Honeywell 2006 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2006 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

|

|

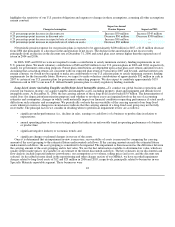

acquisition, second to reduce to zero other non-current intangible assets related to the acquisition, and third to reduce income tax

expense.

Significant judgment is required in determining income tax provisions under Statement of Financial Accounting Standards

No. 109 “Accounting for Income Taxes” (SFAS No. 109) and in evaluating tax positions. We establish additional provisions for

income taxes when, despite the belief that tax positions are fully supportable, there remain certain positions that are likely to be

challenged and that may not be sustained on review by tax authorities. In the normal course of business, the Company and its

subsidiaries are examined by various Federal, State and foreign tax authorities. We regularly assess the potential outcomes of these

examinations and any future examinations for the current or prior years in determining the adequacy of our provision for income

taxes. We continually assess the likelihood and amount of potential adjustments and adjust the income tax provision, the current tax

liability and deferred taxes in the period in which the facts that give rise to a revision become known.

As described in further detail in the Recent Accounting Pronouncements section in Note 1 of Notes to Financial Statements in

“Item 8. Financial Statements and Supplementary Data”, FASB Interpretation (“FIN”) No. 48 “Accounting for Uncertainty in Income

Taxes—an interpretation of FASB Statement 109” is effective beginning January 1, 2007. FIN 48 establishes a single model to

address accounting for uncertainty in tax positions. FIN 48 clarifies the accounting for income taxes by prescribing a minimum

recognition threshold a tax position is required to meet before being recognized in the financial statements. FIN 48 also provides

guidance on derecognition, measurement, classification, interest and penalties, accounting in interim periods, disclosure and transition.

FIN 48 is effective for fiscal years beginning after December 15, 2006. Honeywell will adopt FIN 48 as of January 1, 2007 as

required. Based on our current assessment, and subject to any changes that may result from additional technical guidance being issued,

the adoption of FIN 48 on January 1, 2007 is expected to reduce our existing reserves for uncertain tax positions by approximately

$130 million, to be recorded as a cumulative effect adjustment to equity, largely relating to state income tax matters.

Sales Recognition on Long-Term Contracts—In 2006, we recognized approximately 12 percent of our total net sales using the

percentage-of-completion method for long-term contracts in our Automation and Control Solutions, Aerospace and Specialty

Materials reportable segments. These long-term contracts are measured on the cost-to-cost basis for engineering-type contracts and the

units-of-delivery basis for production-type contracts. Accounting for these contracts involves management judgment in estimating

total contract revenue and cost. Contract revenues are largely determined by negotiated contract prices and quantities, modified by our

assumptions regarding contract options, change orders, incentive and award provisions associated with technical performance and

price adjustment clauses (such as inflation or index-based clauses). Contract costs are incurred over a period of time, which can be

several years, and the estimation of these costs requires management judgment. Cost estimates are largely based on negotiated or

estimated purchase contract terms, historical performance trends and other economic projections. Significant factors that influence

these estimates include inflationary trends, technical and schedule risk, internal and subcontractor performance trends, business

volume assumptions, asset utilization, and anticipated labor agreements. Revenue and cost estimates are regularly monitored and

revised based on changes in circumstances. Anticipated losses on long-term contracts are recognized when such losses become

evident. We maintain financial controls over the customer qualification, contract pricing and estimation processes to reduce the risk of

contract losses.

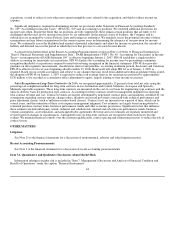

OTHER MATTERS

Litigation

See Note 21 to the financial statements for a discussion of environmental, asbestos and other litigation matters.

Recent Accounting Pronouncements

See Note 1 to the financial statements for a discussion of recent accounting pronouncements.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

Information relating to market risk is included in “Item 7. Management's Discussion and Analysis of Financial Condition and

Results of Operations” under the caption “Financial Instruments”.

44