Cisco 2009 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2009 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

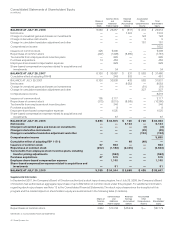

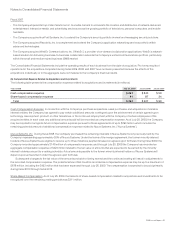

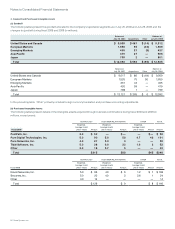

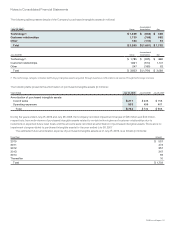

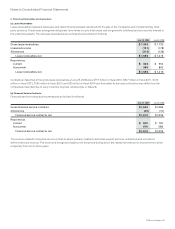

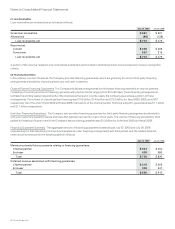

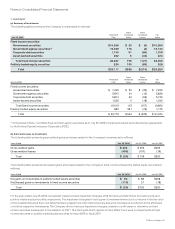

Notes to Consolidated Financial Statements

(u) Recent Accounting Pronouncements Not Yet Effective

SFAS 141(R) and SFAS 160 In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations” (“SFAS 141(R)”)

and SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements — an amendment of ARB No. 51” (“SFAS 160”). In April

2009, the FASB issued FSP FAS 141(R)-1, “Accounting for Assets Acquired and Liabilities Assumed in a Business Combination That Arise

from Contingencies” (“FSP 141(R)-1”).

SFAS 141(R) will significantly change previous accounting practices regarding business combinations. Among the more significant

changes, SFAS 141(R) expands the definition of a business and a business combination; requires the acquirer to recognize the assets

acquired, liabilities assumed and noncontrolling interests (including goodwill) measured at fair value at the acquisition date; requires

acquisition-related expenses and restructuring costs to be recognized separately from the business combination; requires assets

acquired and liabilities assumed to be recognized at their acquisition-date fair values with subsequent changes recognized in earnings;

and requires in-process research and development to be capitalized at fair value as an indefinite-lived intangible asset. FSP 141(R)-1

amends and clarifies SFAS 141(R) to address application issues on initial recognition and measurement, subsequent measurement and

accounting, and disclosure of assets and liabilities arising from contingencies in a business combination. SFAS 160 will change the

accounting and reporting for minority interests, reporting them as equity separate from the parent entity’s equity, as well as requiring

expanded disclosures.

Each of SFAS 141(R), FSP 141(R)-1 and SFAS 160 is effective for financial statements issued for fiscal years beginning after

December 15, 2008, and therefore will be effective for the Company beginning in the first quarter of fiscal 2010. SFAS 141(R) and its related

FSP are effective for acquisitions closing in fiscal 2010, with impacts that may vary depending on each specific business combination or

asset purchase. Upon adoption of SFAS 160, the Company will disclose its noncontrolling interests in accordance with the guidance, and it

does not expect that there will be a material impact on its results of operations or financial position.

FSP FAS 157-2 In February 2008, the FASB issued FSP FAS 157-2, “Effective Date of FASB Statement No. 157” (“FSP 157-2”), which

delayed the effective date of SFAS 157 for all nonfinancial assets and nonfinancial liabilities, except for items that are recognized or

disclosed at fair value in the financial statements on a recurring basis (at least annually), until the beginning of the Company’s fiscal 2010.

The Company does not expect that the application of SFAS 157, when applied to nonfinancial assets and liabilities, will have a material

impact on its results of operations or financial position.

SFAS 166 In June 2009, the FASB issued SFAS No. 166, “Accounting for Transfers of Financial Assets — an amendment of FASB

Statement No. 140” (“SFAS 166”). SFAS 166 eliminates the concept of a qualifying special-purpose entity; removes the scope exception

from applying FASB Interpretation No. 46(R), “Consolidation of Variable Interest Entities” to qualifying special-purpose entities; changes the

requirements for derecognizing financial assets; and requires enhanced disclosure. SFAS 166 is effective for the Company beginning in

the first quarter of fiscal 2011. The Company is currently evaluating the impact that the adoption of SFAS 166 will have on its consolidated

financial statements.

SFAS 167 In June 2009, the FASB issued SFAS No. 167, “Amendments to FASB Interpretation No. 46(R)” (“SFAS 167”). SFAS 167 replaces

the quantitative-based risks and rewards approach with a qualitative approach that focuses on identifying which enterprise has the power

to direct the activities of a variable interest entity that most significantly impact the entity’s economic performance. It also requires an

ongoing reassessment of whether an entity is the primary beneficiary and requires additional disclosures about an enterprise’s

involvement in variable interest entities. SFAS 167 is effective for the Company beginning in the first quarter of fiscal 2011. The Company is

currently evaluating the impact that the adoption of SFAS 167 will have on its consolidated financial statements.

(v) Reclassifications Certain reclassifications have been made to amounts for prior years in order to conform to the current year’s

presentation.

2009 Annual Report 47