Berkshire Hathaway 2006 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2006 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

34

Notes to Consolidated Financial Statements (Continued)

(1) Significant accounting policies and practices (Continued)

(k) Losses and loss adjustment expenses (Continued)

The estimated liabilities of workers’ compensation claims assumed under certain reinsurance contracts are carried in the

Consolidated Balance Sheets at discounted amounts. Discounted amounts are based upon an annual discount rate of

4.5% for claims arising prior to 2003 and 1% for claims arising after 2002, consistent with discount rates used under

statutory accounting principles. The periodic discount accretion is included in the Consolidated Statements of

Earnings as a component of losses and loss adjustment expenses.

(l) Deferred charges reinsurance assumed

The excess of estimated liabilities for claims and claim costs over the consideration received with respect to retroactive

property and casualty reinsurance contracts that provide for indemnification of insurance risk is established as a

deferred charge at inception of such contracts. The deferred charges are subsequently amortized using the interest

method over the expected claim settlement periods. The periodic amortization charges are reflected in the

accompanying Consolidated Statements of Earnings as losses and loss adjustment expenses.

Changes to the expected timing and estimated amount of loss payments produce changes in the unamortized deferred

charge balance. Such changes in estimates are determined retrospectively and included in insurance losses and loss

adjustment expense in the period of the change.

(m) Insurance premium acquisition costs

Costs that vary and are related to the issuance of insurance policies are deferred, subject to ultimate recoverability, and

charged to underwriting expenses as the related premiums are earned. Acquisition costs consist of commissions,

premium taxes, advertising and other underwriting costs. The recoverability of premium acquisition costs,

generally, reflects anticipation of investment income. The unamortized balances of deferred premium acquisition

costs are included in other assets and were $1,432 million and $1,287 million at December 31, 2006 and 2005,

respectively.

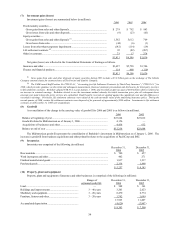

(n) Regulated utilities and energy businesses

Certain domestic energy subsidiaries prepare their financial statements in accordance with SFAS No. 71, reflecting

economic effects deriving from the ability to recover certain costs from customers and the requirement to return

revenues to customers in the future through the regulated rate-setting process. Accordingly, certain costs are

deferred as regulatory assets and obligations are accrued as regulatory liabilities, which will be amortized over

various future periods. At December 31, 2006, MidAmerican had $1,827 million in regulatory assets and $1,839

million in regulatory liabilities, which are components of other assets and other liabilities of utilities and energy

businesses.

Management continually assesses whether the regulatory assets are probable of future recovery by considering factors

such as applicable regulatory changes, recent rate orders received by other regulated entities and the status of any

pending or potential deregulation legislation. If future recovery of costs ceases to be probable, the amount no longer

probable of recovery is charged to earnings.

Utilities and energy businesses recognize legal asset retirement obligations (“ARO”), mainly related to the

decommissioning of nuclear generation assets and the final reclamation of leased coal mining property. The

estimated fair value of a legal ARO is recognized as a liability when a reasonable estimate of the expected future

cash flows can be made. This liability is added to the carrying amount of the associated asset, which is then

depreciated over the remaining useful life of the asset. Subsequent to the initial recognition, the liability is

periodically adjusted for revisions to assumptions used in determining the present value of the retirement obligation.

The ARO as of December 31, 2006 was approximately $423 million and is reflected in other liabilities of utilities

and energy businesses.

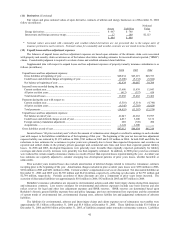

(p) Foreign currency

The accounts of foreign-based subsidiaries are measured in most instances using the local currency as the functional

currency. Revenues and expenses of these businesses are translated into U.S. dollars at the average exchange rate

for the period. Assets and liabilities are translated at the exchange rate as of the end of the reporting period. Gains

or losses from translating the financial statements of foreign-based operations are included in shareholders’ equity

as a component of accumulated other comprehensive income. Unrealized gains or losses associated with available-

for-sale securities are included as a component of other comprehensive income. Gains and losses arising from other

transactions denominated in a foreign currency are included in the Consolidated Statements of Earnings.

(q) Deferred income taxes

Deferred income taxes are calculated under the liability method. Deferred tax assets and liabilities are based on

differences between the financial statement and tax basis of assets and liabilities at the enacted tax rates. Changes in

deferred income tax assets and liabilities that are associated with components of other comprehensive income

(primarily unrealized investment gains and losses) are charged or credited directly to other comprehensive income.

Otherwise, changes in deferred income tax assets and liabilities are included as a component of income tax expense.

Valuation allowances have been established for certain deferred tax assets where realization is not likely.