HP 2012 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2012 HP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

HEWLETT-PACKARD COMPANY AND SUBSIDIARIES

Notes to Consolidated Financial Statements (Continued)

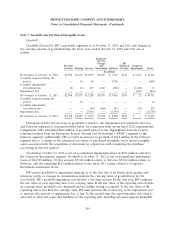

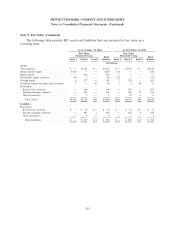

Note 9: Fair Value

HP determines fair value based on the exchange price that would be received for an asset or paid

to transfer a liability (an exit price) in the principal or most advantageous market for the asset or

liability in an orderly transaction between market participants.

Valuation techniques used by HP are based upon observable and unobservable inputs. Observable

or market inputs reflect market data obtained from independent sources, while unobservable inputs

reflect HP’s assumptions about market participant assumptions based on the best information available.

Observable inputs are the preferred basis of valuation. These two types of inputs create the following

fair value hierarchy:

Level 1—Quoted prices (unadjusted) for identical instruments in active markets.

Level 2—Quoted prices for similar instruments in active markets, quoted prices for identical or

similar instruments in markets that are not active, and model-based valuation techniques for which all

significant assumptions are observable in the market or can be corroborated by observable market data

for substantially the full term of the assets or liabilities.

Level 3—Prices or valuations that require management inputs that are both significant to the fair

value measurement and unobservable.

The following section describes the valuation methodologies HP uses to measure its financial assets

and liabilities at fair value.

Cash Equivalents and Investments: HP holds time deposits, money market funds, mutual funds,

other debt securities primarily consisting of corporate and foreign government notes and bonds, and

common stock and equivalents. Where applicable, HP uses quoted prices in active markets for identical

assets to determine fair value. If quoted prices in active markets for identical assets are not available to

determine fair value, HP uses quoted prices for similar assets and liabilities or inputs that are

observable either directly or indirectly. If quoted prices for identical or similar assets are not available,

HP uses internally developed valuation models, whose inputs include bid prices, and third-party

valuations utilizing underlying assets assumptions.

Derivative Instruments: As discussed in Note 10, HP mainly holds non-speculative forwards, swaps

and options to hedge certain foreign currency and interest rate exposures. When active market quotes

are not available, HP uses industry standard valuation models. Where applicable, these models project

future cash flows and discount the future amounts to a present value using market-based observable

inputs including interest rate curves, credit risk, foreign exchange rates, and forward and spot prices for

currencies. In certain cases, market-based observable inputs are not available and, in those cases, HP

uses management judgment to develop assumptions which are used to determine fair value.

Short- and Long-Term Debt: The estimated fair value of publicly-traded debt is based on quoted

market prices for the identical liability when traded as an asset in an active market. For other debt for

which a quoted market price is not available, an expected present value method that uses rates

currently available to HP for debt with similar terms and remaining maturities is used to estimate fair

value. The portion of HP’s fixed-rate debt obligations that is hedged is reflected in the Consolidated

Balance Sheets as an amount equal to the debt’s carrying value, including a fair value adjustment

representing changes in the fair value of the hedged debt obligations arising from movements in

benchmark interest rates. The estimated fair value of HP’s short- and long-term debt approximated its

carrying value of $28.4 billion at October 31, 2012. The estimated fair value of HP’s short- and

113