Berkshire Hathaway 2006 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2006 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82

|

|

72

Management’s Discussion (Continued)

Equity Price Risk (Continued)

Berkshire is also subject to equity price risk with respect to certain long duration equity index option contracts.

Berkshire’s maximum exposure with respect to such contracts was approximately $21 billion and $14 billion at

December 31, 2006 and 2005, respectively. These contracts generally expire 15 to 20 years from inception and they may not be

settled before their respective expiration dates. The contracts have been written on four major equity indexes including three that

are foreign. While Berkshire’s ultimate potential loss with respect to these contracts is directly correlated to the movement of the

underlying stock index between contract inception date and expiration, the change in fair value from current changes in the

indices do not produce a proportional change in the estimated fair value of the contracts. Other factors (such as expected future

interest rates, dividend rates and the remaining duration of the contract as well as the general market assumptions) affect the

estimates of fair value reflected in the financial statements. Thus, if the underlying indices declined 30% immediately, and

absent changes in other factors, Berkshire estimates that it could incur a non-cash pre-tax loss of approximately $2 billion from

the change in the estimated fair value of open contracts as of December 31, 2006.

Foreign Currency Risk

Market risks associated with changes in foreign currency exchange rates are currently concentrated in a portfolio of

long duration equity index option contracts on foreign equity indexes. In 2005, Berkshire also had significant exposure to

foreign currency risk from a portfolio of short duration forward contracts. The aggregate notional value of forward contracts was

approximately $1 billion as of December 31, 2006 compared to approximately $13.8 billion as of December 31, 2005.

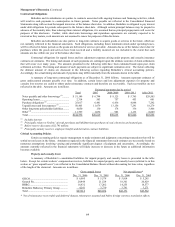

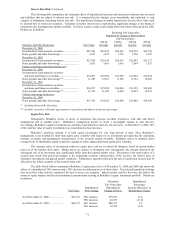

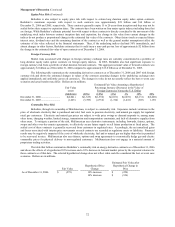

The following table summarizes the outstanding derivatives contracts as of December 31, 2006 and 2005 with foreign

currency risk and shows the estimated changes in values of the contracts assuming changes in the underlying exchange rates

applied immediately and uniformly across all currencies. The changes in value do not necessarily reflect the best or worst case

scenarios and actual results may differ. Dollars are in millions.

Estimated Fair Value Assuming a Hypothetical

Fair Value Percentage Increase (Decrease) in the Value of

assets

Foreign Currencies Versus the U.S. Dollar

(liabilities) (20%) (10%) (1%) 1% 10% 20%

December 31, 2006............................. $(2,041) $(1,819) $(1,936) $(2,031) $(2,051) $(2,131) $(2,200)

December 31, 2005............................. (1,603) (3,789) (2,752) (1,724) (1,481) (305) 1,198

Commodity Price Risk

Berkshire, through its ownership of MidAmerican, is subject to commodity risk. Exposures include variations in the

price of wholesale electricity that is purchased and sold, fuel costs to generate electricity, and natural gas supply for regulated

retail gas customers. Electricity and natural gas prices are subject to wide price swings as demand responds to, among many

other items, changing weather, limited storage, transmission and transportation constraints, and lack of alternative supplies from

other areas. To mitigate a portion of the risk, MidAmerican uses derivative instruments, including forwards, futures, options,

swaps and other over-the-counter agreements, to effectively secure future supply or sell future production at fixed prices. The

settled cost of these contracts is generally recovered from customers in regulated rates. Accordingly, the net unrealized gains

and losses associated with interim price movements on such contracts are recorded as regulatory assets or liabilities. Financial

results may be negatively impacted if the costs of wholesale electricity, fuel and or natural gas are higher than what is permitted

to be recovered in rates. MidAmerican also uses futures, options and swap agreements to economically hedge gas and electric

commodity prices for physical delivery to non-regulated customers. MidAmerican does not engage in a material amount of

proprietary trading activities.

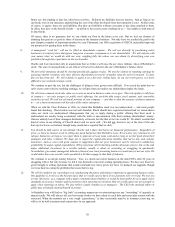

The table that follows summarizes Berkshire’s commodity risk on energy derivative contracts as of December 31, 2006

and shows the effects of a hypothetical 10% increase and a 10% decrease in forward market prices by the expected volumes for

these contracts as of that date. The selected hypothetical change does not reflect what could be considered the best or worst case

scenarios. Dollars are in millions.

Fair Value

Hypothetical Price

Change

Estimated Fair Value after

Hypothetical Change in

Price

As of December 31, 2006 $ (273) 10% increase $ (220)

10% decrease $ (326)