AutoZone 2013 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2013 AutoZone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

59

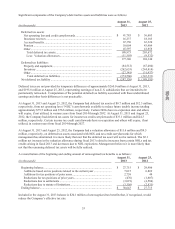

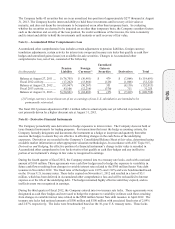

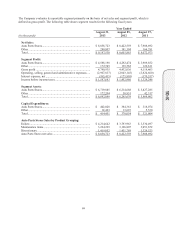

The revolving credit facility agreement requires that the Company’s consolidated interest coverage ratio as of the

last day of each quarter shall be no less than 2.50:1. This ratio is defined as the ratio of (i) consolidated earnings

before interest, taxes and rents to (ii) consolidated interest expense plus consolidated rents. The Company’s

consolidated interest coverage ratio as of August 31, 2013 was 4.68:1.

In addition to the revolving credit facility, the Company also maintains a letter of credit facility that allows it to

request the participating bank to issue letters of credit on its behalf up to an aggregate amount of $100 million. As

of August 31, 2013, the Company has $99.4 million in letters of credit outstanding under the letter of credit

facility, which expires in June 2016.

In addition to the outstanding letters of credit issued under the committed facilities discussed above, the Company

had $41.8 million in letters of credit outstanding as of August 31, 2013. These letters of credit have various

maturity dates and were issued on an uncommitted basis.

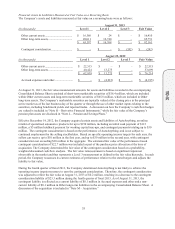

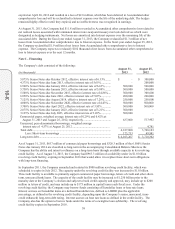

On April 29, 2013, the Company issued $500 million in 3.125% Senior Notes due July 2023 under its shelf

registration statement filed with the SEC on April 17, 2012 (the “Shelf Registration”). The Shelf Registration

allows the Company to sell an indeterminate amount in debt securities to fund general corporate purposes,

including repaying, redeeming or repurchasing outstanding debt and for working capital, capital expenditures,

new store openings, stock repurchases and acquisitions. Proceeds from the debt issuance on April 29, 2013, were

used to repay a portion of the outstanding commercial paper borrowings and for general corporate purposes. The

Company used commercial paper borrowings to repay the $200 million in 4.375% Senior Notes due June 2013.

On November 13, 2012, the Company issued $300 million in 2.875% Senior Notes due January 2023 under its

Shelf Registration. Proceeds from the debt issuance on November 13, 2012, were used to repay a portion of the

outstanding commercial paper borrowings, which were used to repay the $300 million in 5.875% Senior Notes

due in October 2012, and for general corporate purposes.

On April 24, 2012, the Company issued $500 million in 3.700% Senior Notes due April 2022 under its Shelf

Registration. The Company used the proceeds from the issuance of debt to repay a portion of the commercial

paper borrowings and for general corporate purposes.

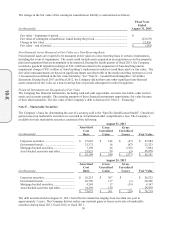

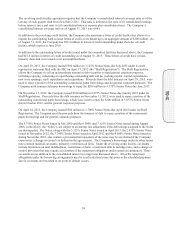

The 5.750% Senior Notes issued in July 2009 and the 6.500% and 7.125% Senior Notes issued during August

2008, (collectively, the “Notes”), are subject to an interest rate adjustment if the debt ratings assigned to the Notes

are downgraded. The Notes, along with the 3.125% Senior Notes issued in April 2013, the 2.875% Senior Notes

issued in November 2012, the 3.700% Senior Notes issued in April 2012 and the 4.000% Senior Notes issued in

during November 2010, also contain a provision that repayment of the notes may be accelerated if the Company

experiences a change in control (as defined in the agreements). The Company’s borrowings under its other senior

notes contain minimal covenants, primarily restrictions on liens. Under the revolving credit facility, covenants

include limitations on total indebtedness, restrictions on liens, a maximum debt to earnings ratio, and a change of

control provision that may require acceleration of the repayment obligations under certain circumstances. These

covenants are in addition to the consolidated interest coverage ratio discussed above. All of the repayment

obligations under the borrowing arrangements may be accelerated and come due prior to the scheduled payment

date if covenants are breached or an event of default occurs.

10-K