HTC 2008 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2008 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Financial Information

| 43

42 |

2008 Annual Report

The government enacted the Alternative Minimum

Tax Act (the “AMT Act”), which became effective on

January 1, 2006. The alternative minimum tax

(“AMT”) imposed under the AMT Act is a

supplemental tax levied at a rate of 10% which is

payable if the income tax payable determined

pursuant to the Income Tax Law is below the

minimum amount prescribed under the AMT Act.

The taxable income for calculating the AMT

includes most of the income that is exempted from

income tax under various laws and statutes. The

Company has considered the impact of the AMT

Act in the determination of its tax liabilities. As a

result, the current income tax payable as of

December 31, 2008 should be NT$3,396,417

thousand (US$103,549 thousand).

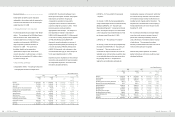

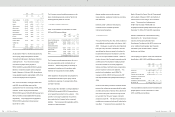

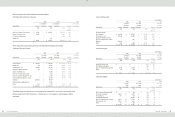

The tax effects of deductible temporary differences

and tax credit carryforwards that gave rise to

deferred tax assets as of December 31, 2006,

2007 and 2008 were as follows:

2006

2007

2008

NT$

NT$

NT$

US$

Temporary differences

(Note 3)

Provision for loss on decline in value of inventory

$

222,916

$

229,072

$

405,806

$

12,372

Unrealized marketing expenses

245,772

751,755

1,452,633

44,288

Unrealized reserve for warranty expense

348,499

867,489

1,306,466

39,831

Capitalized expense

31,936

39,628

58,190

1,774

Unrealized royalties

942,097

1,009,848

1,535,925

46,827

Unrealized bad-debt expenses

-

16,151

26,503

808

Unrealized value loss on financial instruments

19,117

24,064

128,521

3,918

Other

27,770

41,434

12,465

380

Tax credit carryforwards

-

-

2,196,808

66,976

Total deferred tax assets

1,838,107

2,979,441

7,123,317

217,174

Less: Valuation allowance

(

1,134,041

)

(

1,970,824

)

(

5,679,417

)

(

173,153

)

Total deferred tax assets, net

704,066

1,008,617

1,443,900

44,021

Deferred tax liabilities

Unrealized pension cost

(

18,505

)

(

23,797

)

(

29,284

)

(

893

)

Unrealized foreign exchange gain, net

(

38,254

)

(

42,710

)

(

40,978

)

(

1,249

)

647,307

942,110

1,373,638

41,879

Less: Current portion

(

428,077

)

(

562,025

)

(

552,494

)

(

16,844

)

Deferred tax assets - noncurrent

$

219,230

$

380,085

$

821,144

$

25,035

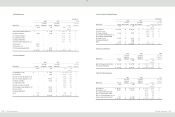

Details of the tax credit carryforwards were as follows:

Credit

2006

2007

2008

Grant Year

Validity Period

NT$

NT$

NT$

US$

(Note 3)

2007

2007-2011

$

-

$

-

$

201,506

$

6,144

2008

2008-2012

-

-

1,995,302

60,832

$

-

$

-

$

2,196,808

$

66,976

Based on the Income Tax Act of the ROC, the

investment and research and development tax

credits can be carried forward for four years.

The total credits used in each year cannot

exceed half of the estimated income tax

provision, except in the last year.

Valuation allowance is based on management’s

evaluation of the amount of tax credits that can

be carried forward for four years, based on the

Company’s financial forecasts.

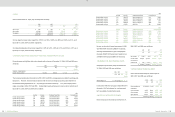

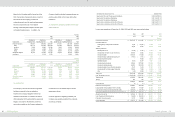

The income taxes in 2006, 2007 and 2008 were as follows:

2006

2007

2008

NT$

NT$

NT$

US$

(Note 3)

Current income tax

$1,847,294

$3,381,327

$3,396,417

$103,549

Increase in deferred income tax assets

(168,447

)

(294,803

)

(431,528

)

(13,156

)

Underestimation (overestimation) of prior year’s income tax

31,704

125,911

(9,759

)

(297

)

Income tax

$1,710,551

$3,212,435

$2,955,130

$90,096

The integrated income tax information is as follows:

2006

2007

2008

NT$

NT$

NT$

US$

(Note 3)

Balance of imputation credit account (ICA)

$1,772,897

$3,005,386

$5,568,676

$169,777

Unappropriated earnings generated from 1998

31,991,090

41,403,867

44,626,182

1,360,555

Actual/estimated creditable ratio (including income tax payable)

5.54 % (actual ratio)

7.26% (actual ratio)

12.48%(estimatedratio)

12.48%(estimatedratio)

For distribution of earnings generated on or after

January 1, 1998, the ratio for the imputation credits

allocated to stockholders of the Company is based

on the balance of the ICA as of the date of dividend

distribution. The expected creditable ratio for the

2008 earnings may be adjusted, depending on the

ICA balance on the date of dividend distribution.

23.EARNINGS PER SHARE

Earnings per share (EPS) before tax and after tax

are calculated by dividing net income by the

weighted average number of common shares

outstanding which includes the deduction of the

effect of treasury stock during each year. The

weighted average number of shares used in EPS

calculation was 761,697 thousand shares, 755,608

thousand shares and 754,148 thousand shares for

the years ended December 31, 2006, 2007 and

2008, respectively. EPS for the years ended

December 31, 2006 and 2007 were calculated

the average number of shares outstanding was

adjusted retroactively for the effect of stock

dividend distribution in 2008.

The Accounting Research and Development

Foundation issued Interpretation 2007-052 that

requires companies to recognize bonuses paid to

employees, directors and supervisors as

compensation expenses beginning January 1,

2008. These bonuses were previously recorded

as appropriations from earnings. If the Company

may settle the bonus to employees by cash or

shares, the Company should presume that the

entire amount of the bonus will be settled in shares

and the resulting potential shares should be

included in the weighted average number of

shares outstanding used in the calculation of

diluted EPS, if the shares have a dilutive effect.

The number of shares is estimated by dividing the

entire amount of the bonus by the closing price of