests in the acquiree are measured as the non-controlling interests’ proportionate share of the

acquiree’s identifiable net assets.

The consideration transferred in a business combination shall be measured at fair value, which shall be calculated as the sum of the acquisition-

date fair values of the assets transferred by the acquirer, the liabilities incurred by the acquirer to former owners of the acquiree and the equity

interests issued by the acquirer. However, any portion of the acquirer’s share-based payment awards exchanged for awards held by the acquiree’s

employees that is included in consideration transferred in the business combination shall be measured in accordance with the method described

above rather than at fair value.

Acquisition-related costs are costs the acquirer incurs to effect a business combination. Those costs include finder’s fees; advisory, legal,

accounting, valuation and other professional or consulting fees; general administrative costs, including the costs of maintaining an internal

acquisitions department; and costs of registering and issuing debt and equity securities. Acquisition-related costs, other than those associated

with the issue of debt or equity securities, are expensed in the periods in which the costs are incurred and the services are received. The costs

to issue debt or equity securities are recognized in accordance with K-IFRS No.1032

Financial Instruments: Presentation

and K-IFRS No.1039

Financial Instruments: Recognition and Measurement.

Goodwill

Goodwill derived from business combinations occurred is as the fair value of the consideration transferred including the recognized amount

of any non-controlling interest in the acquiree, less the net recognized amount of the identifiable assets acquired and liabilities assumed, all

measured as of the acquisition date. When the excess is negative, bargain purchase gain is immediately recognize in statements of income for

the period. Goodwill is subsequently measured at cost less accumulated impairment losses.

Acquisition of non-controlling interests is accounted for intercompany transaction, and related goodwill is not recognized.

65

ANNUAL REPORT 2015 |