HTC 2008 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2008 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

|

|

Financial Information

| 91

90 |

2008 Annual Report

When the Company did not subscribe for the new

shares issued by BandRich Inc. in May 2006 and

Vitamin D Inc. in September 2008, adjustments of

NT$15,845 thousand and NT$1,689 thousand

(US$52 thousand) were made to the investment’s

carrying value and capital surplus, respectively. As

a result, the capital surplus from long-term equity

investments as of December 31, 2008 was

NT$17,534 thousand (US$535 thousand).

The additional paid-in capital from a merger (Note

1), which took effect on March 1, 2004, was

NT$25,972 thousand. Then, because of treasury

stock retirement in April 2007, the additional

paid-in capital from a merger decreased to

NT$25,756 thousand (US$785 thousand).

Appropriation of Retained Earnings and

Dividend Policy

Based on the Company Law of the ROC and the

Company’s Articles of Incorporation, 10% of the

Company’s annual net income less any deficit

should first be appropriated as legal reserve until

this reserve equals its capital. From the remainder,

there should be appropriations of not more than

3‰ as remuneration to directors and supervisors

and at least 5% as bonuses to employees.

The appropriation of retained earnings should be

proposed by the board of directors and approved

by the stockholders in their annual meeting.

As part of a high-technology industry and a

growing enterprise, the Company considers its

operating environment, industry developments,

and long-term interests of stockholders as well as

its programs to maintain operating efficiency and

meet its capital expenditure budget and financial

goals in determining the stock or cash dividends to

be paid. The Company’s dividend policy stipulates

that at least 50% of total dividends may be

distributed as cash dividends.

Had the Company recognized the employees’

bonuses of NT$531,000 thousand as expenses in

2005, the pro forma earnings per share in 2005

would have decreased from NT$33.26 to

NT$31.76, which were not adjusted retroactively

for the effect of stock dividend distribution in later

years.

Had the Company recognized the employees’

bonuses of NT$2,105,000 thousand as expenses

in 2006, the pro forma earnings per share in 2006

would have decreased from NT$57.85 to

NT$53.03, which were not adjusted retroactively

for the effect of stock dividend distribution in the

following year.

Had the Company recognized the employees’

bonuses of NT$1,313,200 thousand as expenses

in 2007, the pro forma earnings per share in 2007

would have decreased from NT$50.48 to

NT$48.19, which were not adjusted retroactively

for the effect of stock dividend distribution in the

following year.

Based on a resolution passed by the Company’s

board of directors in February 2008, the employee

bonus payable should be appropriated at 18% of

net income less employee bonus expenses. If

the actual amounts subsequently resolved by the

stockholders differ from the proposed amounts, the

differences are recorded in the year of

stockholders’ resolution as a change in accounting

estimate. If bonus shares are resolved to be

distributed to employees, the number of shares is

determined by dividing the amount of bonus by the

closing price (after considering the effect of cash

and stock dividends) of the shares of the day

preceding the stockholders’ meeting.

As of January 17, 2009, the date of the

accompanying independent auditors’ report, the

appropriation of the 2008 earnings had not been

proposed by the Board of Directors. Information

on earnings appropriation can be accessed online

through the Market Observation Post System on

the Web site.

22.TREASURY STOCK

On October 7, 2008, the Company’s board of

directors passed a resolution to buy back 10,000

thousand Company shares from the open market.

The repurchase period was between October 8,

2008 and December 7, 2008, and the repurchase

price ranged from NT$400(US$12) to NT$500

(US$15) per share. If the Company’s share price

was lower than this price range, the Company

might continue to buy back its shares.

The Company bought back 10,000 thousand

shares for NT$3,410,277 thousand (US$103,972

thousand) during the repurchase period.

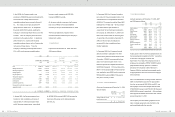

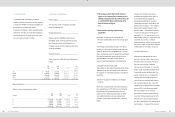

(In thousands of shares)

Purpose

As of

January 1,

2008

Increase

Decrease

As of

December 31,

2008

For maintaining the

Company’s credit

and stockholders’

equity

-

10,000

-

10,000

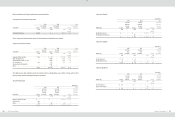

On December 12, 2006, the Company’s board of

directors passed a resolution to buy back 5,000

thousand Company shares from the open market.

The repurchase period was between December

13, 2006 and January 19, 2007, and the

repurchase price ranged from NT$601 to NT$800

per share. If the Company’s share price was

lower than this price range, the Company might

continue to buy back its shares.

During the repurchase period, the Company

bought back 3,624 thousand shares, which were

approved to be retired by the Company’s board of

directors in April 2007, for NT$1,991,755

thousand.

Based on the Securities and Exchange Act of the

ROC, the number of reacquired shares should not

exceed 10% of the Company’s issued and

outstanding stocks, and the total purchase amount

should not exceed the sum of the retained

earnings, additional paid-in capital in excess of par,

and realized capital reserve. In addition, the

Company should not pledge its treasury shares nor

exercise voting rights on the shares before their

reissuance.