AutoZone 2013 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2013 AutoZone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

21

we have not experienced any fundamental shifts in our category sales mix as compared to previous years, we did

experience a slight decline in sales of the maintenance category as a percentage of sales. We believe the slowdown

in maintenance related products during fiscal 2013 was largely due to weather related impacts in various regions.

Because of the unusually mild winter during fiscal 2012 across parts of the U.S., we saw a reduced benefit from

sales of maintenance related products in fiscal 2013 compared to the prior fiscal year. However, sales in the

maintenance category did improve in the last quarter of fiscal 2013 due to a more normalized winter in fiscal 2013

as compared to fiscal 2012.

Our primary response to fluctuations in the demand for the products we sell is to adjust our advertising message,

store staffing, and product assortment. Specifically, during fiscal 2013, we have closely studied our hub

distribution model and store inventory levels and assortment. As a result, we are performing certain strategic tests

including adding additional inventory into our hub stores and increasing product availability in our stores. We

continue to believe we are well positioned to help our customers save money and meet their needs in a

challenging macroeconomic environment.

The two statistics we believe have the closest correlation to our market growth over the long-term are miles driven

and the number of seven year old or older vehicles on the road.

Miles Driven

We believe that as the number of miles driven increases, consumers’ vehicles are more likely to need service and

maintenance, resulting in an increase in the need for automotive hard parts and maintenance items. While over the

long-term, we have seen a close correlation between our net sales and the number of miles driven, we have also

seen certain time frames of minimal correlation in sales performance and miles driven. During the periods of

minimal correlation between net sales and miles driven, we believe net sales have been positively impacted by

other factors, including the number of seven year old or older vehicles on the road. Since the beginning of the

fiscal year and through June 2013 (latest publicly available information), miles driven decreased slightly

compared to the same period last year.

Seven Year Old or Older Vehicles

Since 2008, new vehicle sales have been significantly lower than historical levels, which we believe contributed to

an increasing number of seven year old or older vehicles on the road. We estimate vehicles are driven an average

of approximately 12,500 miles each year. In seven years, the average miles driven equates to approximately

87,500 miles. Our experience is that at this point in a vehicle’s life, most vehicles are not covered by warranties

and increased maintenance is needed to keep the vehicle operating. According to the latest data provided by the

Automotive Aftermarket Industry Association, as of January 1, 2013, the average age of vehicles on the road is

11.3 years as compared to 11.1 years as of January 1, 2012. Although the average age of vehicles continues to

increase, it is increasing at a decelerated rate primarily driven by the improvement in new car sales in recent years.

However, in the near term, we expect the aging vehicle population to continue to increase, as consumers keep

their cars longer in an effort to save money during this uncertain economy. As the number of seven year old or

older vehicles on the road increases, we expect an increase in demand for the products we sell.

Results of Operations

Fiscal 2013 Compared with Fiscal 2012

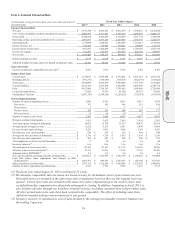

For the fiscal year ended August 31, 2013, we reported net sales of $9.148 billion compared with $8.604 billion

for the year ended August 25, 2012, a 6.3% increase from fiscal 2012. This growth was driven primarily by sales

from new stores of $222.3 million, the 53rd week sales of $177.7 million, and sales from AutoAnything for a

portion of the fiscal year.

At August 31, 2013, we operated 4,836 domestic stores, 362 stores in Mexico and three stores in Brazil, compared

with 4,685 domestic stores, 321 stores in Mexico and none in Brazil at August 25, 2012. We reported a total auto

parts (domestic, Mexico and Brazil) sales increase of 5.2% for fiscal 2013.

Gross profit for fiscal 2013 was $4.741 billion, or 51.8% of net sales, compared with $4.432 billion, or 51.5% of

net sales for fiscal 2012. The improvement in gross margin was primarily driven by lower product acquisition

costs, partially offset by the inclusion of AutoAnything (28 basis points).

10-K