Audi 2015 Annual Report Download - page 232

Download and view the complete annual report

Please find page 232 of the 2015 Audi annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

RECOGNITION AND MEASUREMENT PRINCIPLES

232 >>

RECOGNITION AND

MEASUREMENT PRINCIPLES

/RECOGNITION OF INCOME AND EXPENSES

Revenue, interest income and other operating income are

always recorded when the services are rendered or the goods

or products are delivered, i.e. when the risk and reward is

transferred to the customer. Revenue is reported after the

deduction of any discounts.

No revenue is initially realized from the sale of vehicles subject

to buy-back agreements. The difference between the selling

price and the expected buy-back price is recognized on a

straight-line basis over the period between sale and buy-back.

Vehicles that are still included in the accounts are reported

under inventories.

Where additional services have been contractually agreed with

the customer in addition to the sale of a vehicle, such as warranty

extensions, mobile services or the completion of maintenance

work over a fixed period, the related revenues and expenses

are recorded in the Income Statement in accordance with the

provisions of IAS 18 governing arrangements with multiple

deliverables based on the economic content of the individual

contractual components (partial services).

Operating expenses are recognized in profit or loss when the

service is used or at the time they are economically incurred.

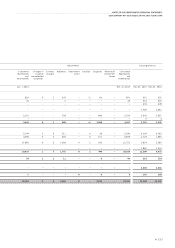

/INTANGIBLE ASSETS

Intangible assets acquired for consideration are recognized at

their cost of purchase, taking into account ancillary costs and

cost reductions, and are amortized on a scheduled straight-line

basis over their useful life.

Concessions, rights and licenses relate to purchased software,

rights of use and subsidies paid.

Goodwill from a business combination has an indefinite useful

life and is subject to regular impairment testing.

Brand names from business combinations generally have an

indefinite useful life and are therefore not amortized. An in-

definite useful life frequently arises from the continued use

and maintenance of a brand. Brand names are tested regularly

for impairment.

Research costs are treated as current expenses in accordance

with IAS 38. The development expenditure for products going

into series production is recognized as an intangible asset,

provided that the sale of these products is likely to bring eco-

nomic benefit to the Audi Group. If the conditions stated in

IAS 38 for capitalization are not met, the costs are expensed in

the Income Statement in the year in which they occur.

Capitalized development costs encompass all direct and indirect

costs that can be directly allocated to the development process.

Capitalized development costs are amortized on a straight-line

basis from the start of production over the anticipated model

life of the developed products.

Depreciation, allocated to the corresponding functional areas,

is primarily based on the following useful lives, which are

reassessed yearly:

Useful life

Concessions, industrial property rights and similar

rights and assets 3–15 years

of which software 3 years

of which customer base 2–8 years

Capitalized development costs 4-9 years

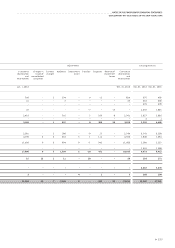

/PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment are measured at cost of pur-

chase or construction, with straight-line depreciation applied

pro rata temporis over the expected useful life.

The costs of purchase include the purchase price, ancillary

costs and cost reductions.

In the case of self-constructed fixed assets, the cost of con-

struction includes both the directly attributable material and

labor costs as well as indirect material and indirect labor costs

that must be capitalized, including pro rata depreciation.