Cisco 2009 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2009 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

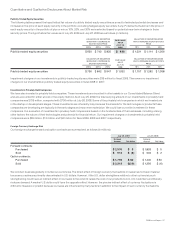

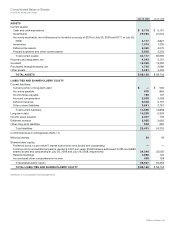

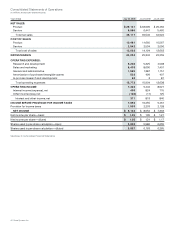

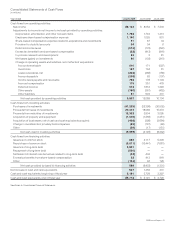

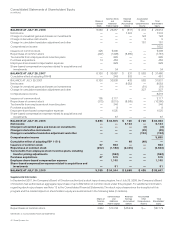

Notes to Consolidated Financial Statements

1. Basis of Presentation

The fiscal year for Cisco Systems, Inc. (the “Company” or “Cisco”) is the 52 or 53 weeks ending on the last Saturday in July. Fiscal 2009,

2008, and 2007 were 52-week fiscal years. The Consolidated Financial Statements include the accounts of Cisco and its subsidiaries. All

significant intercompany accounts and transactions have been eliminated. The Company conducts business globally and is primarily

managed on a geographic basis in the following theaters: United States and Canada, European Markets, Emerging Markets, Asia Pacific,

and Japan. The Emerging Markets theater consists of Eastern Europe, Latin America, the Middle East and Africa, and Russia and the

Commonwealth of Independent States.

The Company has evaluated subsequent events, as defined by SFAS No. 165, “Subsequent Events,” through the date that the financial

statements were issued on September 10, 2009.

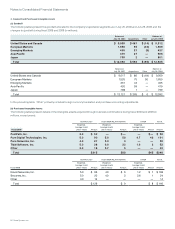

2. Summary of Significant Accounting Policies

(a) Cash and Cash Equivalents The Company considers all highly liquid investments purchased with an original or remaining maturity of

less than three months at the date of purchase to be cash equivalents. Cash and cash equivalents are maintained with various financial

institutions.

(b) Investments The Company’s investments include government and government agency securities, corporate debt securities, asset-

backed securities, and publicly traded equity securities. These investments are held in the custody of several major financial institutions.

The specific identification method is used to determine the cost basis of fixed income securities sold. The weighted-average method is

used to determine the cost basis of publicly traded equity securities sold. The Company classifies its investments as available-for-sale and

these investments are recorded in the Consolidated Balance Sheets at fair value. Unrealized gains and losses on these investments, to the

extent the investments are unhedged, are included as a separate component of accumulated other comprehensive income (AOCI), net of

tax. The Company classifies its investments as current or noncurrent based on the nature of the investments and their availability for use in

current operations.

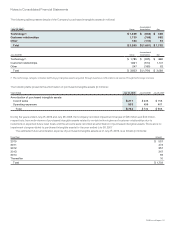

Other-Than-Temporary Impairments Effective April 26, 2009, the Company adopted FSP 115-2, which amends other-than-temporary

impairment guidance relating to debt securities. If the fair value of a debt security is less than its amortized cost, the Company assesses

whether the impairment is other than temporary. An impairment is considered other than temporary if (i) the Company has the intent to sell

the security, (ii) it is more likely than not that the Company will be required to sell the security before recovery of the entire amortized cost

basis, or (iii) the Company does not expect to recover the entire amortized cost basis of the security. If an impairment is considered other

than temporary based on condition (i) or (ii) described above, the entire difference between the amortized cost and the fair value of the

debt security is recognized in earnings. If an impairment is considered other than temporary based on condition (iii), the amount

representing credit losses (defined as the difference between the present value of the cash flows expected to be collected and the

amortized cost basis of the debt security) will be recognized in earnings and the amount relating to all other factors will be recognized in

OCI. Upon the adoption of FSP 115-2, the Company recorded a cumulative effect adjustment of $49 million, which resulted in an increase

to the balance of retained earnings with a corresponding decrease to OCI. Prior to the adoption of FSP 115-2, the Company recognized

impairment charges on fixed income securities using the impairment policy as is currently applied to publicly traded equity securities, as

discussed below.

The Company recognizes an impairment charge on publicly traded equity securities when a decline in the fair value of its investments

in publicly traded equity securities below the cost basis is judged to be other than temporary. The Company considers various factors in

determining whether a decline in the fair value of these investments is other than temporary, including the length of time and extent to

which the fair value of the security has been less than the Company’s cost basis, the financial condition and near-term prospects of the

issuer, and the Company’s intent and ability to hold the investment for a period of time sufficient to allow for any anticipated recovery in

market value.

Investments in privately held companies are included in other assets in the Consolidated Balance Sheets and are primarily accounted

for using either the cost or equity method. The Company monitors these investments for impairments and makes appropriate reductions in

carrying values if the Company determines that an impairment charge is required based primarily on the financial condition and near-term

prospects of these companies.

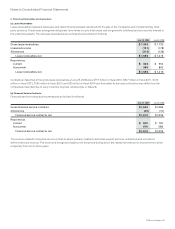

(c) Inventories Inventories are stated at the lower of cost or market. Cost is computed using standard cost, which approximates actual cost,

on a first-in, first-out basis. The Company provides inventory write-downs based on excess and obsolete inventories determined primarily

by future demand forecasts. The write-down is measured as the difference between the cost of the inventory and market based upon

assumptions about future demand and charged to the provision for inventory, which is a component of cost of sales. At the point of the loss

recognition, a new, lower-cost basis for that inventory is established, and subsequent changes in facts and circumstances do not result in

the restoration or increase in that newly established cost basis. In addition, the Company records a liability for firm, noncancelable, and

unconditional purchase commitments with contract manufacturers and suppliers for quantities in excess of the Company’s future demand

forecasts consistent with its valuation of excess and obsolete inventory.

2009 Annual Report 43