Cisco 2009 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2009 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

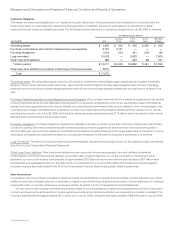

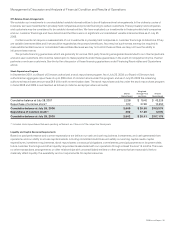

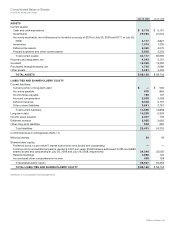

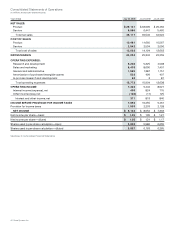

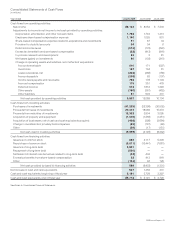

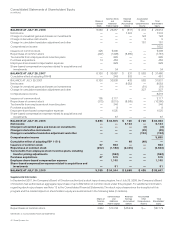

Quantitative and Qualitative Disclosures About Market Risk

Our financial position is exposed to a variety of risks including interest rate risk, equity price risk, and foreign currency exchange risk.

Interest Rate Risk

Fixed Income Investments

We maintain an investment portfolio of various holdings, types, and maturities. Our primary objective for holding fixed income securities is

to achieve an appropriate investment return consistent with preserving principal and managing risk. At any time, a sharp rise in interest

rates or credit spreads could have a material adverse impact on the fair value of our fixed income investment portfolio. Conversely,

declines in interest rates, including the impact from lower credit spreads, could have a material adverse impact on interest income for our

investment portfolio. We may utilize derivative instruments designated as hedging instruments to achieve our investment objectives. We

had no outstanding hedging instruments for our fixed income securities as of July 25, 2009. Our fixed income instruments are held for

purposes other than trading. Our fixed income instruments are not leveraged as of July 25, 2009. See Note 7 to the Consolidated Financial

Statements. We monitor our interest rate and credit risks, including our credit exposures to specific rating categories and to individual

issuers. We believe the overall credit quality of our portfolio is strong, with our cash equivalents and fixed income portfolio invested in

securities with a weighted-average credit rating exceeding AA.

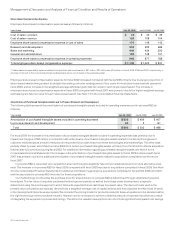

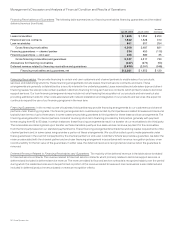

The following tables present the hypothetical fair values of our fixed income securities, including the hedging effects when applicable,

as a result of selected potential market decreases and increases in interest rates. For the balances as of July 25, 2009, the market changes

reflect immediate hypothetical parallel shifts in the yield curve of plus or minus 50 basis points (“BPS”), plus 100 BPS, and plus 150 BPS.

Due to the low interest rate environment at the end of fiscal 2009, we did not believe a parallel of shift of minus 100 BPS or minus 150 BPS

was relevant for the July 25, 2009 balances. For the balances as of July 26, 2008, the market changes reflect immediate hypothetical

parallel shifts in the yield curve of plus or minus 50 BPS, 100 BPS, and 150 BPS. The hypothetical fair values as of July 25, 2009 and July 26,

2008 are as follows (in millions):

VALUATION OF SECURITIES

GIVEN AN INTEREST RATE

DECREASE OF X BASIS POINTS

FAIR VALUE

AS OF

JULY 25,

2009

VALUATION OF SECURITIES

GIVEN AN INTEREST RATE

INCREASE OF X BASIS POINTS

(150 BPS) (100 BPS) (50 BPS) 50 BPS 100 BPS 150 BPS

Fixed income securities N/A N/A $ 28,486 $ 28,355 $ 28,224 $ 28,093 $ 27,963

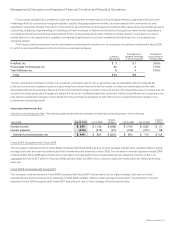

VALUATION OF SECURITIES

GIVEN AN INTEREST RATE

DECREASE OF X BASIS POINTS

FAIR VALUE

AS OF

JULY 26,

2008

VALUATION OF SECURITIES

GIVEN AN INTEREST RATE

INCREASE OF X BASIS POINTS

(150 BPS) (100 BPS) (50 BPS) 50 BPS 100 BPS 150 BPS

Fixed income securities $ 20,216 $ 20,100 $ 19,985 $ 19,869 $ 19,753 $ 19,638 $ 19,522

Impairment charges on our investments in fixed income securities were $219 million for fiscal 2009. There were no impairment charges on

our investments in fixed income securities in fiscal 2008 or 2007.

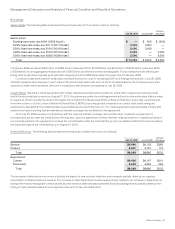

Long-Term Debt

As of July 25, 2009, we had $10.0 billion in principal amount of fixed-rate long-term debt outstanding, with a carrying amount of $10.3 billion

and a fair value of $10.5 billion, which fair value is based on market prices. A hypothetical 50 BPS increase or decrease in market interest

rates would decrease or increase, respectively, the fair value of the fixed-rate debt as of July 25, 2009 by approximately $300 million.

However, this hypothetical change in interest rates would not impact the interest expense on the fixed-rate debt.

Equity Price Risk

The fair value of our equity investments in publicly traded companies is subject to market price volatility. We may hold equity securities for

strategic purposes or to diversify our overall investment portfolio. Our equity portfolio consists of securities with characteristics that most

closely match the Standard & Poor’s 500 Index or NASDAQ Composite Index. These equity securities are held for purposes other than

trading. To manage our exposure to changes in the fair value of certain equity securities, we may enter into equity derivatives designated

as hedging instruments.

36 Cisco Systems, Inc.