AT&T Wireless 2008 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2008 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

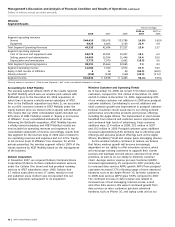

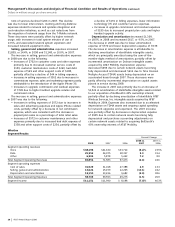

Management’s Discussion and Analysis of Financial Condition and Results of Operations (continued)

Dollars in millions except per share amounts

36

| AT&T Annual Report 2008

remanded. The Court of Appeals vacated the E911 Order in

September 2008. As of the date of this report, discussions

are continuing between the FCC, wireless carriers, and the

public safety community as to what steps should be taken

regarding improved E911 accuracy.

Wireless Universal Service AT&T Mobility is currently

a Competitive Eligible Telecommunications Carrier (CETC)

for purposes of receiving federal universal service support

inseveral states. To maintain these designations, the state

must certify that the carrier is entitled to receive the funds

for the subsequent calendar year based on federal and

applicable state CETC requirements. We arecurrent on our

certifications and have a process to review these requirements

on an annual basis. In May 2008, the FCC adopted an Order

capping high-cost universal service support received by

CETCs — predominantly wireless carriers — at a statewide

level. The state-specific cap will be set based on the amount

of support that CETCs in that state were eligible to receive

in March 2008 on an annualized basis. Notably, while AT&T

previously consented to a voluntary cap on its receipt of

federal universal service support as of June 30, 2007 in

order to obtain approval for the acquisition of Dobson, this

commitment was superseded by the industry-wide CETC

cap adopted in the May 2008 Order. The industry-wide cap

was implemented in the third quarter of 2008. AT&T Mobility

received approximately $211 million in federal high-cost

support in 2008.

State Regulation A summary of significant 2008 state

regulatory developments follows.

Video Service Legislation A number of states in which we

operate have adopted legislation or issued clarifying opinions

that will make it easier for telecommunications companies to

offer video service.

California High Cost Fund In June 2006, the California

Public Utilities Commission (CPUC) opened a rulemaking

to review the California High Cost Fund B (CHCF-B).

The CHCF-B program was established in 1996 and was

designed to support universal service goals by ensuring

that basic telephone service remains affordable in high-cost

areas within the service territories of the state’s major

incumbent local exchange carriers. In September 2007,

the CPUC adopted a decision that changed how the

CHCF-B is calculated. We estimate the change will reduce

our payments from the CHCF-B by approximately $100 in

2009 compared to 2008 payments. In September 2008, the

CPUC adopted a related decision, which permits but does

not require, increases to basic rates of prescribed amounts

over a two-year phase-in period beginning January 1, 2009.

This two-year transition period concludes with full

pricing flexibility for basic residential service starting

January 1, 2011.

CO M PETIT I O N

Competition continues to increase for telecommunications

and information services. Technological advances have

expanded the types and uses of services and products

available. In addition, lack of or a reduced level of regulation

of comparable alternatives (e.g., cable, wireless and

VoIP providers) has lowered costs for these alternative

communications service providers. As a result, we face

heightened competition as well as some new opportunities

in significant portions of our business.

Wireless

We face substantial and increasing competition in all aspects

of our wireless business. Under current FCC rules, six or

more PCS licensees, two cellular licensees and one or more

enhanced specialized mobile radio licensees may operate

in each of our service areas, which results in the potential

presence of multiple competitors. Our competitors are

principally three national (Verizon Wireless, Sprint Nextel Corp.

and T-Mobile) and a larger number of regional providers of

cellular, PCS and other wireless communications services.

More than 95% of the U.S. population lives in areas with

three mobile telephone operators and more than half the

population lives in areas with at least five competing carriers.

We may experience significant competition from companies

that provide similar services using other communications

technologies and services. While some of these technologies

and services are now operational, others are being developed

or may be developed in the future. We compete for customers

based principally on price, service offerings, call quality,

coverage area and customer service.

We were a winning bidder in the FCC 700 MHz spectrum

auctions that began in January 2008, and in 2008, we

purchased additional spectrum licenses covering 196 million

people in the 700 MHz frequency band. The availability of

this additional spectrum from the auctions could increase

the effectiveness of existing competition, or result in new

entrants in the wireless arena.

Wireline

Our wireline subsidiaries expect continued competitive

pressure in 2009 from multiple providers, including wireless,

cable and other VoIP providers, interexchange carriers

and resellers. In addition, economic pressures are forcing

customers to terminate their traditional local wireline

service and substitute wireless and Internet-based services,

intensifying a pre-existing trend toward wireless and Internet

use. At this time, we are unable to quantify the effect of

competition on the industry as a whole, or financially on

this segment. However, we expect both losses of revenue

share in local service and gains resulting from business

initiatives, especially in the area of bundling of products

and services, including wireless and video, large-business

data services and broadband. In most markets, we compete

with large cable companies, such as Comcast Corporation,

Cox Communications, Inc. and Time Warner Inc., for local,

high-speed Internet and video services customers and

other smaller telecommunications companies for both

long-distance and local services customers.

Our wireline subsidiaries generally remain subject to

regulation by state regulatory commissions for intrastate

services and by the FCC for interstate services. In contrast,

our competitors are often subject to less or no regulation

in providing comparable voice and data services or the

extent of regulation is in dispute. Under the Telecom Act,

companies seeking to interconnect to our wireline