AT&T Wireless 2008 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2008 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

AT&T Annual Report 2008

| 37

subsidiaries’ networks and exchange local calls enter into

interconnection agreements with us. Any unresolved issues

in negotiating those agreements are subject to arbitration

before the appropriate state commission. These agreements

(whether fully agreed-upon or arbitrated) are then subject to

review and approval by the appropriate state commission.

Recently, in a number of the states in which we operate as

an ILEC, state legislatures or the state public utility commissions

have concluded that the voice telecommunications market

is competitive and have allowed for greater pricing flexibility

for non-basic residential retail services, including bundles,

promotions and new products and services. While it has been

a number of years since we have been allowed to raise local

service rates in certain states, some of these state actions

have been challenged by certain parties and are pending

court review.

In addition to these rates and service regulations noted

above, our wireline subsidiaries (excluding rural carrier

affiliates) operate under state-specific elective “price-cap

regulation” for retail services (also referred to as “alternative

regulation”) that was either legislatively enacted or authorized

by the appropriate state regulatory commission. Under

price-cap regulation, price caps are set for regulated services

and are not tied to the cost of providing the services or to

rate-of-return requirements. Price-cap rates may be subject

to or eligible for annual decreases or increases and also may

be eligible for deregulation or greater pricing flexibility if the

associated service is deemed competitive under some state

regulatory commission rules. Minimum customer service

standards may also be imposed and payments required if

we fail to meet the standards.

We continue to lose access lines due to competitors

(e.g., wireless, cable and VoIP providers) who can provide

comparable services at lower prices because they are not

subject to traditional telephone industry regulation (or the

extent of regulation is in dispute) and consequently have

lower cost structures. In response to these competitive

pressures, for several years we have utilized a bundling

strategy that rewards customers who consolidate their

services (e.g., local and long-distance telephone, DSL,

wireless and video) with us. We continue to focus on bundling

wireline and wireless services, including combined packages

of minutes and video service through our AT&T U-verse

service and our relationships with satellite television providers.

We will continue to develop innovative products that

capitalize on our expanding fiber network.

Additionally, we provide local, domestic intrastate and

interstate, international wholesale networking capacity and

switched services to other service providers, primarily large

Internet Service Providers using the largest class of

nationwide Internet networks (Internet backbone), wireless

carriers, CLECs, regional phone ILECs, cable companies

and systems integrators. These services are subject to

additional competitive pressures from the development

of new technologies and the increased availability of

domestic and international transmission capacity.

The introduction of new products and service offerings

and increasing satellite, wireless, fiber-optic and cable

transmission capacity for services similar to those provided

by us continues to provide competitive pressures. We face

a number of international competitors, including Equant,

British Telecom and SingTel; as well as competition from

a number of large systems integrators, such as Electronic

Data Systems.

Advertising & Publishing

Our advertising & publishing subsidiaries face competition

from approximately 100 publishers of printed directories in

their operating areas. Competition also exists from other

advertising media, including newspapers, radio, television and

direct-mail providers, as well as from directories offered over

the Internet. Through our wholly-owned subsidiary, YPC, we

compete with other providers of Internet-based advertising

and local search.

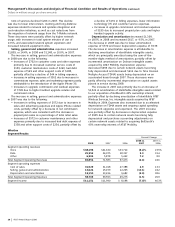

ACCOUNTING POLI C I ES AND STANDA RDS

Significant Accounting Policies and Estimates Because of

the size of the financial statement line items they relate to,

some of our accounting policies and estimates have a more

significant impact on our financial statements than others.

The policies below are presented in the order in which the

topics appear in our consolidated statements of income.

Allowance for Uncollectibles We maintain an allowance

for doubtful accounts for estimated losses that result from

the failure of our customers to make required payments.

When determining the allowance, we consider the probability

of recoverability based on past experience, taking into account

current collection trends as well as general economic factors,

including bankruptcy rates. Credit risks are assessed based

on historical write-offs, net of recoveries, and an analysis of

the aged accounts receivable balances with reserves generally

increasing as the receivable ages. Accounts receivable may

be fully reserved for when specific collection issues are

known to exist, such as pending bankruptcy or catastrophes.

The analysis of receivables is performed monthly and the

bad-debt allowances are adjusted accordingly. A 10% change

in the amounts estimated to be uncollectible would result

in a change in uncollectible expense of approximately $130.

Pension and Postretirement Benefits Our actuarial

estimates of retiree benefit expense and the associated

significant weighted-average assumptions are discussed in

Note 11. One of the most significant of these assumptions

is the return on assets assumption, which was 8.50% for the

year ended December 31, 2008. In setting the long-term

assumed rate of return, management considers capital

markets future expectations and the asset mix of the plans’

investments. The actual long-term return can, in relatively

stable markets, also serve as a factor in determining future

expectations. However, the dramatic adverse market

conditions in 2008 have skewed the calculation of the

long-term actual return; the actual 10-year return was

4.21% through 2008 compared with 9.18% through 2007.

The severity of the 2008 losses will make the 10-year actual

return less of a relevant factor in management’s evaluation

of future expectations. Based on future expectations and the

plans’ asset mix, management has left unchanged the

long-term assumed rate of return for 2009. If all other factors

were to remain unchanged, we expect that a 1.0% decrease

in the assumed long-term rate of return would cause 2009