Berkshire Hathaway 2006 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2006 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

of your ancestors. I believe that at some point in the future U.S. workers and voters will find this annual

“tribute” so onerous that there will be a severe political backlash. How that will play out in markets is

impossible to predict – but to expect a “soft landing” seems like wishful thinking.

* * * * * * * * * * * *

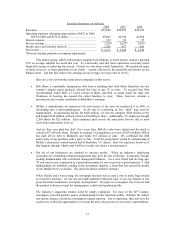

I should mention that all of the direct currency profits we have realized have come from forward

contracts, which are derivatives, and that we have entered into other types of derivatives contracts as well.

That may seem odd, since you know of our expensive experience in unwinding the derivatives book at Gen

Re and also have heard me talk of the systemic problems that could result from the enormous growth in the

use of derivatives. Why, you may wonder, are we fooling around with such potentially toxic material?

The answer is that derivatives, just like stocks and bonds, are sometimes wildly mispriced. For

many years, accordingly, we have selectively written derivative contracts – few in number but sometimes

for large dollar amounts. We currently have 62 contracts outstanding. I manage them personally, and they

are free of counterparty credit risk. So far, these derivative contracts have worked out well for us,

producing pre-tax profits in the hundreds of millions of dollars (above and beyond the gains I’ ve itemized

from forward foreign-exchange contracts). Though we will experience losses from time to time, we are

likely to continue to earn – overall – significant profits from mispriced derivatives.

* * * * * * * * * * * *

I have told you that Berkshire has three outstanding candidates to replace me as CEO and that the

Board knows exactly who should take over if I should die tonight. Each of the three is much younger than

I. The directors believe it’ s important that my successor have the prospect of a long tenure.

Frankly, we are not as well-prepared on the investment side of our business. There’ s a history

here: At one time, Charlie was my potential replacement for investing, and more recently Lou Simpson has

filled that slot. Lou is a top-notch investor with an outstanding long-term record of managing GEICO’ s

equity portfolio. But he is only six years younger than I. If I were to die soon, he would fill in

magnificently for a short period. For the long-term, though, we need a different answer.

At our October board meeting, we discussed that subject fully. And we emerged with a plan,

which I will carry out with the help of Charlie and Lou.

Under this plan, I intend to hire a younger man or woman with the potential to manage a very

large portfolio, who we hope will succeed me as Berkshire’ s chief investment officer when the need for

someone to do that arises. As part of the selection process, we may in fact take on several candidates.

Picking the right person(s) will not be an easy task. It’ s not hard, of course, to find smart people,

among them individuals who have impressive investment records. But there is far more to successful long-

term investing than brains and performance that has recently been good.

Over time, markets will do extraordinary, even bizarre, things. A single, big mistake could wipe

out a long string of successes. We therefore need someone genetically programmed to recognize and avoid

serious risks, including those never before encountered. Certain perils that lurk in investment strategies

cannot be spotted by use of the models commonly employed today by financial institutions.

Temperament is also important. Independent thinking, emotional stability, and a keen

understanding of both human and institutional behavior is vital to long-term investment success. I’ ve seen

a lot of very smart people who have lacked these virtues.

Finally, we have a special problem to consider: our ability to keep the person we hire. Being able

to list Berkshire on a resume would materially enhance the marketability of an investment manager. We

will need, therefore, to be sure we can retain our choice, even though he or she could leave and make much

more money elsewhere.

17