TCF Bank 2014 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2014 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

|

|

these loans is recognized on a cash basis when there is sustained repayment performance for six consecutive months, the loan

is not more than 60 days delinquent and a current credit evaluation has been completed.

Generally, when a loan or lease is placed on non-accrual status, uncollected interest accrued in prior years is charged-off against

the allowance for loan and lease losses and interest accrued in the current year is reversed against interest income. For

non-accrual leases that have been discounted with third-party financial institutions on a non-recourse basis, the related liability is

also placed on non-accrual status. Interest payments received on loans and leases in non-accrual status are generally applied to

principal unless the remaining principal balance has been determined to be fully collectible, in which case interest income is

recognized on a cash basis.

Premises and Equipment Premises and equipment, including leasehold improvements, are carried at cost and are

depreciated or amortized on a straight-line basis over estimated useful lives of owned assets and for leasehold improvements

over the estimated useful life of the related asset or the lease term, whichever is shorter. Maintenance and repairs are charged to

expense as incurred. Rent expense for leased land with facilities is recognized in occupancy and equipment expense. Rent

expense for leases with free rent periods or scheduled rent increases is recognized on a straight-line basis over the lease term.

Other Real Estate Owned and Repossessed and Returned Assets Assets acquired through foreclosure, repossession or

returned to TCF are initially recorded at the lower of the loan or lease carrying amount or fair value of the collateral less estimated

selling costs at the time of transfer to real estate owned or repossessed and returned assets. The fair value of other real estate

owned is based on independent appraisals, real estate brokers’ price opinions or automated valuation methods, less estimated

selling costs. The fair value of repossessed and returned assets is based on available pricing guides, auction results or price

opinions, less estimated selling costs. Any carrying amount in excess of the fair value less estimated selling costs is charged off

to the allowance for loan and lease losses. Subsequently, if the fair value of an asset, less the estimated costs to sell, declines to

less than the carrying amount of the asset, the shortfall is recognized in the period in which it becomes known and is included in

foreclosed real estate and repossessed assets, net expense. Operating expenses of properties and recoveries on sales of other

real estate owned are also recorded in foreclosed real estate and repossessed assets, net. Operating revenue from foreclosed

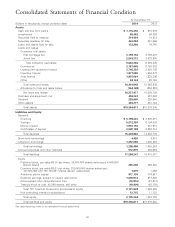

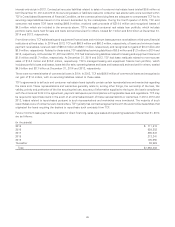

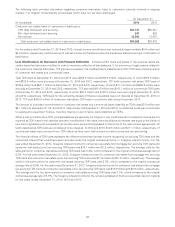

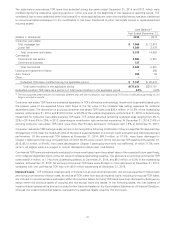

property is included in other non-interest income. Other real estate owned at December 31, 2014 and 2013, was $65.7 million

and $68.9 million, respectively. Repossessed and returned assets at both December 31, 2014 and 2013, was $3.5 million.

Investments in Affordable Housing Limited Partnerships Investments in affordable housing consist of investments in

limited partnerships that operate qualified affordable housing projects or that invest in other limited partnerships formed to

operate affordable housing projects. TCF generally utilizes the effective yield method to account for these investments with the

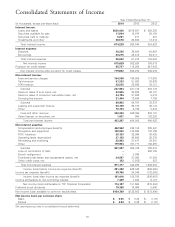

tax credits and amortization of the investment reflected in the Consolidated Statements of Income as a reduction of income tax

expense. However, depending on circumstances, the equity or cost methods may be utilized. The amount of the investment

along with any unfunded equity contributions which are unconditional and legally binding are recorded in other assets. A liability

for the unfunded equity contributions is recorded in other liabilities.

Interest-Only Strips TCF periodically sells loans to third party financial institutions at fixed or variable rates. For those

transactions which achieve sale treatment, the underlying loan is not recognized on TCF’s Consolidated Statements of Financial

Condition. The Company sells these loans at par value and generally retains an interest in the future cash flows of borrower loan

payments, known as an interest-only strip. The interest-only strip is recorded at fair value at the time of sale. The fair value of the

interest-only strip represents the present value of future cash flows generated by the loans to be retained by TCF. After initial

recording of the interest-only strip, the accretable yield is measured as the difference between the initial investment, or fair

value, and the cash flows expected to be collected. The accretable yield is amortized into interest income over the life of the

interest-only strip using the effective yield method. The expected cash flows are evaluated quarterly to determine if they have

changed from previous projections. If the present value of the original cash flows expected to be collected is less than the

present value of the current estimate of cash flows to be collected, the change is adjusted prospectively over the remaining life

of the interest-only strip. If the present value of the original cash flows expected to be collected is greater than the present value

of the current estimate, an other than temporary impairment is generally recorded.

Intangible Assets All assets and liabilities acquired in purchase acquisitions, including goodwill and other intangibles, are

recorded at fair value. Goodwill is recorded when the purchase price of an acquisition is greater than the fair value of net assets,

including identifiable intangible assets. Goodwill is not amortized, but assessed for impairment on an annual basis at the

reporting unit level. Interim impairment analysis may be required if events occur or circumstances change that would more likely

than not reduce a reporting unit’s fair value below its carrying amount. Other intangible assets are amortized on a straight-line or

effective yield basis over their estimated useful lives and are subject to impairment if events or circumstances indicate a possible

inability to realize their carrying amounts.

When testing for goodwill impairment, TCF initially performs a qualitative assessment. Based on the results of this qualitative

assessment, if TCF concludes it is more likely than not that a reporting unit’s fair value is less than its carrying amount, a

60