Berkshire Hathaway 2006 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2006 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

44

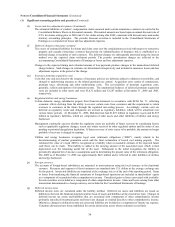

Notes to Consolidated Financial Statements (Continued)

(14) Income taxes (Continued)

Berkshire and its subsidiaries’ income tax returns are continuously under audit by Federal and various local and international

taxing authorities. Berkshire’ s consolidated Federal income tax return liabilities have been settled with the Internal Revenue Service

through 1998. Berkshire has received approximately $50 million in income tax refunds and interest with respect to certain issues in

its Federal income tax returns dating back to 1988 that were litigated and for which a favorable ruling from the U.S. District Court

was received in the fourth quarter of 2005. Berkshire does not currently believe that the impact of potential future audit adjustments

will have a material effect on its Consolidated Financial Statements.

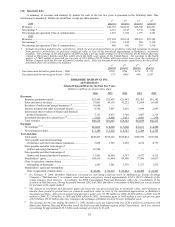

Charges for income taxes are reconciled to hypothetical amounts computed at the U.S. Federal statutory rate in the table shown

below (in millions).

2006 2005 2004

Earnings before income taxes................................................................................................ $16,778 $12,791 $10,936

Hypothetical amounts applicable to above

computed at the Federal statutory rate ............................................................................... $ 5,872 $ 4,477 $ 3,828

Tax effects resulting from:

Tax-exempt interest income............................................................................................... (44) (65) (59)

Dividends received deduction ............................................................................................ (224) (133) (116)

Net earnings of MidAmerican............................................................................................ — (183) (83)

State income taxes, less Federal income tax benefit.............................................................. 99 84 70

Foreign rate differences......................................................................................................... (45) 56 (41)

Other differences, net ............................................................................................................ (153) (77) (30)

Total income taxes ................................................................................................................ $ 5,505 $ 4,159 $ 3,569

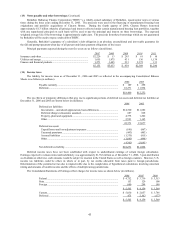

(15) Dividend restrictions – Insurance subsidiaries

Payments of dividends by insurance subsidiaries are restricted by insurance statutes and regulations. Without prior regulatory

approval, insurance subsidiaries may declare up to approximately $6.4 billion as ordinary dividends before the end of 2007.

Combined shareholders’ equity of U.S. based property/casualty insurance subsidiaries determined pursuant to statutory

accounting rules (Statutory Surplus as Regards Policyholders) was approximately $59 billion at December 31, 2006 and $52 billion at

December 31, 2005.

Statutory surplus differs from the corresponding amount determined on the basis of GAAP. The major differences between

statutory basis accounting and GAAP are that deferred charges reinsurance assumed, deferred policy acquisition costs, unrealized

gains and losses on investments in fixed maturity securities and related deferred income taxes are recognized under GAAP but not for

statutory reporting purposes. In addition, statutory accounting for goodwill of acquired businesses requires amortization of goodwill

over 10 years, whereas under GAAP, goodwill is subject to periodic tests for impairment.

(16) Fair values of financial instruments

The estimated fair values of Berkshire’ s financial instruments as of December 31, 2006 and 2005 are as follows (in millions).

Carrying Value Fair Value

2006 2005 2006 2005

Insurance and other:

Investments in fixed maturity securities....................................................... $25,300 $27,420 $25,300 $27,420

Investments in equity securities ................................................................... 61,533 46,721 61,533 46,721

Notes payable and other borrowings............................................................ 3,698 3,583 3,815 3,653

Finance and financial products:

Investments in fixed maturity securities....................................................... 3,012 3,435 3,164 3,615

Derivative contract assets

(a) ....................................................................... 624 801 624 801

Loans and finance receivables ..................................................................... 11,498 11,087 11,862 11,370

Notes payable and other borrowings............................................................ 11,961 10,868 11,787 10,865

Derivative contract liabilities....................................................................... 3,883 5,061 3,883 5,061

Utilities and energy:

Investments

(a)............................................................................................. 1,046 — 1,041 —

Derivative contract assets

(a) ....................................................................... 484 — 484 —

Notes payable and other borrowings............................................................ 16,946 — 17,789 —

Derivative contract liabilities

(b).................................................................. 889 — 889 —

(a) Included in Other assets

(b) Included in Accounts payable, accruals and other liabilities

In determining fair value of financial instruments, Berkshire used quoted market prices when available. For instruments where

quoted market prices were not available, independent pricing services or appraisals by Berkshire’ s management were used. Those