Cricket Wireless 2011 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2011 Cricket Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

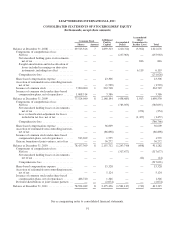

LEAP WIRELESS INTERNATIONAL, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

income and reduce its income tax liability. For state income tax purposes, the NOL carryforward period ranges

from five to 20 years. As of December 31, 2011, the Company had federal and state NOLs of approximately $2.5

billion, which begin to expire in 2022 for federal income tax purposes and of which $37.2 million will expire at

the end of 2012 for state income tax purposes. While these NOL carryforwards have a potential to be used to

offset future ordinary taxable income and reduce future cash tax liabilities by approximately $973.6 million, the

Company’s ability to utilize these NOLs will depend upon the availability of future taxable income during the

carryforward period and, as such, there is no assurance the Company will be able to realize such tax savings.

The Company’s ability to utilize NOLs could be further limited if it were to experience an “ownership

change,” as defined in Section 382 of the Internal Revenue Code and similar state provisions. In general terms,

an ownership change can occur whenever there is a collective shift in the ownership of a company by more than

50 percentage points by one or more “5% stockholders” within a three-year period. The occurrence of such a

change generally limits the amount of NOL carryforwards a company could utilize in a given year to the

aggregate fair market value of the company’s common stock immediately prior to the ownership change,

multiplied by the long-term tax-exempt interest rate in effect for the month of the ownership change.

The determination of whether an ownership change has occurred for purposes of Section 382 is complex

and requires significant judgment. The occurrence of such an ownership change would accelerate cash tax

payments the Company would be required to make and likely result in a substantial portion of its NOLs expiring

before the Company could fully utilize them. As a result, any restriction on the Company’s ability to utilize these

NOL carryforwards could have a material adverse impact on its business, financial condition and future cash

flows.

On August 30, 2011, the Company’s board of directors adopted a Tax Benefit Preservation Plan to help

deter acquisitions of Leap common stock that could result in an ownership change under Section 382 and thus

help preserve the Company’s ability to use its NOL carryforwards. The Tax Benefit Preservation Plan is designed

to deter acquisitions of Leap common stock that would result in a stockholder owning 4.99% or more of Leap

common stock (as calculated under Section 382), or any existing holder of 4.99% or more of Leap common stock

acquiring additional shares, by substantially diluting the ownership interest of any such stockholder unless the

stockholder obtains an exemption from the Company’s board of directors.

None of the Company’s NOL carryforwards are being considered as an uncertain tax position or disclosed

as an unrecognized tax benefit. Any carryforwards that expire prior to utilization as a result of a Section 382

limitation will be removed from deferred tax assets with a corresponding reduction to valuation allowance. Since

the Company currently maintains a full valuation allowance against its federal and state NOL carryforwards, it is

not expected that any possible limitation would have a current impact on its results of operations.

In accordance with the authoritative guidance for business combinations, which became effective for the

Company on January 1, 2009, any reduction in the valuation allowance, including the valuation allowance

established in fresh-start reporting, will be accounted for as a reduction of income tax expense.

The Company’s unrecognized income tax benefits and uncertain tax positions, as well as any associated

interest and penalties, are recorded through income tax expense; however, such amounts have not been

significant in any period. All of the Company’s tax years from 1998 to 2010 remain open to examination by

federal and state taxing authorities. In July 2009, the federal examination of the Company’s 2005 tax year, which

was limited in scope, was concluded and the results did not have a material impact on the consolidated financial

statements.

101